In 2026, tech startups are redefining entire industries by turning cutting-edge technology into scalable, real-world systems. Companies like Linker Vision, Articul8 AI, and Genspark show how innovation now spans smart cities, enterprise AI, and next-generation search – amid a record surge in investment, with nearly 46% of global startup funding flowing into AI and tech startups in 2025.

Much like how Google reshaped information access or Airbnb transformed travel, today’s startups begin with focused pilots or MVPs and scale rapidly through repeatable models. From Anduril’s autonomous defense systems to Discord’s global creator and community platforms, these companies prioritize speed, technical depth, and real-world impact. In this landscape, sustained growth depends not only on innovation, but on how effectively your tech startup is discovered online.

Tech startups are early-stage companies that use technology to solve problems and scale rapidly. In 2026, the most active sectors include AI, robotics, cybersecurity, defense tech, Web3, digital health, EdTech, fintech, and enterprise IT startups modernizing core business infrastructure.

Key Characteristics of Tech Startups

- Technology-first: Built around software, AI, hardware, or emerging technologies

- Rapid scalability: Designed to grow without proportional cost increases

- Venture-backed: Often funded by VCs, with some reaching unicorn status ($1B+)

- High-risk, high-reward: Fast innovation cycles with significant failure rates

How Do Tech Startups Operate?

- Define the Problem: Good startup ideas often begin by identifying market pain through customer validation

- Build MVP: Create minimum viable product to test hypothesis, a critical step for small tech startups operating with limited capital and compressed timelines

- Validate Demand: Secure pilot customers before scaling

- Raise Capital: Attract funding based on traction and team credibility

- Scale Execution: Expand through repeatable systems

- Iterate Rapidly: Continuously improve based on feedback

Challenges of Tech Startups

- High failure rates: 90% of startups fail.

- Capital intensity: Robotics, defense, and physical AI require heavy upfront investment

- Security risks: Identity breaches and AI-driven threats are increasing

- Talent competition: Startup hubs face intense demand for skilled engineers

Examples of Tech Startups

- Figure AI: Humanoid robots deployed in manufacturing

- Anduril Industries: Autonomous defense and AI-powered systems

- Zipline: Drone delivery platform with over one million commercial deliveries

- Suno: AI music generation platform producing millions of songs daily

- Discord: Community communication platform with 200M+ monthly users

Resources for Exploring Tech Startups

- Accelerators: Y Combinator, Techstars, 500 Global, Founder Institute

- Funding & data platforms: Crunchbase, PitchBook, Wellfound, Carta

- Venture capital firms: Andreessen Horowitz, Sequoia Capital, Founders Fund

This guide focuses on robotics, cybersecurity, defense and aerospace technology, AI infrastructure, gaming and entertainment, and enterprise tools and platforms.

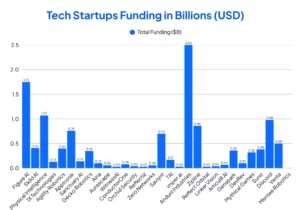

Quick Summary of the Top 30 Tech Startups Funding

| Rank | Company | Category | Location | Total Funding | Valuation | Latest Round | Lead Investor(s) |

|---|---|---|---|---|---|---|---|

| 1 | Figure AI | Humanoid Robotics | Sunnyvale, CA | $1.75B | $39B | Series B+ (2024–2025) | Jeff Bezos, Microsoft, OpenAI, Nvidia |

| 2 | Skild AI | Robotics AI | Pittsburgh, PA | $414M | $1.5B | $300M Series A (Jul 2024) | Lightspeed, Coatue, SoftBank |

| 3 | Physical Intelligence | Robot AI | San Francisco, CA | $1.07B | $5.6B | $600M Series B (Nov 2025) | CapitalG, Jeff Bezos, OpenAI |

| 4 | 1X Technologies | Humanoid Robotics | Norway / SF | $126M | Not disclosed | $100M Series B (Jan 2024) | EQT Ventures, OpenAI Fund |

| 5 | Agility Robotics | Humanoid Manufacturing | Salem, OR | ~$400M | $1.75B | Series D (raising, 2025) | Amazon, GXO, Nvidia |

| 6 | Apptronik | Humanoid Robotics | Austin, TX | $763M | $5B | $350M Series A (Feb 2025) | B Capital, Capital Factory, Google |

| 7 | Sanctuary AI | Humanoid Robotics | Vancouver, Canada | $140M+ | Not disclosed | Strategic (Jul 2024) | BDC Capital, InBC, Magna |

| 8 | Gecko Robotics | Inspection Robots | Pittsburgh, PA | $354M | $1.25B | $125M Series D (Jun 2025) | Cox Enterprises, Founders Fund |

| 9 | Airia | AI Security | Atlanta, GA | $100M | Not disclosed | $100M (Sep 2025) | Not disclosed |

| 10 | Aurascape | AI Security | Palo Alto, CA | $62.8M | Not disclosed | $50M (Apr 2025) | Greylock, Menlo Ventures |

| 11 | WitnessAI | AI Governance | San Francisco, CA | $27.5M | Not disclosed | $27.5M Series A (May 2024) | GV, Ballistic Ventures |

| 12 | ConductorOne | Identity Security | San Francisco, CA | $79M | Not disclosed | $79M Series B (Oct 2025) | Greycroft, CrowdStrike Fund |

| 13 | Orchid Security | Identity Security | New York, NY | $36M | Not disclosed | $36M Seed (Jan 2025) | Team8, Intel Capital |

| 14 | Reflectiz | Web Security | Tel Aviv, Israel | $28M | Not disclosed | $22M Series B (Oct 2025) | Titanium Ventures, Intel Capital |

| 15 | Zero Networks | Zero Trust | Tel Aviv, Israel | $55M | Not disclosed | $55M Series C (Jun 2025) | U.S. Venture Partners, CrowdStrike |

| 16 | Saviynt | Identity Security | El Segundo, CA | $700M | ~$3B | $700M Series B (Dec 2025) | KKR |

| 17 | 7AI | Agentic Security | Palo Alto, CA | $166M | Not disclosed | $130M Series A (Dec 2025) | Index Ventures, Greylock |

| 18 | imper.ai | Anti-Impersonation | NYC / Tel Aviv | $28M | Not disclosed | $28M Seed (Dec 2025) | Not disclosed |

| 19 | Anduril Industries | Defense Tech | Costa Mesa, CA | $2.5B+ | $30.5B | $2.5B Series F (Jun 2025) | Founders Fund, Fidelity |

| 20 | Zipline | Drone Delivery | South San Francisco, CA | $863M+ | $5.22B | $350M Series G (Jun 2024) | Baillie Gifford, Temasek |

| 21 | Reflect Orbital | Space Tech | Los Angeles, CA | $26.5M | Not disclosed | $20M Series A (May 2025) | Lux Capital, Sequoia |

| 22 | Linker Vision | AI Edge Computing | Taipei, Taiwan | $35M | Not disclosed | $35M Series A (Dec 2025) | Nvidia, Abico Group |

| 23 | Articul8 AI | Enterprise AI | Palo Alto, CA | ~$70M | $500M+ | Series B (raising, Jan 2026) | Intel spin-off |

| 24 | Genspark | AI Productivity | San Francisco, CA | $360M+ | $1.25B | $275M Series B (Nov 2025) | Emergence Capital, LV Tech |

| 25 | Mentee Robotics | Humanoid Robotics | Tel Aviv, Israel | — | $900M | Acquisition (Jan 2026) | Mobileye (Intel) |

| 26 | DevRev | AI Platform | Palo Alto, CA | $100.8M | $1.15B | $100.8M Series A (Aug 2024) | Khosla Ventures, Mayfield |

| 27 | Mythical Games | Blockchain Gaming | Sherman Oaks, CA | $319M | $1.25B | $150M Series C (Nov 2021) | Andreessen Horowitz, Binance |

| 28 | Suno | AI Music | Cambridge, MA | $375M | $2.45B | $250M Series C (Nov 2025) | Menlo Ventures, Lightspeed |

| 29 | Discord | Communication | San Francisco, CA | $978M | $15B (2021) | IPO Filed (Jan 2026) | Dragoneer Investment Group |

| 30 | Vanta | Compliance | San Francisco, CA | $504M | $4.15B | $150M Series D (Jul 2025) | Wellington Management |

30 Revolutionary Tech Startups Reshaping Industries in 2026

These 30 tech startups represent the sharpest edge of innovation in 2026, building real-world systems across AI, robotics, cybersecurity, defense, and enterprise infrastructure. Each company shows how focused technology, backed by capital and execution, is transforming entire industries at scale.

Category 1: Humanoid Robotics & Physical AI

The humanoid robotics market is projected to reach $38 billion by 2035 according to Goldman Sachs with Austin seed and Series A tech AI startups in 2026 increasingly contributing to robotics, AI infrastructure, and physical automation breakthroughs.

The sector attracted $3.2 billion in funding across 2024-2025, with eight companies developing general-purpose robots for manufacturing, warehousing, and home applications.

Quick facts: Founded in 2022 · Sunnyvale, California · Series C · $1.75B+ raised at $39B valuation (Sep 2025) · Backed by Parkway Venture Capital, Bezos Expeditions, OpenAI, Nvidia, Microsoft

Why it stands out: Figure AI achieved the fastest path to unicorn status in robotics history, reaching $39B valuation within 3 years. Their humanoid robots (Figure 01 and Figure 02) are deployed in BMW manufacturing facilities, demonstrating real-world commercial viability.

