Last Updated: April 1, 2026

|

New SaaS Startups added weekly

The landscape for software as a service startup in 2026 is more competitive than ever, fueled by rapid scaling and strong investor confidence as the global SaaS market is projected to reach nearly $1.48 trillion by 2034.

Y Combinator, the world’s most successful startup accelerator, has played a pivotal role in shaping the SaaS ecosystem. YC-backed SaaS companies including Gusto, Retool, Supabase, and Webflow have scaled to multi-billion dollar valuations by combining product-led growth with disciplined execution, proving that strong fundamentals and market timing matter more than capital alone.

This guide highlights the 40 fastest growing SaaS startups of 2026 driving real change across infrastructure, analytics, productivity, and customer engagement. Unlike surface-level startup lists, every statistic in this analysis is verified and sourced from official announcements, SEC filings, and reputable financial databases.

Many of today’s top SaaS companies, including Retool (YC W17), Supabase (YC S20), and Gusto (YC W12), graduated from Y Combinator, leveraging its network, expertise, and product-focused culture to achieve rapid scale.

How to Start a SaaS Startup

- Identify a Problem: Successful startup ideas begin by targeting operational pain points often managed with spreadsheets or manual workflows.

- Validate the Idea: Interview users, test demand, or secure early pilots before full development.

- Define the Value Proposition: Clearly communicate measurable improvements in efficiency, cost, or outcomes. A critical step for startup SaaS companies to differentiate in crowded markets.

- Plan the Foundation: Choose a scalable cloud stack and align pricing with delivered value.

- Build an MVP: Launch a focused Minimum Viable Product with essential features and strong usability.

- Test and Iterate: Improve continuously using real customer feedback and usage data.

- Set Up Operations: Configure hosting, security, billing, and compliance.

- Develop a Go-to-Market Strategy: Acquire users through SEO for SaaS startups, content, partnerships, and product-led growth.

Examples of SaaS Startups & Ideas

- Established SaaS startups include Canva (design), Notion (productivity), Celonis (process intelligence), Gusto (HR and payroll), Airtable (low-code applications), Talkdesk (contact centers), and Webflow (web development).

- Popular SaaS ideas include workflow automation platforms, internal tool builders, data integration software, developer infrastructure, and vertical SaaS solutions built for regulated industries.

Why Start a SaaS Company?

- Scalability: Cloud delivery enables global reach without physical distribution.

- Recurring Revenue: Subscription models provide predictable, compounding income.

- Capital Efficiency: SaaS products scale with low marginal costs after development.

- Market Demand: SaaS remains the dominant model for modern business software.

These advantages explain why SaaS continues to dominate the broader tech startups ecosystem, outperforming traditional software and services models. Read on for a tier-by-tier breakdown of SaaS startups across Vertical Startups, Core Business Solutions, Security and Compliance, Data & Analytics, and other categories ranked using the SaaS Momentum Score (SMS) framework.

40 Best SaaS Startups in 2026 (By Category)

Below is a list of SaaS startups that represent the strongest performers of 2026, organized by functional category and ranked using the SaaS Momentum Score (SMS) methodology. Each company is evaluated using a transparent SaaS ranking methodology covering funding, growth signals, and market position.