Who it’s built for: Automotive manufacturers facing labor shortages, logistics companies seeking warehouse automation, construction firms requiring dangerous task automation, and enterprises exploring AI-powered physical labor.

The opportunity: Figure’s valuation increased 15x from $2.6B to $39B in just 7 months (February 2024 Series B to September 2025 Series C), reflecting explosive investor confidence in commercial humanoid robotics.

Proof of traction: Partnership with OpenAI for AI model development, active deployment at BMW facilities, and raised $675M Series B at $2.6B valuation in February 2024 from Jeff Bezos, Nvidia, and Microsoft.

Quick facts: Founded in 2023 · Pittsburgh, Pennsylvania · Series A · $300M raised at $1.5B valuation (July 2024) · Total funding: $414M · Backed by Lightspeed Venture Partners, Coatue, SoftBank Group, Jeff Bezos

Why it stands out: Skild AI is building the world’s first general-purpose foundation model for robotics—one AI “brain” that can control any robot platform for manipulation, locomotion, and navigation tasks. Only 16 employees at Series A announcement.

Who it’s built for: Robot manufacturers seeking plug-and-play intelligence, industrial automation companies deploying diverse robot fleets, research institutions advancing robotics AI, and enterprises building custom robotic solutions.

The opportunity: Foundation models revolutionized language AI; Skild AI aims to do the same for robotics. Their model demonstrates unprecedented generalization across robot types and tasks, positioning them as the “OpenAI of robotics.”

Proof of traction: Raised largest robotics AI Series A in history ($300M), demonstrating exceptional capital efficiency and technology validation from top-tier investors.

🌐 Website

Quick facts: Founded in 2024 · San Francisco, California · Series B · $600M Series B at $5.6B valuation (Nov 2025) · Series A: $400M at $2B (Nov 2024) · Total funding: $1.07B · Backed by Google CapitalG, Jeff Bezos, OpenAI, Thrive Capital

Why it stands out: Physical Intelligence (π) is developing a foundation model for robotic intelligence with a team of former researchers from Google DeepMind, Tesla, and OpenAI. Valuation increased from $2B to $5.6B in 12 months.

Who it’s built for: Robotics companies seeking universal AI controllers, manufacturers deploying diverse robot types, research labs pushing embodied AI boundaries, and enterprises automating complex physical tasks.

The opportunity: One of the fastest-growing robotics valuations in venture history, with Google’s CapitalG leading their Series B, signaling strategic importance to Alphabet’s robotics ambitions.

Proof of traction: Raised $400M Series A in November 2024 followed by $600M Series B 12 months later, demonstrating exceptional momentum and investor confidence in their “universal brain” approach.

🌐 Website

Quick facts: Founded in 2014 · Palo Alto, California (Norway origin) · Series B · $100M raised (Jan 2024) · Total funding: $126M · Backed by EQT Ventures, Samsung, OpenAI Startup Fund

Why it stands out: 1X Technologies secured a 10,000-unit deployment deal with EQT (2026-2030) and opened pre-orders for their NEO humanoid home robot at $20,000. Reportedly seeking $1B raise at $10B valuation.

Who it’s built for: Consumers seeking in-home assistance robots, enterprises deploying humanoids for logistics and warehousing, healthcare facilities requiring physical support automation, and hospitality industry exploring service robotics.

The opportunity: One of the first companies targeting the consumer home robotics market, with NEO designed for household tasks. The 10,000-unit EQT deal represents one of the largest commercial humanoid deployments announced to date.

Proof of traction: 10,000-unit deployment agreement with EQT portfolio companies spanning 2026-2030, NEO pre-orders opened October 2025, and seeking $1B funding round demonstrating market confidence.

Quick facts: Founded in 2015 · Salem, Oregon · Series D (raising) · $400M at $1.75B valuation (Apr 2025) · Backed by Amazon, Playground Global, DCVC

Why it stands out: Agility Robotics operates the world’s first full-scale humanoid robot factory (RoboFab) opened in 2024, and their Digit robot is the first commercially available humanoid in production, deployed at Amazon fulfillment centers and Spanx facilities.

Who it’s built for: E-commerce fulfillment centers facing labor shortages, logistics companies automating warehouses, manufacturing facilities seeking flexible automation, and retailers optimizing distribution operations.

The opportunity: Only humanoid currently operating in commercial logistics at scale, with partnership with Amazon since 2023 and active deployments demonstrating real-world ROI in warehouse environments.

Proof of traction: Deployed at Amazon fulfillment centers and Spanx facilities in 2024, opened RoboFab manufacturing facility, and raising $400M Series D at $1.75B valuation.

🌐 Website

Quick facts: Founded in 2016 · Austin, Texas · Series A · $350M raised (Feb 2025) · Total: $763M at $5B valuation · Backed by B Capital, Capital Factory, Google/Alphabet

Why it stands out: Apptronik partnered with Google DeepMind Robotics (December 2024) and developed 15 robotic systems including NASA’s Valkyrie robot. Their Apollo humanoid targets logistics, manufacturing, and elder care with premoney valuation of $5B.

Who it’s built for: Industrial manufacturers automating assembly lines, logistics companies seeking warehouse automation, healthcare facilities deploying elder care assistants, and aerospace companies requiring specialized robotic systems.

The opportunity: Partnership with Google DeepMind provides access to cutting-edge AI capabilities, while NASA heritage demonstrates technical sophistication. Targeting commercial deployments in 2026.

Proof of traction: Developed 15 robotic systems including NASA’s Valkyrie, partnership with Google DeepMind announced December 2024, and raised $350M Series A with $5B premoney valuation.

Quick facts: Founded in 2018 · Vancouver, Canada · Strategic Investment · $140M+ total funding (July 2024) · Backed by BDC Capital, InBC Investment, Magna International, BCE

Why it stands out: Sanctuary AI’s Phoenix robot (7th generation, April 2024) is priced at $40,000 upfront cost and powered by their proprietary Carbon AI control system. Partnership with Magna International targets automotive manufacturing deployments.

Who it’s built for: Automotive manufacturers seeking assembly line automation, telecommunications companies deploying field service robots, industrial facilities requiring flexible automation, and enterprises exploring human-robot collaboration.

The opportunity: Partnership with Magna International provides access to global automotive supply chain. Reportedly seeking additional $175M raise to accelerate commercial deployments.

Proof of traction: $140M+ raised by July 2024, partnership with Magna International for automotive applications, and Phoenix 7th generation launched April 2024.

Quick facts: Founded in 2013 · Pittsburgh, Pennsylvania · Series D · $125M raised at $1.25B valuation (June 2025) · Total: $354M · Employees: 101-200 · Backed by Cox Enterprises, Y Combinator, Founders Fund

Why it stands out: Gecko Robotics achieved unicorn status in June 2025 with wall-climbing robots that inspect critical infrastructure (power plants, refineries, ships). Planning UAE factory by 2026.

Who it’s built for: Energy companies maintaining power generation facilities, defense contractors inspecting ships and submarines, oil & gas refineries requiring asset integrity management, and industrial facilities preventing catastrophic failures.

The opportunity: Operating in defense, energy, and manufacturing sectors where infrastructure inspection prevents billions in potential failures. Expanding internationally with UAE factory planned for 2026.

Proof of traction: Achieved unicorn status with $1.25B valuation in June 2025, Y Combinator alumnus (W16), and planning UAE manufacturing facility demonstrating international expansion.

- Hardware R&D: $50M-$200M per company

- Manufacturing facilities (Agility’s RoboFab alone likely >$100M)

- Unlike software, you can’t prototype robots in a garage

- Figure AI: BMW manufacturing pilot validates technology

- 1X Technologies: 10,000-unit EQT deal (2026-2030)

- Agility: Amazon + Spanx deployments prove commercial viability

The Pattern: Not one of these 8 humanoid robotics companies is profitable, yet they’ve raised over $4 billion. Here’s why investors are betting big:

Capital Intensity = Barrier to Entry

“Deploy First, Monetize Later” Strategy

The Valuation Rocket: Data Network Effects

More deployments → More training data → Better AI → More customers → Lower unit costs

Figure AI’s 15x jump ($2.6B → $39B in 7 months) wasn’t revenue-driven—it was deployment validation. BMW putting humanoids on production lines signaled the technology works at scale.

Bottom Line: VCs are funding a “land grab” similar to ride-sharing (2014-2016). Market leaders will achieve winner-takes-most dynamics once manufacturing scales.

Category 2: Cybersecurity & Identity Security

The cybersecurity sector raised $1.4+ billion in 2025, driven by AI-driven threats, identity-based attacks, and the need for AI governance. Identity security alone captured $1.1B in funding as enterprises prioritize zero-trust architectures.

Quick facts: Founded in 2024 · Atlanta, Georgia · Series A · $100M raised (Sep 2025) · 300+ customers, 150 employees across 5 continents · Backed by General Catalyst, Ballistic Ventures

Why it stands out: Airia scaled from 0 to 300 enterprise customers in 12 months since emerging from stealth. Their AI security and orchestration platform enables safe enterprise AI adoption with visibility, governance, and protection.

Who it’s built for: Enterprises deploying AI at scale, regulated industries (finance, healthcare, government) requiring AI compliance, security teams managing AI risk, and IT leaders orchestrating multi-model AI deployments.

The opportunity: As enterprises rush to deploy AI, security and governance become critical. Airia’s rapid customer growth demonstrates urgent market need for AI-native security solutions.

Proof of traction: Scaled to 300+ enterprise customers and 150 employees in 12 months, raised $100M Series A, and expanded across five continents demonstrating global demand.

🌐 Website

Quick facts: Founded in 2023 · USA · Stealth Launch · $50M raised (Apr 2025) · Total: $62.8M · Backed by Mayfield Fund, Menlo Ventures (co-led), Greg Clark (ex-Symantec)

Why it stands out: Aurascape AI security platform emerged from stealth in April 2025 with $50M to provide real-time security and observability for AI applications. Addresses Shadow AI, prompt injection, and data leakage with AI-native approach.

Who it’s built for: Enterprises deploying AI applications, security teams managing AI risk, developers building AI-powered products, and compliance teams ensuring AI governance in regulated industries.

The opportunity: Launched after one year in stealth with significant funding, addressing the critical gap in AI application security as enterprises rapidly deploy generative AI across business functions.

Proof of traction: Raised $50M in stealth round co-led by tier-1 VCs, with total funding of $62.8M and backing from former Symantec CEO.

🌐 Website

Quick facts: Founded in 2023 · USA · Series A · $27.5M raised (May 2024) · Employees: 18 (launch), targeting 40 by end 2024 · Backed by GV (Google Ventures), Ballistic Ventures (co-led)

Why it stands out: WitnessAI provides security and governance guardrails for enterprise LLMs and AI applications. Named to Fortune Cyber 60 list (October 2025) and launched automated red-teaming and AI firewall (August 2025).

Who it’s built for: Enterprises deploying LLMs, security teams managing AI model risk, compliance officers ensuring AI governance, and developers building AI applications requiring safety guardrails.

The opportunity: As LLM adoption accelerates, enterprises need guardrails against prompt injection, data exfiltration, and AI impersonation. WitnessAI’s Fortune Cyber 60 recognition validates market urgency.

Proof of traction: Raised $27.5M Series A co-led by GV, launched automated red-teaming in August 2025, and named to Fortune Cyber 60 list in October 2025.

🌐 Website

Quick facts: Founded in 2020 · San Francisco, California · Series B · $79M raised (Oct 2025) · Backed by Greycroft (led), CrowdStrike Falcon Fund, Accel, Felicis

Why it stands out: ConductorOne is the world’s first AI-native identity security platform securing human, non-human, and AI agent identities. Addresses rising identity-related cyberattacks with automated access management at scale.

Who it’s built for: Enterprises managing complex identity ecosystems, security teams implementing zero-trust architectures, IT leaders governing AI agent access, and compliance teams ensuring identity governance.

The opportunity: Identity-based attacks are the #1 cybersecurity threat. ConductorOne’s AI-native approach automates what was previously manual, addressing the explosion of AI agents and non-human identities.

Proof of traction: Raised $79M Series B led by Greycroft in October 2025 with participation from CrowdStrike Falcon Fund, demonstrating strategic validation from cybersecurity leader.

🌐 Website

Quick facts: Founded in 2024 · USA · Seed · $36M raised (Jan 2025) · Backed by YL Ventures, Mayfield Fund, Hetz Ventures

Why it stands out: Orchid Security raised the largest cybersecurity seed round reported in early 2025. Uses LLMs to bring clarity to fragmented identity security, featured at 2025 CRN 10 Cybersecurity Startups to Watch.

Who it’s built for: Enterprises struggling with identity complexity, security teams managing fragmented identity systems, compliance officers ensuring identity governance, and IT leaders seeking AI-powered identity management.

The opportunity: Identity security is fragmented across dozens of tools. Orchid Security uses LLMs to unify and simplify, addressing a painful enterprise problem with cutting-edge AI.

Proof of traction: Raised $36M seed round in January 2025—one of the largest cybersecurity seeds ever—and featured at CRN 10 Cybersecurity Startups to Watch 2025.

🌐 Website

Quick facts: Founded in 2016 · Israel · Series B · $22M raised (Oct 2025) · Total: $28M · Backed by Fulcrum Equity Partners (led)

Why it stands out: Reflectiz provides AI-driven web exposure management, detecting third-party tools and open-source component risks that create silent cyber risks in websites. Continuous Threat Exposure Management (CTEM) approach.

Who it’s built for: E-commerce companies managing third-party scripts, enterprises with public-facing websites, security teams addressing supply chain risk, and compliance officers ensuring website security governance.

The opportunity: Modern websites integrate dozens of third-party tools, creating massive security blind spots. Reflectiz’s platform addresses this growing attack surface as websites become more complex.

Proof of traction: Raised $22M Series B in October 2025 with total funding of $28M to expand AI-driven CTEM solutions.

🌐 Website

Quick facts: Founded in 2019 · Israel · Series C · $55M raised (June 2025) · Backed by Highland Europe (led), U.S. Venture Partners

Why it stands out: Zero Networks provides automated microsegmentation to contain ransomware and stop lateral movement. Positioned as the “Era of the Defender” against attackers with scalable zero trust architecture and MSP-focused go-to-market.

Who it’s built for: Enterprises preventing ransomware spread, security teams implementing zero trust, MSPs offering managed security services, and organizations seeking automated network segmentation.

The opportunity: Microsegmentation has historically been too complex to deploy at scale. Zero Networks automates what was manual, making zero trust practical for organizations of all sizes.

Proof of traction: Raised $55M Series C in June 2025 led by Highland Europe, with MSP-focused channel strategy demonstrating scalable go-to-market approach.

🌐 Website

Quick facts: Founded in 2010 · USA · Series B Growth Equity · $700M raised at ~$3B valuation (Dec 2025) · Backed by KKR (led)

Why it stands out: Saviynt raised the largest cybersecurity growth round in 2025 ($700M) to establish identity security as foundational infrastructure for the AI era. Manages identities for humans, AI agents, and non-human entities with focus on governance, compliance, and risk management.

Who it’s built for: Global enterprises managing complex identity ecosystems, regulated industries ensuring identity compliance, organizations deploying AI agents at scale, and IT leaders seeking unified identity governance.

The opportunity: As AI agents proliferate, identity and access management becomes exponentially more complex. Saviynt’s massive funding round signals investor conviction that identity is critical infrastructure for AI adoption.

Proof of traction: Raised $700M at $3B valuation in December 2025 – largest cybersecurity growth equity round of the year—led by premier growth investor KKR.

🌐 Website

Quick facts: Founded in 2025 · Boston, Massachusetts · Series A · $130M raised at $700M valuation (Dec 2025) · Total: $166M · Backed by Index Ventures (led)

Why it stands out: 7AI raised the largest cybersecurity Series A in history ($130M) just 10 months after emerging from stealth. AI security agents automate cybersecurity investigations, reducing response time from hours to minutes. Founded by Cybereason veterans.

Who it’s built for: Security operations centers (SOCs) overwhelmed by alerts, enterprises seeking automated threat response, security teams facing analyst shortages, and organizations requiring 24/7 security coverage.

The opportunity: The “Agentic Security Inflection Point” is here—AI agents can now handle complex security investigations autonomously, addressing the critical cybersecurity skills shortage while improving response times.

Proof of traction: Raised $130M Series A—largest cybersecurity A-round ever – just 10 months after emerging from stealth in February 2025, at $700M valuation.

🌐 Website

Quick facts: Founded in 2024 · New York City / Israel · Seed · $28M raised (Dec 2025) · Backed by YL Ventures, Mayfield Fund, Hetz Ventures (co-led)

Why it stands out: imper.ai provides real-time cyber impersonation prevention across Zoom, Teams, and Slack. Founded by elite Unit 8200 (Israeli cyber-intelligence) veterans, combating deepfakes and AI-driven social engineering attacks. Launched publicly December 2025.

Who it’s built for: Enterprises vulnerable to CEO fraud, financial institutions preventing wire transfer scams, executives targeted by deepfake attacks, and organizations using video conferencing for sensitive communications.

The opportunity: Deepfake and AI impersonation attacks are exploding. imper.ai addresses the critical threat of real-time impersonation on communication platforms where most business happens today.

Proof of traction: Raised $28M seed in December 2025, founded by Unit 8200 veterans with proven cybersecurity track records, and launched with real-time detection across major communication platforms.

🌐 Website

- Saviynt ($700M): Manages humans + AI agents + non-human identities

- ConductorOne ($79M): Automates access governance

- Orchid ($36M seed): Uses LLMs to unify fragmented identity systems

- 7AI ($130M Series A): AI agents investigate identity threats

- imper.ai ($28M seed): Prevents real-time deepfake impersonation

- Zero Networks ($55M): Microsegmentation to contain breaches

- Average enterprise: 10 human identities per employee (SSO, cloud apps)

- Plus: 45 non-human identities per employee (API keys, AI agents, service accounts)

- Total: 55x identities per employee vs. 5 years ago

The Crisis: 82% of breaches involve compromised identities (Verizon 2025 DBIR). Traditional security focused on perimeters; modern threats exploit identity.

The Common Problem These 6 Companies Solve:

The Identity Explosion:

Traditional tools can’t scale. These 6 companies are building the identity operating system for the AI era.