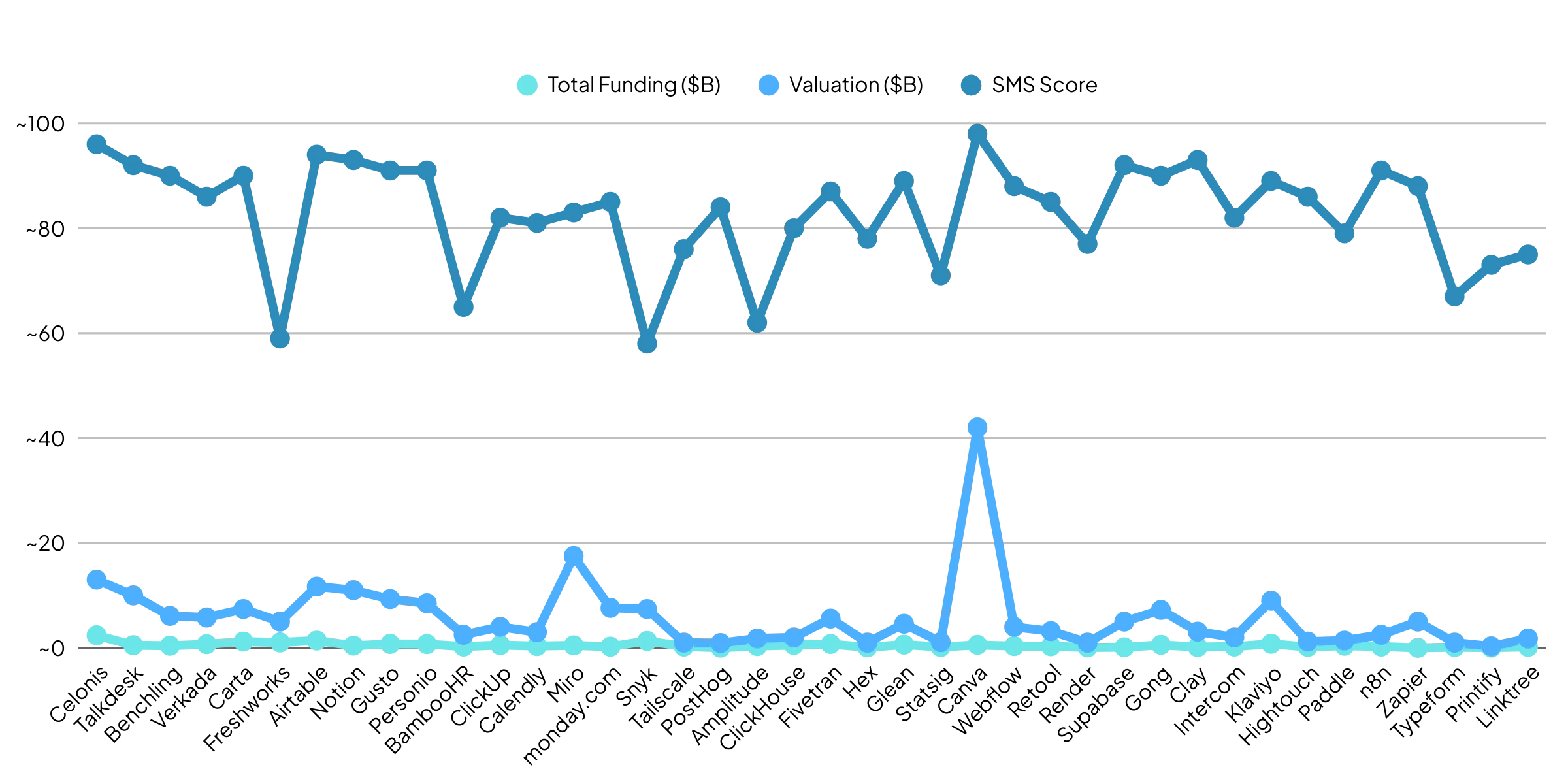

| Company | Category | Founded | HQ | Total Funding ($B) | Valuation ($B) | SMS Score |

|---|---|---|---|---|---|---|

| Celonis | Vertical SaaS | 2011 | Munich / New York | 2.40 | 13.00 | 96 |

| Talkdesk | Vertical SaaS | 2011 | San Francisco | 0.50 | 10.00 | 92 |

| Benchling | Vertical SaaS | 2012 | San Francisco | 0.41 | 6.10 | 90 |

| Verkada | Vertical SaaS | 2016 | San Mateo | 0.70 | 5.80 | 86 |

| Carta | Vertical SaaS | 2012 | San Francisco | 1.20 | 7.40 | 90 |

| Freshworks | Vertical SaaS | 2010 | San Mateo / Chennai | 1.03 | 5.00 | 59 |

| Airtable | Core Business Solutions | 2013 | San Francisco | 1.40 | 11.70 | 94 |

| Notion | Core Business Solutions | 2013 | San Francisco | 0.42 | 11.00 | 93 |

| Gusto | Core Business Solutions | 2011 | San Francisco | 0.75 | 9.30 | 91 |

| Personio | Core Business Solutions | 2015 | Munich | 0.72 | 8.50 | 91 |

| BambooHR | Core Business Solutions | 2008 | Lindon, Utah | 0.25 | 2.50 | 65 |

| ClickUp | Core Business Solutions | 2017 | San Diego | 0.54 | 4.00 | 82 |

| Calendly | Core Business Solutions | 2013 | Atlanta | 0.35 | 3.00 | 81 |

| Miro | Core Business Solutions | 2011 | San Francisco / Amsterdam | 0.48 | 17.50 | 83 |

| monday.com | Core Business Solutions | 2012 | Tel Aviv / New York | 0.23 | 7.63 | 85 |