Investor Signal: Saviynt’s $700M (largest identity round ever) + 7AI’s $130M Series A (largest cybersecurity A-round ever) = identity is now foundational infrastructure, not just a tool.

Category 3: Defense & Aerospace Technology

Defense tech emerged as the hottest sector in 2025, with Anduril alone raising $2.5 billion, making it one of the largest defense technology startup companies in history, while multiple companies followed a pattern of defense tech raising between $100M–$300M in funding to scale autonomous systems.

As autonomous systems, drone delivery, and space infrastructure redefine national security and logistics, founders are increasingly facing a new risk at scale: AI misunderstood what my startup does, and that misinterpretation now shapes investor perception, media narratives, and market positioning.

Quick facts: Founded in 2017 · Costa Mesa, California · Series G · $2.5B raised at $30.5B valuation (June 2025) · Total: $4B+ · Employees: 2,000+ · Backed by Founders Fund ($1B), Fidelity, Franklin Venture Partners

Why it stands out: Anduril is the largest defense tech startup in history with $30.5B valuation. Valuation increased 118% from $14B to $30.5B in 10 months. Founded by Palmer Luckey (Oculus), developing autonomous drones, submarines, and AI-powered defense platforms. Plans to go public.

Who it’s built for: U.S. Department of Defense and allied militaries seeking autonomous systems, defense contractors requiring AI-powered platforms, border security agencies deploying surveillance drones, and special operations forces using advanced robotics.

The opportunity: Rebuilding the “Arsenal of Democracy” for the 21st century with software-defined defense systems. Major contracts with DoD and allies position Anduril as the defense tech leader of the next generation.

Proof of traction: Raised $2.5B at $30.5B valuation (June 2025), up from $14B in August 2024. Plans to IPO, with Palmer Luckey stating Anduril will become publicly traded.

Quick facts: Founded in 2014 · South San Francisco, California · Series G · $350M raised (June 2024) · Valuation: $5.22B · Total: $863M+ · Employees: 1,400 · Plus: $150M U.S. State Department grant (Nov 2025)

Why it stands out: Zipline is the first company to achieve 1 million commercial drone deliveries (70% in 2023-2024). Operating across Rwanda, Ghana, Nigeria, Kenya, Côte d’Ivoire, Japan, and USA. Medical supply delivery reduced blood expiry by 67% in Rwanda. 97% likelihood of IPO according to PitchBook.

Who it’s built for: Healthcare systems delivering medical supplies, retailers expanding instant commerce, governments improving rural logistics, and pharmaceutical companies distributing vaccines and medications.

The opportunity: Drone delivery market projected to reach $65B by 2034 according to PwC. Zipline’s proven track record at scale positions them as the category leader for commercial drone delivery.

Proof of traction: First company to achieve 1 million commercial drone deliveries, operating in 7 countries, received $150M U.S. State Department funding to triple network.

Quick facts: Founded in 2023 · Hawthorne, California · Series A · $20M raised (May 2025) · Seed: $6.5M (Sep 2024) · Total: $26.5M · Backed by Lux Capital (led), Sequoia Capital, Starship Ventures

Why it stands out: Reflect Orbital is building a satellite constellation to reflect sunlight to Earth on demand. Satellites transform into precise orbital mirrors for applications including solar energy extension, emergency lighting, and agricultural optimization. First expected launch in 2026.

Who it’s built for: Solar energy companies extending generation hours, disaster response agencies providing emergency lighting, agricultural operations optimizing crop growth, and utilities managing peak demand.

The opportunity: Novel approach to space infrastructure addressing multiple markets. Controversial concept has raised concerns in astronomical community but represents potential breakthrough in on-demand energy and lighting.

Proof of traction: Raised $20M Series A in May 2025 led by Lux Capital, with first launch expected in 2026.

🌐 Website

- Ukraine-Russia: Demonstrated drone warfare effectiveness

- China-Taiwan tensions: Accelerated autonomous systems demand

- Result: U.S. defense budget +13% (2024-2025), heavy AI/autonomous focus

- Anduril: Computer vision + autonomous navigation (like Tesla)

- Zipline: Route optimization AI (like Uber Eats)

- Reflect Orbital: Satellite control (adjacent to Starlink)

The Shift: In 2016, defense tech was taboo in Silicon Valley. By 2025, Anduril became the most valuable private defense company in history ($30.5B).

What Changed?

1. Geopolitical Reality Check

2. Technology Convergence

All 3 defense companies use the same stack as consumer tech:

3. Software-Defined Hardware = Better Economics

Traditional defense: Cost-plus contracts, 5-year timelines, 15-20x P/E

Defense tech startups: Rapid iteration, software margins (70-80%), valued like SaaS

The Anduril Example: $30.5B pre-revenue valuation because investors bet on software gross margins on hardware through autonomous systems + recurring Lattice OS revenue. Traditional contractors can’t match this because they’re locked into government cost-plus contracts.

Category 4: AI Infrastructure & Edge Computing

As enterprises demand on-premises AI deployment, edge computing and AI infrastructure startups raised $800+ million, blending the economics of a software startup with a focus on sovereign AI, data privacy, and low-latency processing. The AI infrastructure market is projected to reach $227 billion by 2030.

Quick facts: Founded in 2021 · Taipei, Taiwan · Series A · $35M raised (Dec 2025) · Employees: 150+ · Backed by Abico Group (led), Nvidia

Why it stands out: Linker Vision has deployed 50+ smart city projects with 10,000 edge devices processing real-time urban and industrial data. AI software platform for edge computing and smart city infrastructure, expanding across US, Latin America, Asia, Middle East, Europe.

Who it’s built for: Municipal governments deploying smart city systems, industrial manufacturers automating facilities, telecom operators managing urban networks, and robotics companies building autonomous machines.

The opportunity: Global smart city market surpassing $500 billion creates massive opportunity for AI edge infrastructure. Linker Vision’s Nvidia backing and 10,000 deployed devices demonstrate market validation.

Proof of traction: $35M Series A December 2025, 50+ smart city projects deployed, 10,000 edge devices in operation, and Nvidia investment confirming strategic importance.

🌐 Website

Quick facts: Founded in 2023 (Intel spin-off) · Santa Clara, California · Series B (partial) · ~$70M raised (first closing) · Expected total: ~$80M · Valuation: 5x increase from $100M to $500M+ in 18 months · Employees: 100+ · Backed by Intel Capital, Adara Ventures, NXC Corporation

Why it stands out: Articul8 AI spun out from Intel’s incubation program with customer SoftBank-owned DigitalBridge. On-premises generative AI platform for secure enterprise deployment focusing on data sovereignty and privacy-first AI. 5x valuation increase demonstrates rapid market validation.

Who it’s built for: Regulated industries (finance, healthcare, government) requiring on-premises AI, enterprises with data sovereignty requirements, organizations prioritizing privacy-first AI, and companies in jurisdictions with strict data residency laws.

The opportunity: As data privacy regulations tighten globally, demand for on-premises AI solutions accelerates. Articul8’s Intel heritage and rapid valuation growth signal enterprise urgency for sovereign AI.

Proof of traction: Spun out from Intel with strategic backing, secured DigitalBridge as customer, raised ~$70M Series B first closing with valuation increase from $100M to $500M+ in under 18 months.

🌐 Website

Quick facts: Founded in 2023 · USA · Series B · $275M raised at $1.25B valuation (Nov 2025) · Employees: 50 · ARR: $36M · ARR per employee: $200K

Why it stands out: Genspark achieved unicorn status ($1.25B valuation) in November 2025 with AI Workspace that automates email, spreadsheets, and team projects—”Put Busywork on Autopilot.” Revenue grew from $1B to $5B in 8 months. Exceptional $200K ARR per employee demonstrates efficiency.

Who it’s built for: Knowledge workers drowning in busywork, teams managing email overload, organizations seeking productivity automation, and enterprises reducing administrative burden.

The opportunity: Emerged from stealth to unicorn in under 3 years. High revenue efficiency ($200K ARR/employee) with only 50 employees signals product-market fit and scalable business model.

Proof of traction: Achieved $1.25B unicorn valuation November 2025, launched AI Workspace product, and $36M ARR with 50 employees.

🌐 Website

Quick facts: Founded: Recently (exact year not disclosed) · Israel · Acquired by Mobileye for $900M (Jan 2026) · Expected close: Q1 2026 · Acquirer: Mobileye Global Inc. (Intel subsidiary)

Why it stands out: One of the largest robotics acquisitions in 2026. Mobileye aims to dominate “physical AI” across autonomous driving and humanoid robotics. Mobileye stock jumped 18% on acquisition news. Deal announced at CES 2026 in Las Vegas, making it one of the most impactful stories in tech startup news 2026.

Who it’s built for: Automotive manufacturers integrating humanoid robots, autonomous vehicle companies expanding to robotics, logistics operations seeking automation, and enterprises deploying physical AI systems.

The opportunity: Mobileye’s strategic acquisition signals convergence of autonomous driving and humanoid robotics. Integration of Mobileye’s perception systems with Mentee’s humanoid platforms creates powerful synergy.

Proof of traction: $900M acquisition by Mobileye announced January 2026, transaction aims to create leaders in physical AI per CEO statement.

🌐 Website: Information not publicly available (recently acquired)

Category 5: Gaming, Entertainment & Communication

From blockchain gaming to AI-generated music and communication platforms, this sector raised $500+ million as creators and users demand new tools for expression and connection.