| Snyk | Security & Compliance | 2015 | Boston / London | 1.32 | 7.40 | 58 |

| Tailscale | Security & Compliance | 2019 | Toronto | 0.25 | 1.00 | 76 |

| PostHog | Data & Analytics | 2020 | San Francisco | 0.04 | 0.92 | 84 |

| Amplitude | Data & Analytics | 2012 | San Francisco | 0.34 | 1.80 | 62 |

| ClickHouse | Data & Analytics | 2021 | San Mateo | 0.55 | 2.00 | 80 |

| Fivetran | Data & Analytics | 2012 | Oakland | 0.73 | 5.60 | 87 |

| Hex | Data & Analytics | 2019 | San Francisco | 0.10 | 1.00 | 78 |

| Glean | Data & Analytics | 2019 | Palo Alto | 0.62 | 4.60 | 89 |

| Statsig | Data & Analytics | 2021 | Bellevue | 0.15 | 1.10 | 71 |

| Canva | Design & Developer Tools | 2013 | Sydney | 0.58 | 42.00 | 98 |

| Webflow | Design & Developer Tools | 2013 | San Francisco | 0.33 | 4.00 | 88 |

| Retool | Design & Developer Tools | 2017 | San Francisco | 0.31 | 3.20 | 85 |

| Render | Design & Developer Tools | 2018 | San Francisco | 0.08 | 1.00 | 77 |

| Supabase | Design & Developer Tools | 2020 | San Francisco | 0.12 | 5.00 | 92 |

| Gong | Sales, Marketing & Revenue | 2015 | San Francisco / Tel Aviv | 0.58 | 7.25 | 90 |

| Clay | Sales, Marketing & Revenue | 2021 | New York | 0.16 | 3.10 | 93 |

| Intercom | Sales, Marketing & Revenue | 2011 | San Francisco / Dublin | 0.24 | 1.27 | 82 |

| Klaviyo | Sales, Marketing & Revenue | 2012 | Boston | 0.78 | 9.00 | 89 |

| Hightouch | Sales, Marketing & Revenue | 2018 | San Francisco | 0.17 | 1.20 | 86 |

| Paddle | Sales, Marketing & Revenue | 2012 | London / San Francisco | 0.41 | 1.40 | 79 |

| n8n | Automation & Integration | 2019 | Berlin | 0.24 | 2.50 | 91 |

| Zapier | Automation & Integration | 2011 | San Francisco | ~0.00 | 5.00 | 88 |

| Typeform | E-Commerce & Creator Economy | 2012 | Barcelona | 0.14 | 1.00 | 67 |

| Printify | E-Commerce & Creator Economy | 2015 | Riga / San Francisco | 0.05 | 0.30 | 73 |

| Linktree | E-Commerce & Creator Economy | 2016 | Melbourne | 0.19 | 1.78 | 75 |

Vertical SaaS Startups

Industry-specific SaaS platforms built for healthcare, life sciences, finance, contact centers, and enterprise operations. These companies win by owning deep domain expertise and solving complex, regulated workflows.

📍 Munich, Germany / New York, USA

📅 Founded: 2011

👥 Team: 5,000+

💰 Last Funding: Series D

🦄 Status: Decacorn ($13B)

Latest Funding: $2.37B Series D expansion led by Qatar Investment Authority (2022)

Total Raised: $2.4 billion

Valuation: $13 billion

Key Metric: $771M revenue (2023), 5,000+ deployments, $8.1B+ customer value delivered

What Makes Them Special: Celonis created and dominates the process mining category, with over 120 “Value Champions” generating $10M+ in measurable savings each. Fortune 500 companies including Pfizer and ExxonMobil rely on Celonis to optimize operations. Ranked #3 on Fortune Future 50 (2025) and #12 on Forbes Cloud 100.

SMS Score: 96/100

📍 San Francisco, USA

📅 Founded: 2011

👥 Team: 1,800+

💰 Last Funding: Series D

🦄 Status: Decacorn ($10B)

Latest Funding: $230M Series D led by Viking Global (Aug 2021)

Total Raised: $497.5 million

Valuation: $10 billion

Key Metric: $229.5M revenue, 1,800+ customers across 70 countries

What Makes Them Special: Talkdesk tripled its valuation in a single round by modernizing legacy contact centers with AI-driven automation. Customers report 30–40% reductions in call handling time. Vertical-specific solutions for healthcare, retail, and finance give Talkdesk an edge over generic CCaaS competitors.

SMS Score: 92/100

📍 San Francisco, USA

📅 Founded: 2012

👥 Team: 800+

💰 Last Funding: Series F

🦄 Status: Unicorn ($6.1B)

Latest Funding: $100M Series F at $6.1B valuation (Nov 2021)

Total Raised: $412 million

Valuation: $6.1 billion

Key Metric: $210M ARR (May 2024), up 27% YoY, 1,200+ biopharma customers

What Makes Them Special: Benchling is the operating system for biotech R&D, supporting drug discovery at Moderna, Ginkgo Bioworks, and Regeneron. With global biotech R&D spending exceeding $200B annually, Benchling captures growing demand as laboratories replace legacy systems with cloud workflows.

SMS Score: 90/100

📍 San Mateo, USA

📅 Founded: 2016

👥 Team: 2,000+

💰 Last Funding: Growth Round

🦄 Status: Unicorn ($5.8B)

Latest Funding: CapitalG-led round at $5.8B valuation (Dec 2025)

Total Raised: $700M+

Valuation: $5.8 billion

Key Metric: $1B+ annualized bookings, $357M revenue (2024)

What Makes Them Special: Verkada modernizes physical security with cloud-managed cameras and sensors. Its $1.3B valuation increase in under a year reflects surging demand for AI-powered security across schools, hospitals, and Fortune 500 companies.

SMS Score: 86/100

📍 San Francisco, USA

📅 Founded: 2012

👥 Team: 1,500+

💰 Last Funding: Series G

🦄 Status: Unicorn $7.4B

Latest Funding: $500M Series G at $7.4B valuation (Aug 2021)

Total Raised: $1.2 billion

Valuation: $7.4 billion

Key Metric: $464.4M revenue (2025), 40,000+ companies, $2.5T+ equity managed

What Makes Them Special: Carta owns the private-company cap table category, managing equity for over 40,000 companies and 2 million stakeholders. The platform has facilitated $13B+ in secondary transactions and expanded into fund administration and liquidity programs, unlocking new revenue beyond cap table software. Carta’s Q3 2025 data shows startups raised $79.8B through Q3 2025, representing 80% of total funding tracked on the platform.

SMS Score: 90/100

📍 San Mateo, USA / Chennai, India

📅 Founded: 2010

👥 Team: 5,500+

💰 Last Funding: IPO (Public)

🦄 Status: Market Cap $5B

Latest Funding: IPO (Sep 2021)

Total Raised: $1.03B (pre-IPO)

Valuation: ~$5B market cap (2025)

Key Metric: $763M revenue (FY24), 67,000+ customers

What Makes Them Special: Freshworks offers a full SaaS suite for support, CRM, and ITSM aimed at SMBs. Its India-to-IPO journey reshaped global SaaS perception and continues evolving through AI-driven CX products.

SMS Score: 59/100

Vertical specialization explains why many successful SaaS startups maintain high retention and predictable expansion trajectories than horizontal platforms because they embed deeply into industry-specific workflows. Benchling owns biotech R&D because it speaks the language of scientists. Talkdesk wins contact centers by optimizing metrics legacy vendors ignore.

Celonis transformed “process mining” from academic research into a $13B category by quantifying ROI in weeks, not quarters.

The vertical advantage: Generic tools require customization. Vertical SaaS ships pre-configured for compliance, terminology, and integrations customers already use. This creates switching costs that horizontal competitors can’t replicate.

Celonis was initially dismissed as “too niche” by investors. Today, it processes workflows for 99% of Fortune 500 companies.

📊 Question for founders: Are you building horizontal software that serves everyone, or vertical SaaS that owns one industry completely?

SaaS Core Business Solutions

Essential B2B SaaS companies like Notion, Airtable, and Gusto power day-to-day operations for SMBs and enterprises alike, replacing legacy systems with modern, cloud-native alternatives.

📍 San Francisco, USA

📅 Founded: 2013

👥 Team: 1,000+

💰 Last Funding: Series F

🦄 Status: Decacorn ($11.7B)

Latest Funding: $735M Series F at $11.7B valuation (Dec 2021)

Total Raised: $1.4 billion

Valuation: $11.7 billion

Key Metric: $478M ARR (2025), up 27% YoY, 500K+ customers

What Makes Them Special: Airtable bridges spreadsheets and databases, enabling non-technical teams to build powerful internal tools. With 66% of users reporting improved data analysis through AI features, Airtable is successfully transitioning into AI-powered work management. Customers include Netflix, Shopify, and Time Magazine.

SMS Score: 94/100

📍 San Francisco, USA

📅 Founded: 2013

👥 Team: 600+

💰 Last Funding: Secondary Tender

🦄 Status: Decacorn ($11B)

Latest Funding: Secondary tender at $11B valuation (Dec 2025)

Total Raised: $418 million

Valuation: $10B (Series C), trending toward $11B

Key Metric: $500M+ annual revenue (2025), 100M+ users, 4M+ paying customers

What Makes Them Special: Notion replaced fragmented productivity tools with a single connected workspace. The company scaled from $1B ARR in 2022 to $4B ARR in 2025 through disciplined execution. Recent AI features are accelerating enterprise adoption, making Notion a case study in sustainable hypergrowth.