Quick facts: Founded in 2018 · Los Angeles, California · Series C · $150M at $1.25B valuation (2021) · Total: $319M · Employees: 250-350 · Revenue: $59.5M · Backed by Andreessen Horowitz (a16z), Galaxy Interactive

Why it stands out: Mythical Games operates flagship game NFL Rivals (officially licensed NFL mobile game) and Blankos Block Party (multiplayer NFT game). Platform enables player-owned economies and NFT marketplaces, focusing on mainstream adoption of blockchain gaming.

Who it’s built for: Gamers seeking true asset ownership, game developers building blockchain games, sports leagues exploring digital collectibles, and enterprises entering Web3 gaming.

The opportunity: Blockchain gaming market projected to reach significant scale as mainstream adoption increases. Mythical’s NFL partnership demonstrates path to bringing blockchain gaming beyond crypto-native audiences.

Proof of traction: $150M Series C at $1.25B valuation led by a16z, $319M total raised, and $59.5M revenue with 250-350 employees.

Quick facts: Founded in 2022 · Cambridge, Massachusetts · Series C · $250M raised at $2.45B valuation (Nov 2025) · Series B: $125M at $500M (May 2024) · Total: $375M+ · Revenue: $200M trailing · Backed by Menlo Ventures (led), Lightspeed, Matrix

Why it stands out: Suno users generate 7 million songs daily. First licensing deal with Warner Music Group (Nov 2025). Text-to-music AI platform for creators. 5x valuation increase from Series B to Series C in 18 months.

Who it’s built for: Musicians seeking creative tools, content creators needing custom music, marketers producing branded audio, and music enthusiasts exploring AI composition.

The opportunity: AI music generation market exploding as barriers to music creation disappear. Suno’s Warner Music deal signals path to legitimacy amid copyright controversies, while 7M daily song generation demonstrates massive adoption.

Proof of traction: 7 million songs generated daily, $2.45B valuation November 2025, $200M trailing revenue, and first major label deal with Warner Music.

🌐 Website

Quick facts: Founded in 2015 · San Francisco, California · Series H · $500M at $18B valuation (Oct 2025) · Total: $995.4M+ · Users: 200M+ monthly active · Backed by Dragoneer Investment Group (led), Sony, Tencent

Why it stands out: Discord has almost $1B in total funding since inception with 200+ million monthly active users. Communication platform for communities spanning gaming, education, crypto, and more. Rejected Microsoft’s $12 billion acquisition offer (2021). Potential IPO in 2026.

Who it’s built for: Gaming communities, online educators, crypto/Web3 projects, creator communities, student groups, and any organization building engaged communities.

The opportunity: Discord redefined online community building beyond gaming. 200M+ MAU demonstrates mainstream adoption, while potential 2026 IPO signals maturity. Rejected $12B Microsoft offer suggests confidence in independent value creation.

Proof of traction: 200+ million monthly active users, $500M Series H at $18B valuation October 2025, $995.4M+ total raised, and potential 2026 IPO.

- Wrong bet: AI replaces musicians → Limited TAM (existing market)

- Right bet: AI enables 100x more people to create → TAM expansion

- Video: Runway, Pika (enable creators)

- Code: GitHub Copilot, Cursor (enable developers)

- Design: Midjourney, DALL-E (enable designers)

Pattern Across All 3 Entertainment Companies: They enable creators, not replace them.

| Company | Creators Enabled | Business Model |

|---|---|---|

| Suno | Musicians | $10–30/month subscriptions |

| Discord | Community builders | Nitro ($10/month) + Server Boosts |

| Mythical | Game developers | NFT marketplace revenue share |

The Insight: Suno’s $2.45B valuation (5x increase in 18 months) proves AI tools for creators beat AI replacing creators.

Why?

Proof: 7 million songs created daily on Suno. Most creators couldn’t make music before – Suno expanded the market.

This pattern repeats everywhere:

Investor Takeaway: Creator-enablement companies (Suno $2.45B, Discord $15B) outpace creator-replacement because they grow markets instead of disrupting them.

Category 6: Enterprise Tools & Platforms

Two standout companies in compliance automation and AI-native platforms are redefining how enterprises operate in regulated industries and manage customer-product workflows.

Quick facts: Founded in 2017 · San Francisco, California · Series D · $150M at $4.2B valuation (2025) · Employees: 201-500 · Customers: 8,000+ companies · Backed by Sequoia Capital, Y Combinator

Why it stands out: Vanta automates security and compliance certifications (SOC 2, ISO 27001, GDPR, HIPAA) serving 8,000+ companies globally. Y Combinator alumnus (W18) enabling startups to achieve enterprise-grade compliance in weeks instead of months.

Security frameworks like SOC 2 and GDPR aren’t just checkboxes, they’re sales accelerators. Top-performing SaaS startups combine automated compliance with strong on-page SEO to build authority signals that accelerate enterprise trust and deal velocity.

Who it’s built for: Startups seeking enterprise customers, regulated industries (finance, healthcare) ensuring compliance, growing companies scaling security programs, and enterprises managing multi-framework compliance.

The opportunity: Every B2B startup needs compliance certifications to sell to enterprises. Vanta’s 8,000+ customer base and $4.2B valuation demonstrate the massive market for automated compliance as more companies pursue enterprise sales.

Proof of traction: Serving 8,000+ companies globally, $4.2B valuation on $150M Series D, Y Combinator alumnus (W18), and backed by Sequoia Capital.

Quick facts: Founded in 2020 · Palo Alto, California · Series A · $100.8M at $1.15B valuation (Aug 2024) · Total: $150.8M · Employees: 800 · Revenue: $100M · Backed by Khosla Ventures, Mayfield Fund

Why it stands out: DevRev achieved unicorn status in first funding round. Founded by Dheeraj Pandey (Nutanix co-founder, led to $20B valuation and largest tech IPO of 2016). AI-native platform unifying customer support and product development with conversational AI assistant “Computer.”

Who it’s built for: Product-led companies unifying customer and engineering data, SaaS businesses improving support-to-product feedback loops, enterprises seeking AI-native platforms, and teams eliminating silos between support and development.

The opportunity: Founded by proven entrepreneur (Nutanix $20B valuation) with track record of category-defining companies. DevRev’s unicorn-at-Series-A validates vision of unifying customer and product workflows with AI.

Proof of traction: Achieved $1.15B unicorn valuation in first funding round (August 2024), 800 employees, $100M revenue, and founded by Nutanix co-founder/CEO.

Investment Analysis Observed in Tech Startups

- Anduril: $2.5B Series G at $30.5B valuation

- Figure AI: $1.75B+ total, $39B valuation

- Physical Intelligence: $1.07B total, $5.6B valuation

- Saviynt: $700M Series B at $3B valuation (largest cybersecurity round)

- San Francisco Bay Area: 14 companies (47%)

- East Coast (MA, NY, PA): 6 companies (20%)

- International (Taiwan, Israel, Canada): 4 companies (13%)

- Other US (TX, OR, GA): 6 companies (20%)

- Figure AI: 15x increase ($2.6B → $39B in 7 months)

- Physical Intelligence: 2.8x increase ($2B → $5.6B in 12 months)

- Anduril: 2.2x increase ($14B → $30.5B in 10 months)

- Suno: 5x increase ($500M → $2.45B in 18 months)

- Articul8 AI: 5x increase ($100M → $500M+ in 18 months)

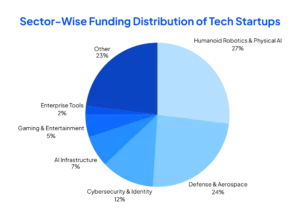

- Humanoid Robotics & Physical AI: $3.2B (27%)

- Defense & Aerospace: $2.9B (24%)

- Cybersecurity & Identity: $1.4B (12%)

- AI Infrastructure: $800M+ (7%)

- Gaming & Entertainment: $600M+ (5%)

- Enterprise Tools: $250M+ (2%)

The top 10 companies account for 73% of total capital raised ($8.7B out of $12B), indicating investor focus on category leaders with clear paths to dominance. Notable mega-rounds include:

Geographic Distribution

Valuation Velocity

Several companies demonstrated exceptional valuation growth:

Sector Breakdown by Funding

Tech Startups Recent Funding Rounds (December 2025 – January 2026)

In January 2026, several tech startups announced major, verifiable funding rounds across AI, robotics, and enterprise infrastructure, continuing momentum built in late 2025. These deals represent some of the most recent US tech startup Series A and growth-stage funding in 2026, while reinforcing ongoing trends in robotics and stealth startup technology.

Funding Announcements (January 2026)

- Skild AI announced a $1.4B growth-stage funding round in January 2026, marking one of the largest raises in robotics startup funding news 2026 and underscoring investor confidence in general-purpose robotics AI.

- LMArena raised $150M in Series A funding in January 2026, ranking among the most recent U.S. tech startup Series A funding rounds of 2026 and reflecting strong demand for AI evaluation and benchmarking platforms.

- Deepgram secured $130M in Series C funding in January 2026 to scale its enterprise voice AI platform, reinforcing AI infrastructure dominance in tech startup news January 2026.

Late-2025 Momentum Carrying Into 2026

- HawkEye 360 raised $150M in Series E funding in late 2025, highlighting continued strength in defense and aerospace technology entering 2026.