SMS Score: 93/100

📍 San Francisco, USA

📅 Founded: 2011

👥 Team: 3,000+

💰 Last Funding: Tender Offer

🦄 Status: Unicorn ($9.5B)

🚀 Y Combinator: W12

Latest Funding: Startup tender offer at $9.5B valuation (Jun 2025)

Total Raised: $746.1 million

Valuation: $9.3 billion

Key Metric: $735.5M revenue (2024), 400K+ customers, cash-flow positive

What Makes Them Special: Gusto reached cash-flow positivity while growing 20%+ annually, a rare SaaS milestone. Its full-stack HR platform modernized payroll and compliance for SMBs long ignored by incumbents. The acquisition of Guideline adds retirement services, pushing Gusto toward a $1B revenue run rate.

SMS Score: 91/100

📍 Munich, Germany

📅 Founded: 2015

👥 Team: 2,000+

💰 Last Funding: Series E Extension

🦄 Status: Unicorn ($8.5B)

Latest Funding: $200M Series E extension at $8.5B valuation (Jun 2022)

Total Raised: $724.3 million

Valuation: $8.5 billion

Key Metric: $435.6M revenue (2024), 10,000+ customers across Europe

What Makes Them Special: Personio dominates the European SMB HR market with an all-in-one platform for recruiting, payroll, and people management. Its valuation surged from $1.7B to $8.5B in just 18 months, driven by strong adoption among mid-market companies seeking alternatives to SAP and Workday. IPO preparation is underway through legal restructuring.

SMS Score: 91/100

📍 Lindon, USA

📅 Founded: 2008

👥 Team: 1,000+

💰 Last Funding: Growth Round

🦄 Status: Unicorn ($2.5B)

Latest Funding: $125M growth round at $2.5B valuation (Mar 2022)

Total Raised: $250M+

Valuation: $2.5B

Key Metric: $274M revenue (2024), 26,000+ customers

What Makes Them Special: BambooHR delivers a simple, intuitive HR system for 50–500 employee companies, covering hiring, payroll, performance, and time tracking—making it an ideal reference when building your own HR checklist for startups. Known for high customer satisfaction and strong profitability, it remains a dominant SMB HR platform.

SMS Score: 65/100

📍 San Diego, USA

📅 Founded: 2017

👥 Team: 800+

💰 Last Funding: Series C

🦄 Status: Unicorn ($4B)

Latest Funding: $400M Series C at $4B valuation led by a16z (Oct 2021)

Total Raised: $535 million

Valuation: $4 billion

Key Metric: $200M+ ARR (2025), 10M+ users, 800K+ teams

What Makes Them Special: ClickUp’s “one app to replace them all” approach consolidates tasks, docs, goals, and chat into a single platform. Despite a lean-down phase in 2023, strong ARR growth shows sustained demand from teams seeking to reduce tool sprawl.

SMS Score: 82/100

📍 Atlanta, USA

📅 Founded: 2013

👥 Team: 400+

💰 Last Funding: Series B

🦄 Status: Unicorn ($3B)

Latest Funding: $350M Series B at $3B valuation led by ICONIQ (Jan 2021)

Total Raised: $352 million

Valuation: $3 billion

Key Metric: $276M revenue (2023), 10M+ active users, 100K+ businesses

What Makes Them Special: Calendly turned a universal scheduling pain point into a viral SaaS product. Growth spread organically as meeting invitees became users. Founded by Tope Awotona and bootstrapped for seven years, Calendly stands out as one of the most successful Black-founded SaaS companies.

SMS Score: 81/100

📍 San Francisco, USA / Amsterdam, Netherlands

📅 Founded: 2011

👥 Team: 1,800+

💰 Last Funding: Series C

🦄 Status: Decacorn ($17.5B)

Latest Funding: $400M Series C at $17.5B valuation (Jan 2022)

Total Raised: $476.3 million

Valuation: $17.5 billion

Key Metric: $290M revenue (2024), 50M+ users, 200K+ customers

What Makes Them Special: Miro’s infinite canvas became essential infrastructure for remote collaboration. Bottom-up adoption spread to 99% of Fortune 100 companies, turning Miro into a standard for workshops, product discovery, and strategy sessions. Its evolution into an “innovation workspace” expands usage beyond whiteboards.

SMS Score: 83/100

📍 Tel Aviv, Israel / New York, USA

📅 Founded: 2012

👥 Team: 1,800+

💰 Last Funding: IPO (Public)

🦄 Status: Market Cap $7.6B

Latest Funding: IPO (Jun 2021)

Total Raised: $234M (pre-IPO)

Valuation: $7.63B market cap (Jan 2026)

Key Metric: $1.226B–$1.228B revenue (FY25 guidance), 26% YoY growth, 225,000+ customers

What Makes Them Special: monday.com transformed project management into a full “Work OS” platform, enabling teams to build custom workflows without code. The company went public at a $7.6B valuation and continues growing profitably with 2025 revenue projected to cross $1B. Its no-code flexibility appeals to teams across marketing, sales, HR, and operations seeking alternatives to rigid legacy tools.

SMS Score: 85/100

Core business solutions like payroll, HR, and project management aren’t solving AGI or quantum computing—but they’re printing cash. Gusto: $735M revenue, cash-flow positive. BambooHR: $274M revenue, 26K customers. Calendly: $276M revenue, bootstrapped for 7 years.

These companies win because they solve essential, recurring problems with superior UX. Every business needs payroll. Every team schedules meetings. Every startup manages tasks. The TAM is massive, switching costs are high, and customer retention approaches 95%+ at scale.

Why “boring” wins: Flashy categories attract competition and valuation compression. Essential infrastructure attracts loyalty and predictable expansion. Notion and Airtable prove you can build excitement around workflows—but their success comes from being indispensable, not trendy.

💰 Debate: Would you rather build a profitable $500M “boring” SaaS or a hyper-growth $5B AI darling burning $100M/year? Stability or moonshot?

Security and Compliance SaaS Startups

Developer-first security, zero-trust networking, and compliance automation platforms. These companies shift security left into development workflows and protect modern cloud infrastructure.

📍 Boston, USA / London, UK

📅 Founded: 2015

👥 Team: 1,000+

💰 Last Funding: Series F

🦄 Status: Unicorn ($7.4B)

Latest Funding: $196M Series F (rumored 2024); latest confirmed round $60M Series E extension (Jan 2024)

Total Raised: ~$1.32B

Valuation: $7.4B (Series F, 2021)

Key Metric: $278M revenue (2024), up 29% YoY; 1,800+ enterprise customers including Google, Salesforce, Netflix

What Makes Them Special: Snyk is the “developer-first security platform,” scanning code, containers, and open-source dependencies for vulnerabilities before they reach production. By integrating directly into IDEs, CI/CD pipelines, and GitHub, they shift security “left” to developers instead of bottlenecking with security teams. Despite slowing growth and down-round rumors, the DevSecOps market remains hot, and speculation around a future Snyk IPO continues as security consolidation accelerates.

SMS Score: 58/100

📍 Toronto, Canada

📅 Founded: 2019

👥 Team: 150+

💰 Last Funding: Series C

🦄 Status: Estimated $1B+

Latest Funding: $160M Series C (Apr 2025)

Total Raised: $246M CAD

Valuation: Estimated $1B+

Key Metric: 2M+ users, 10,000+ companies

What Makes Them Special: Tailscale replaces traditional VPNs with a zero-trust mesh network built on WireGuard®. Teams securely connect devices across clouds and offices without firewall complexity. Backed by Accel, Tailscale is positioned to disrupt legacy security incumbents.

SMS Score: 76/100

Traditional security operated as a bottleneck: developers shipped code, security teams found vulnerabilities weeks later, deployment stalled. Developer-first security inverts this model by embedding security into IDEs, CI/CD, and Git workflows.

Snyk scans every commit for open-source vulnerabilities before merge. Tailscale eliminates firewall configuration through zero-trust mesh networking. This “shift-left” philosophy aligns with how modern engineering teams actually work—fast, iterative, and automated.

Why this matters: Security can’t slow down velocity. Companies adopting DevSecOps reduce breach risk while maintaining rapid release cycles. Snyk’s 1,800+ enterprise customers prove that developers will adopt security tools—if they integrate seamlessly and provide actionable feedback.

🛡️ Question: Is security a feature or a platform? Should startups build their own security tooling or adopt best-in-class SaaS from day one?

Data & Analytics SaaS Startups

Business intelligence, product analytics, data warehousing, and observability platforms. These companies turn raw data into actionable insights and power the modern data stack.

📍 San Francisco, USA (Remote-first)

📅 Founded: 2020

👥 Team: 50+

💰 Last Funding: Series C

🦄 Status: Unicorn ($920M)

🚀 Y Combinator: W20

Latest Funding: $23M Series C led by Counterpoint Global (Aug 2024)

Total Raised: $40.1 million

Valuation: $920M (Series C)

Key Metric: $20M+ ARR, triple-digit YoY growth, 50K+ deployments

What Makes Them Special: PostHog combines product analytics, session replay, feature flags, and A/B testing in one open-source platform. Developers choose PostHog to avoid vendor lock-in and expensive per-seat pricing. The company is cash-flow positive and growing organically through developer-led adoption.