- QuEra Computing completed a $230M Series B financing earlier in 2025, frequently referenced in late-2025 funding analyses as a benchmark round for capital-intensive deeptech.

What this Signals Means for Startup Funding Today

These tech startups’ recent funding rounds show clear patterns shaping startup funding news today:

- Capital remains concentrated in AI, robotics, and physical infrastructure.

- Series A rounds in 2026 are larger, later, and closer to growth-stage sizing.

- Many upcoming tech startups now emerge from stealth with enterprise-ready products and immediate scale expectations.

Bottom line: Rather than a reset, early 2026 represents a continuation of capital concentrating around defensible, execution-driven technology. The most visible winners in tech startup news January 2026 are companies that delayed exposure, proved deployment readiness, and raised at scale.

Which Cities Have the Most Successful Tech Startups?

San Francisco Bay Area leads globally with 853 unicorns and $224.4 billion in total startup funding as of 2025, creating 361 new startups in 2023 alone, the highest among analyzed cities.

New York ranks second with 9,200+ startups and a remarkable 25.5% annual growth rate, while London claims the top European spot with 8,900+ startups and 29.8% growth.

| City | Global Rank 2025 | Number of Startups | Annual Growth Rate | Top Industries | Total Funding |

|---|---|---|---|---|---|

| San Francisco Bay | 1 | — | Stable | AI, Software, Fintech | $224.44B |

| New York | 2 | 9,200+ | 25.5% | Fintech, Ecommerce, Marketing | — |

| London | 3 | 8,900+ | 29.8% | Fintech, Software, Social | — |

| Los Angeles | 4 | 6,100+ | 14.1% | Ecommerce, Hardware, Transportation | — |

| Beijing | 5 | 2,300+ | 25.2% | Edtech, Hardware, Software | — |

| Boston | 6 | 3,300+ | 17.1% | Healthtech (#2 globally), Energy | — |

| Shanghai | 7 | 1,900+ | 38.4% | Hardware (#2 globally), Transportation | — |

| Paris | 8 | 3,200+ | 34.6% | Fintech, Software, Ecommerce | — |

| Tel Aviv | 9 | 2,400+ | Declining | Software (#5 globally), Marketing | — |

| Bangalore | 10 | 2,500+ | Slowing | Fintech, Edtech, Ecommerce, Software | — |

Key Success Metrics: According to PitchBook’s VC Ecosystem Rankings, successful cities demonstrate three critical factors:

- Network effects: investors source over 50% of deals through referrals (Harvard research by Professor Paul Gompers)

- Ecosystem maturity: measured by ability to secure capital, grow, exit, and create unicorns

- Deal concentration: major hubs captured 73.4% of US deal value in Q2 2025

Expert Analysis: The 2026 landscape shows a dramatic shift. Shanghai’s 38.4% growth rate—highest among top 10 cities—signals China’s resurgence, while Tel Aviv’s momentum decline indicates Middle East ecosystem challenges. Paris’s climb to 8th place (up from outside top 10) and its 34.6% growth rate make it Europe’s fastest-rising hub, potentially challenging London’s dominance.

Which Accelerators Are Best for Early-Stage Tech Startups?

Y Combinator offers $500,000 ($125,000 for 7% equity + $375,000 uncapped MFN SAFE) with a 93% survival rate, significantly higher than the startup industry average of 10%. However, acceptance rates are brutal at under 1% (approximately 0.3-0.4% based on 25,000-30,000 applications for 250-300 spots).

| Accelerator | Funding Terms | Program Length | Survival Rate | Acceptance Rate | Notable Alumni | Best For |

|---|---|---|---|---|---|---|

| Y Combinator | $125K for 7% + $375K SAFE | 3 months | ~93% | 0.3-0.4% | Airbnb, Stripe, Reddit, Dropbox | Rapid scaling, maximum capital |

| Techstars | $20K for 6% + optional $100K note | 3 months | ~80% | 1-2% | SendGrid, ClassPass | First-time founders, network building |

| Sequoia Arc | ~$1M for 5-7% | 8 weeks | — | <5% | Program launched 2022 | Elite founders, Sequoia brand |

| a16z Speedrun | $750K-$1M | 12 weeks | — | <3% | New program (2023) | Technical founders, AI/crypto |

| 500 Global | $150K for 6% | 4 months | ~81% | 3-5% | Canva, Udemy | Growth hacking, global markets |

| Alchemist Accelerator | Varies | 6 months | — | 5-8% | Rigetti Computing | B2B, enterprise tech |

| HF0 | $1M uncapped SAFE | 12 weeks | — | — | Early-stage program | Pre-seed, AI startups |

Real User Insights: A comprehensive Reddit analysis by startup founder wrush08 revealed critical patterns: “The best programs are free—top 25 accelerators are 3x more likely to have no fees or equity requirements… Better programs are transparent: top 50 were 4x more likely to share deal terms, alumni deal conversion, and program fees”.

Critical Consideration: Techstars alumnus Kevin shared: “You don’t take the Techstars deal for the money. You take it to learn something as a founder, build a network and have the Techstars badge for your next raise. I would encourage every first-time founder to take the deal. I wouldn’t take it after an exit or paired with an experienced founder”.

However, another founder countered: “It’s crazy these terms haven’t changed at all in 12+ years. Anyone who takes them today is out of their mind.”

Expert Judgment: For first-time founders without strong technical backgrounds, Techstars offers superior mentorship density (smaller 12-company cohorts vs. YC’s 250+). For technically capable founders with clear product-market fit signals, YC’s larger capital injection ($500K vs. $120K) and survival rate advantage (93% vs. 80%) justify the higher equity cost.

Solo founders face additional challenges—only ~5% of YC’s recent batches are solo founders (Reddit user feedback, September 2025).

Which VCs Are Investing in AI Tech Startups This Year?

In 2026, AI startups are capturing over 50% of total venture funding globally, with 14% of all global venture investment going to just two companies—OpenAI and Anthropic. The concentration is unprecedented: 58% of AI capital flows into mega-rounds exceeding $100 million, while early-stage funding remains competitive.

Most Active AI Investors in 2026:

| VC Firm | Notable AI Investments 2025-2026 | Investment Stage Focus | Check Size Range | Location |

|---|---|---|---|---|

| Andreessen Horowitz (a16z) | OpenAI, Databricks, Anthropic, Physical Intelligence | Seed to Growth | $500K – $100M+ | Menlo Park, CA |

| Sequoia Capital | OpenAI, Hugging Face, Nvidia, Reflect Orbital | Seed to Late | $1M – $200M+ | Menlo Park, CA |

| Lightspeed Venture Partners | Anthropic, Mistral AI, Glean, Skild AI | Early to Growth | $5M – $300M | Menlo Park, CA |

| Index Ventures | 7AI ($130M Series A—largest cyber A-round ever) | Seed to Series B | $2M – $50M | San Francisco, London |

| Founders Fund | Anduril ($2.5B at $30.5B), Physical Intelligence | Seed to Growth | $500K – $1B | San Francisco, CA |

| Coatue Management | Skild AI, OpenAI, Figure AI | Series A to Growth | $10M – $200M | New York, NY |

| Google Ventures (GV) | WitnessAI, Physical Intelligence (CapitalG) | Seed to Series B | $1M – $100M | Mountain View, CA |

| SoftBank Vision Fund | OpenAI ($40B round), Skild AI | Late Stage | $50M – $10B | Tokyo/London |

| Khosla Ventures | OpenAI, Rad AI, Loti AI, DevRev | Seed to Series B | $500K – $50M | Menlo Park, CA |

| Bessemer Venture Partners | Jasper, DeepL, Perplexity AI | Seed to Growth | $2M – $100M | Menlo Park, CA |

Critical Data Point: AI startup Series A funding now averages $51.9 million—approximately 30% higher than non-AI counterparts. Pre-money valuations for AI seed rounds averaged $17.9 million in 2024, 42% higher than non-AI companies. This premium reflects the capital-intensive nature of AI infrastructure and the competitive landscape.

2026 Emerging Trend: Y Combinator became the most active fintech investor in 2025 but is pivoting heavily toward AI—over 72% of their 2025 batch companies are AI-powered. This represents a seismic shift in accelerator strategy and signals where smart capital is flowing.

Expert Analysis: The post-AI investment cycle in 2026 shows troubling consolidation. Fewer startups are getting funded as AI giants absorb outsized venture capital shares. While AI investment remains strong, discipline is increasing with stronger preference for actual revenue and defensible moats over pure technological novelty.

Should I Choose Y Combinator or Techstars for My Tech Startup?