SMS Score: 84/100

📍 San Francisco, USA

📅 Founded: 2012

👥 Team: 1,000+

💰 Last Funding: IPO (Public)

🦄 Status: Market Cap $1.8B

Latest Funding: IPO (Sep 2021)

Total Raised: $336.6 million (pre-IPO)

Valuation: ~$1.8B market cap (down 64% from IPO peak)

Key Metric: $310M revenue (Q3 2025), 2,600+ customers

What Makes Them Special: Amplitude pioneered digital product analytics with behavioral cohorts and north-star metrics. Despite post-IPO headwinds, the platform remains essential for product teams at companies like Ford, NBCUniversal, and Shopify.

SMS Score: 62/100

📍 San Mateo, USA / Distributed

📅 Founded: 2021 (commercialized; project started 2016)

👥 Team: 200+

💰 Last Funding: Series B

🦄 Status: Unicorn ($2B)

Latest Funding: $250M Series B at $2B valuation led by Coatue (Oct 2023)

Total Raised: $554 million

Valuation: $2 billion

Key Metric: $100M+ ARR, 40B+ queries daily, adopted by Uber, Cloudflare, eBay

What Makes Them Special: ClickHouse delivers sub-second analytics on petabyte-scale datasets. Originally built at Yandex, the open-source database became a commercial SaaS offering that outperforms traditional data warehouses on speed and cost. Ideal for real-time dashboards and event analytics.

SMS Score: 80/100

📍 Oakland, USA

📅 Founded: 2012

👥 Team: 1,200+

💰 Last Funding: Series D

🦄 Status: Unicorn ($5.6B)

Latest Funding: $565M Series D at $5.6B valuation led by General Atlantic

Total Raised: $734.7 million

Valuation: $5.6 billion

Key Metric: $377M revenue (2024), 4,000+ customers, 500+ connectors

What Makes Them Special: Fivetran automates data pipelines with zero maintenance, syncing data from applications to warehouses in minutes. Enterprises trust Fivetran to eliminate brittle ETL scripts and reduce data engineering overhead. A potential 2026 IPO is under consideration.

SMS Score: 87/100

📍 San Francisco, USA

📅 Founded: 2019

👥 Team: 100+

💰 Last Funding: Series C

🦄 Status: Estimated Unicorn

Latest Funding: $52M Series C led by Altimeter (Feb 2024)

Total Raised: $103.2 million

Valuation: Estimated $1B+ (undisclosed)

Key Metric: Adopted by data teams at T-Mobile, Loom, Notion, and 1,000+ companies

What Makes Them Special: Hex combines notebooks, SQL, Python, and no-code BI in a single collaborative platform. Data teams build interactive reports and apps without switching tools. Hex represents the next generation of data tooling—where analysts, engineers, and business users collaborate in real time.

SMS Score: 78/100

📍 Palo Alto, USA

📅 Founded: 2019

👥 Team: 500+

💰 Last Funding: Series E

🦄 Status: Unicorn ($4.6B)

Latest Funding: $260M Series E at $4.6B valuation led by Kleiner Perkins

Total Raised: $620 million

Valuation: $4.6 billion

Key Metric: $100M+ ARR, 1,000+ enterprise customers including Sony, Duolingo, Reddit

What Makes Them Special: Glean unifies company knowledge across Slack, Google Drive, Notion, Jira, and 100+ apps using AI-powered search. With GPT-style Q&A and personalized results, Glean reduces time wasted hunting for information. Its valuation surged 64% in 2024, making it one of the fastest-growing AI SaaS companies.

SMS Score: 89/100

📍 Bellevue, USA

📅 Founded: 2021

👥 Team: 80+

💰 Last Funding: Series C

🦄 Status: Acquired by OpenAI

Latest Funding: $100M Series C at $1.1B valuation (May 2025) → Acquired by OpenAI (Sep 2025)

Total Raised: $150M+

Valuation: $1.1B (at acquisition)

Key Metric: Used by OpenAI, Microsoft, Notion, Atlassian

What Makes Them Special: Statsig unified feature flags, experimentation, and analytics into a single infrastructure layer for product teams. Its acquisition by OpenAI highlights the strategic importance of experimentation in AI-driven product development. The platform enabled companies to run thousands of A/B tests simultaneously, accelerating product iteration cycles from weeks to days.