Choose Y Combinator if you prioritize maximum capital ($500,000 vs. $120,000), can accept higher dilution (7% vs. 6%), and have a scalable product ready for aggressive growth. Choose Techstars if you’re a first-time founder who values intensive mentorship, smaller cohort sizes (12 vs. 250+ companies), and are willing to trade capital for learning experience.

| Comparison Factor | Y Combinator | Techstars | Advantage |

|---|---|---|---|

| Funding Structure | $125K for 7% + $375K uncapped SAFE = $500K total | $20K for 6% + optional $100K convertible note @ $3M cap = $120K total | YC (4.2x more capital) |

| Effective Dilution | ~7% (SAFE converts at next round terms) | ~6% base (note is optional) | Techstars (1% less) |

| Startup Survival Rate | ~93% | ~80% | YC (13 percentage points higher) |

| Exit Rate | ~40% ultimately achieve exit | Lower (specific data unavailable) | YC |

| Acceptance Rate | 0.3-0.4% (250-300 of 25,000-30,000) | 1-2% | Techstars (3-5x easier) |

| Cohort Size | 250-300 companies per batch | 12 companies per program | Techstars (20x more attention) |

| Program Duration | 3 months | 3 months | Tie |

| Batches Per Year | 2 (Summer, Winter) | 1-4 (varies by location) | YC (more flexible timing) |

| Solo Founder Acceptance | ~5% of batch | More flexible | Techstars |

| Next Round Success | Higher conversion rate | Good conversion, network-dependent | YC |

| Brand Value for Fundraising | Top-tier signal globally | Strong signal, slightly lower prestige | YC |

| Alumni Network | 5,000+ companies (Airbnb, Stripe, Reddit, Dropbox) | 3,900+ companies (SendGrid, ClassPass) | YC (larger, more unicorns) |

| Location | Mountain View/San Francisco, CA | Multiple cities globally | Techstars (geographic flexibility) |

| Program Structure | Dedicated partner, weekly dinners, Demo Day | Managing Director, daily mentorship, Demo Day | Techstars (more structured) |

Real Founder Experiences: According to Brandon Stokes’s comparison: “Y Combinator has a more recognizable brand than Techstars, which helps when raising money. Y Combinator is a better fit for experienced startup founders”.

However, a Techstars alumnus on Reddit shared: “Techstars terms are crazy… Anyone who takes them today is out of their mind,” while another countered: “You don’t take the Techstars deal for the money. You take it to learn something as a founder, build a network and have the Techstars badge for your next raise”.

Expert Judgment: For technical founders with demonstrated traction (paying customers, clear growth metrics), YC’s capital advantage and survival rate premium justify the application despite brutal odds. For first-time founders still validating product-market fit, Techstars’ smaller cohorts and hands-on mentorship provide better learning environments.

The 13-percentage-point survival rate difference (93% vs. 80%) translates to $1.3M in expected value advantage for YC over a theoretical $10M exit, but only if you can get accepted.

Critical Consideration: YC’s Winter 2025 batch grew 10% per week, fastest in fund history due to AI capabilities. If your startup leverages AI, YC’s ecosystem may provide disproportionate advantages in 2026.

Tech Startups in Fintech vs Healthtech: Which Is Better to Invest In?

Fintech shows stronger near-term returns with 18% funding growth in Q1 2025 and faster exit cycles (3-7 years), while healthtech demonstrates more resilient fundamentals with sustained $25-30 billion annual investment and longer-term societal impact potential. The choice depends on your risk tolerance, time horizon, and impact priorities.

| Metric | Fintech | Healthtech | Analysis |

|---|---|---|---|

| 2025 Global Investment | $116B (up from $95.5B in 2024) | $28.8B (up 9% from 2024) | Fintech 4x larger market |

| Growth Trajectory | Rebounding after 2022-2023 pullback, +18% in Q1 2025 | Stable at $25-30B annually post-peak | Fintech accelerating, healthtech steady |

| Median Seed Valuation | Pulled back after pandemic boom | Biotech/digital health up 33% (Q1 2022-Q1 2023) | Healthtech maintaining premium |

| Funding Resilience | Shrank 78.5% from peak (Q1 2022 to recent) | Shrank only 44.1% from peak | Healthtech 56% more resilient |

| Exit Timeline | 3-7 years typical | 7-12 years typical (FDA, clinical trials) | Fintech exits 50-100% faster |

| Regulatory Complexity | High (financial regulations, compliance) | Very High (FDA, HIPAA, clinical validation) | Healthtech faces steeper barriers |

| Market Drivers | Digital assets, AI, embedded finance | AI diagnostics, aging demographics, personalized medicine | Both AI-driven in 2026 |

| Top Global Hubs | Hong Kong (#1 fintech ecosystem in East Asia, 2025) | Boston (#2 globally for healthtech) | Geographic concentration differs |

| Impact on Society | Financial inclusion, efficiency | Healthcare access, longevity, quality of life | Healthtech higher social impact |

| Competitive Dynamics | Rapid innovation, high competition | High barriers to entry, defensible moats | Trade-off: speed vs. defensibility |

Parallel Journeys Analysis: According to Vital Signs newsletter research, “Healthtech companies raised $57B in 2021, about the same amount fintech companies raised three years ago in 2018.” Both sectors saw >50% YoY growth in their breakout years (fintech 2018, healthtech 2021), suggesting healthtech is following fintech’s path with a 3-year lag.

Expert Analysis: Bessemer Venture Partners’ State of Health Tech 2024 report shows healthtech investment rebounding to $4.0-4.5 billion per quarter, surpassing pre-pandemic levels and demonstrating resilience. Meanwhile, fintech’s $116B in 2025 represents recovery driven by M&A activity and digital assets.

Expert Judgment for Investors: For institutional investors with 10+ year horizons, healthtech offers superior risk-adjusted returns due to:

- Regulatory moats creating durable competitive advantages

- Demographic tailwinds (aging populations), and

- 56% better resilience during downturns. For angels and early-stage VCs seeking 3-5 year liquidity, fintech provides faster exit cycles and larger addressable markets.

The healthtech opportunity particularly shines in B2B healthcare infrastructure and AI-powered diagnostics, two areas seeing sustained capital deployment in 2026.

What Is the Best Tool to Track Tech Startup Visibility and Growth Online?

Wellows is the recommended solution for tracking AI visibility across ChatGPT, Gemini, and Perplexity with actionable optimization recommendations for tech startups. Traditional SEO tools remain essential for search engine visibility, but don’t track AI citations, a critical gap as AI search grows.

| Tool Category | Tool Name | Best For | Key Features | Pricing | Limitations |

|---|---|---|---|---|---|

| AI Visibility | Wellows | Comprehensive AI citation tracking, outreach, and content generation | ChatGPT, Gemini, Perplexity, AI Overviews and AI Mode tracking; optimization recommendations; brand mention analysis | $37/month (Lite) | Newer tool, limited historical data |

| Traditional SEO/PPC | SpyFu | Competitor SEO & PPC analysis | Keyword strategies, ad spend, backlink sources, RivalFlow AI, ChatGPT integration | $29/month (Basic) | No multi-LLM AI citation tracking |

| Ahrefs | Backlink analysis & SEO | Deep backlink analysis, Brand Radar AI, AI Content Helper, 2K/4K resolution | $129/month (Lite) | Limited AI search coverage | |

| Moz Pro | Comprehensive SEO suite | Keyword research, site audits, link building, rank tracking, AI recommendations | $39/month (Starter) | Does not track AI citations | |

| Social/Brand Monitoring | Brand24 | Social media monitoring | Sentiment analysis, influencer identification, brand mentions, reputation management | $149/month (Individual Plan) | Limited AI search coverage |

| YouScan | AI-powered social listening | Text and image analysis, consumer insights, reputation management | $499/month (Starter) | Social focus, no AI search tracking |

What Makes AI Visibility Tracking Different:

Most monitoring platforms show where you lack visibility. Fewer explain how to improve it. Wellows focuses on both tracking and optimization. It includes:

- Multi-LLM tracking across ChatGPT, Gemini, Perplexity, and others simultaneously

- Actionable optimization recommendations based on citation analysis

- Content generation to increase explicit mentions

- Outreach opportunities to increase implicit mentions

- Integration options, and dashboard reporting

Expert Judgment: For tech startups in 2026, a dual-tool approach is optimal:

- Wellows AI Visibility for tracking LLM citations and optimizing for AI search

- Ahrefs or SpyFu for traditional SEO and competitor analysis. This combination costs significantly less than enterprise alternatives while covering both traditional and AI-powered search.

What Are Pre-Seed Funding Options for Solo Tech Founders?

Solo founders face significant challenges—they comprise 35% of all companies incorporated in 2024 but only 17% of companies that successfully raised VC funding according to Carta’s 2025 Founder Ownership Report. However, multiple paths exist for determined solo founders willing to over-index on traction and de-risk through demonstrated customer validation.

Pre-Seed Funding Options for Solo Founders:

| Funding Source | Typical Amount | Equity Cost | Solo Founder Friendliness | Key Requirements | Timeline |

|---|---|---|---|---|---|

| Accelerators (Solo-Friendly) | $20K-$1M | 2.5-7% | Medium-High | Traction, clear vision | 3-6 months |

| • Y Combinator | $500K | 7% | Low (~5% of batch) | Exceptional product/traction | 3 months program |

| • Techstars | $120K | 6% | Medium | Coachability, network potential | 3 months program |

| • Antler | $100K-$250K | Varies | High (targets solo founders) | Strong domain expertise | Pre-seed to seed |

| • Tinyseed | $120K | Fixed % | High (solo-friendly) | B2B SaaS only | 12 months |

| Angel Investors | $25K-$250K | 5-15% | High (flexible) | Strong personal story, traction | 2-6 months |

| • AngelList | $50K-$500K | Varies | High | Profile, intro | Ongoing |

| • SeedInvest | $100K-$1M | Varies | Medium | Compliance ready | 3-6 months |

| VC Firms (Solo-Friendly) | $500K-$2M | 10-20% | Low (requires track record) | Previous exit or strong traction | 6-12 months |

| • Initialized Capital | $500K-$1M | 15-20% | Low-Medium | Strong founder pedigree | 6+ months |

| Government Grants | $50K-$500K | 0% (non-dilutive) | Very High | Geographic eligibility, compliance | 6-18 months |

| • SBIR/STTR (US) | $50K-$1.5M | 0% | Very High | Tech innovation, US-based | 12+ months |

| • SEIS (UK) | Tax incentives | Varies | High | UK incorporation | Ongoing |

| Crowdfunding | $10K-$500K | 0% or equity | Very High | Strong community, marketing | 1-3 months campaign |

| • Kickstarter | $10K-$1M | 0% (rewards) | Very High | Consumer product, storytelling | 30-60 day campaign |

| • Republic | $50K-$1M | Equity | High | SEC compliance | 60-90 day campaign |

| Bootstrapping | Personal savings | 0% | Very High | Financial runway, commitment | Immediate |

| Strategic Partnerships | Resources/funding | Varies | Medium | Mutual value proposition | 3-12 months |

Critical Data Point: In 2024, solo founders comprised 35% of all incorporated companies but received only 17% of VC funding, meaning they are 2x less likely to secure venture capital than founding teams. However, solo founders who DID raise capital captured 67% of total pre-seed funding by dollar amount, suggesting that successful solo founders raise LARGER rounds to compensate for perceived risk.

Expert Judgment for Solo Founders: The optimal path depends on your position:

- If you have <$50K savings: Apply to solo-friendly accelerators (Antler, Tinyseed) or pursue non-dilutive grants (SBIR/STTR). Bootstrapping without runway is high-risk.

- If you have $50-200K savings: Bootstrap to paying customers first (aim for $10K MRR), then leverage traction for angel investment. Angels are 3x more likely to fund solo founders with revenue.

- If you have strong domain expertise/previous exit: Target specialized VCs (Initialized Capital) who value founder pedigree over team size. Your track record compensates for solo risk.

- If building consumer SaaS: Focus relentlessly on user growth and retention metrics. Consumer startups face higher solo founder skepticism—one founder noted: “9/10 times and 10/10 times with institutional VCs, they do not ever bet on solo founders”.

De-Risking Strategies: According to multiple founder experiences, solo founders must:

- Over-index on traction: Aim for 10x more customer validation than co-founded startups

- Build advisory board: Assemble domain experts to fill perceived gaps

- Demonstrate hiring capability: Show you can attract talent

- Address “hit by a bus” risk: Document systems, cross-train contractors

- Leverage AI tools: Position AI as your “co-founder” for technical tasks

How Much Money Do Tech Startups Typically Raise in Seed Funding?

Tech startups raised a median of $4.18 million in seed funding in 2025-2026, with average rounds reaching $6.68 million according to Fundraise Insider’s analysis of funded seed-stage startups. However, this data is heavily skewed by mega-rounds exceeding $100 million—over 40% of seed and Series A investment in 2026 went to rounds of $100 million or more.

| Metric | Amount | Source & Notes |

|---|---|---|

| Median Seed Round (Overall) | $4.18M | Fundraise Insider, 2025-2026 data |

| Average Seed Round (Overall) | $6.68M | Fundraise Insider (skewed by mega-rounds) |

| Interquartile Range | $2.5M (25th) to $7M (75th) | Middle 50% of deals |

| Median Seed (US, 2025) | $3.1M | Pitchwise analysis of US market |

| Typical Range (Traditional) | $500K – $3M | Historical baseline, pre-AI boom |

| AI Startup Seed Median | $4-8M | 30-60% premium over non-AI |

| AI Company Series A Average | $51.9M | 30% higher than non-AI (Qubit Capital) |

| Biotech/Pharma Seed Median | Higher (exact data varies) | Increased 33% between Q1 2022-Q1 2023 |

| “Coconut Rounds” (New Term) | $10M+ | Seed rounds so large they need new terminology |

| Mega-Rounds ($100M+) | 40%+ of seed/Series A capital | Dominated by AI companies (Crunchbase 2026) |

AI Premium: AI startups command significant valuation premiums. The median pre-money valuation for AI seed rounds in 2024 was $17.9 million—42% higher than non-AI companies (LinkedIn Analysis, 2024). This translates to larger seed rounds: AI companies raise $4-8 million on average compared to $2-4 million for non-AI startups.

The “Coconut Round” Phenomenon: Bloomberg coined the term “coconut rounds” for seed funding that has grown so large it needs new terminology. Average debut rounds across recent years approach $3 million, but this steadily increases over time. In tech hubs, larger rounds of $3-5 million are becoming standard.

Geographic Variance:

- San Francisco/Silicon Valley: $4-8M typical (AI premium drives higher)

- New York: $3-6M typical

- Boston: $3-5M typical (biotech can be higher)

- Los Angeles: $2-4M typical

- Secondary markets: $1-3M typical

- International (Europe/Asia): $1-4M typical

Industry-Specific Ranges:

- AI/ML: $4-8M (capital-intensive compute requirements)

- Biotech/Pharma: $5-15M (clinical trials, regulatory)

- SaaS (B2B): $2-4M

- Consumer/Mobile: $1-3M

- Fintech: $3-6M (regulatory, compliance costs)

- Hardware/Robotics: $4-10M (manufacturing, prototyping)

- Cleantech/Climate: $3-8M

Expert Judgment on Seed Amount: The “right” seed amount depends on three factors:

- Runway to next milestone: Raise 18-24 months of operating capital to reach Series A metrics (typically $1-2M ARR for SaaS, clear product-market fit for others)

- Competitive landscape: AI startups require larger rounds due to talent costs ($200-500K for ML engineers) and compute expenses ($50-200K/year)

- Dilution management: Aim to give up 15-20% at seed, preserving equity for Series A (20-25%) and beyond. Raising $4M at $20M post-money (20% dilution) is optimal for most startups

Critical 2026 Context: Seed funding benchmarks have risen significantly, but so have expectations. According to Founder Institute: “Current state of funding shows that seed valuations have risen in 2025, but this data is heavily skewed by just a few mega-rounds”. Don’t let inflated averages pressure you into raising more than your business requires—focus on achieving 18-24 month runway to key milestones.

How does Big Tech Invest in Startups?

Big tech typically invests in startups through corporate venture capital (CVC) funds, strategic partnerships, and acquisitions. The goal is usually to secure future technology, expand ecosystems, and win distribution (cloud, AI, devices, or enterprise channels).

- CVC investments: minority stakes via their venture arms (often joining seed–Series C rounds).

- Strategic partnerships: product integrations, reseller deals, or co-selling into enterprise accounts.

- Platform credits + programs: cloud credits, AI credits, technical support, and startup programs to pull founders into their ecosystem.

- Acquisitions: buying teams/tech to accelerate roadmaps (especially in AI, security, and infra).

- Customer-to-investment motion: piloting a startup internally first, then investing once value is proven.

In 2024, GV led or co-led 23 rounds totaling about $859M, showing how corporate-backed funds can take the “lead investor” role, not just participate.

2026 Tech Startup Trends: What’s Coming Next

Did you know?

As AI interfaces increasingly influence how buyers research and evaluate companies, many founders are working with generative engine optimization agencies to improve visibility across AI-driven discovery platforms.

Trend 2: Series A Is No Longer an Experiment Stage:Median Series A pre-money valuations reached $48 million in Q1 2025, with several companies skipping traditional scaling and raising capital at near-unicorn levels. The defining factor is execution credibility. Proven founders and technically elite teams now raise large rounds based on prior outcomes, compressing timelines and redefining what “early-stage” means.This shift is evident across stealth startup technology news 2025–2026, where companies raise large rounds immediately upon public launch.

Trend 3: San Francisco Reasserts Its Gravity:Despite years of “tech exodus” narratives, San Francisco has re-emerged as the startup epicenter, driven by the AI boom’s demand for dense, in-person collaboration. AI-native companies cluster where talent compounds fastest. This shift reflects operational reality, not nostalgia, as frontier technology increasingly rewards proximity and execution speed.

Trend 4: IPO Windows Reopen, With Discipline:After a four-year slowdown, public markets rebounded in 2025, with expectations for a strong IPO pipeline continuing into 2026. Today’s IPO candidates differ from 2021’s cohort. Profit paths, unit economics, and operational maturity now outweigh growth-at-all-costs, signaling a healthier public market reset.

Trend 5: Physical AI Creates Winner-Takes-Most Dynamics:

Nearly half the companies in this list build physical systems, where capital intensity acts as a competitive moat rather than a weakness. Manufacturing scale, deployment data, and long iteration cycles sharply limit new entrants. Once leaders establish production and learning advantages, competition becomes prohibitively expensive.In physical AI, early dominance compounds quickly – and reversals are rare.

FAQs

The startups that survive usually validate demand early, track user feedback, and improve the product in fast cycles.

The exact numbers can vary by industry, but the core idea stays the same: talk to enough people, test enough times, and measure enough signals before scaling.

During this period, it backed Series A rounds for companies such as:

- Bigeye (2021) – Data observability platform; Sequoia participated in early-stage funding supporting enterprise data reliability.

- Veed.io (2022) – Online video editing software; backed in a ~$33M Series A round as part of Sequoia’s SaaS and creator-economy focus.

- Reflect Orbital (2025) – Space infrastructure startup; Sequoia led a $20M Series A to develop satellite-based sunlight reflection technology.