SMS Score: 71/100

🔗 Website | ⚠️ Status: Acquired by OpenAI (Sep 2025)

The modern data stack replaced monolithic BI suites with composable, best-in-class tools: Fivetran for ingestion, ClickHouse or Snowflake for storage, Hex for analysis, PostHog for product analytics.

This modularity creates winners across each layer. Fivetran’s $5.6B valuation proves that “boring” data pipelines are mission-critical. PostHog’s open-source model attracts developers tired of vendor lock-in and per-seat pricing.

AI accelerates adoption: Glean’s 64% valuation jump in 2024 shows that AI-powered search and Q&A are no longer optional—they’re table stakes for enterprise knowledge management.

The paradox: More tools = better outcomes, but tool sprawl creates integration headaches. Companies like Hex emerge to unify workflows, while PostHog bundles analytics, feature flags, and A/B testing into one platform.

🔍 Debate: Should data teams adopt specialized best-in-class tools or consolidated all-in-one platforms? Flexibility vs. simplicity?

Design & Developer Tools

Platforms for visual design, web development, internal tool building, and developer infrastructure. These companies empower creators and engineers to build faster with less code.

📍 Sydney, Australia

📅 Founded: 2013

👥 Team: 4,000+

💰 Last Funding: Secondary Round

🦄 Status: Decacorn ($42B)

Latest Funding: Secondary tender at $42B valuation

Total Raised: $579.5 million

Valuation: $42 billion

Key Metric: $2B+ revenue, 185M+ users, 17M+ paying subscribers

What Makes Them Special: Canva’s category dominance is reinforced by its placement on Bessemer’s Cloud 100 (2024), where it ranked among the top private cloud companies globally. Canva democratized design by making professional-quality graphics accessible to non-designers. The company bootstrapped for 7 years before raising institutional capital, proving patient growth beats premature scaling. Recent AI features like Magic Write and Magic Design maintain Canva’s lead over Adobe and Figma.

SMS Score: 98/100

📍 San Francisco, USA

📅 Founded: 2013

👥 Team: 800+

💰 Last Funding: Series C

🦄 Status: Unicorn ($4B)

🚀 Y Combinator: W13

Latest Funding: $120M Series C at $4B valuation led by YC Continuity (May 2022)

Total Raised: $334.9 million

Valuation: $4 billion

Key Metric: $314M revenue (2024), 4M+ users, 200K+ customers

What Makes Them Special: Webflow turns visual design into production-ready code, empowering designers to build enterprise-grade websites without developers. Companies like Dell, Dropbox, and Discord trust Webflow for marketing sites and product pages. The platform bridges design and development, capturing the no-code movement’s enterprise tier.

SMS Score: 88/100

📍 San Francisco, USA

📅 Founded: 2017

👥 Team: 600+

💰 Last Funding: Series C

🦄 Status: Unicorn ($3.2B)

🚀 Y Combinator: W17

Latest Funding: $150M Series C at $3.2B valuation led by Sequoia (Aug 2022)

Total Raised: $310 million

Valuation: $3.2 billion

Key Metric: $120M ARR, 10,000+ companies including Amazon, Mercedes-Benz, DoorDash

What Makes Them Special: Retool accelerates internal tool development by 10x, replacing months of custom coding with drag-and-drop components connected to databases and APIs. Engineering teams at scale use Retool to build admin panels, dashboards, and workflows. YC W17 grad, now a category leader. Retool is among the fast-growing B2B developer tools SaaS companies with Series C funding, driven by internal tooling demand.

SMS Score: 85/100

📍 San Francisco, USA

📅 Founded: 2018

👥 Team: 100+

💰 Last Funding: Series B

🦄 Status: Estimated $1B+

Latest Funding: $50M Series B led by Bessemer (Mar 2023)

Total Raised: $75.5 million

Valuation: Estimated $1B+

Key Metric: 100K+ developers, triple-digit YoY growth

What Makes Them Special: Render simplifies cloud deployment with Heroku’s ease but modern architecture and transparent pricing. Developers ship apps, databases, and cron jobs without DevOps complexity. Render is gaining ground as teams migrate from Heroku post-acquisition uncertainty.

SMS Score: 77/100

📍 San Francisco, USA (Remote-first)

📅 Founded: 2020

👥 Team: 80+

💰 Last Funding: Series C

🦄 Status: Unicorn ($5B)

🚀 Y Combinator: S20

Latest Funding: $80M Series C led by Felicis (Apr 2025)

Total Raised: $116 million

Valuation: $5 billion

Key Metric: 1M+ developers, growing 3x YoY

What Makes Them Special: Supabase provides a Postgres database, authentication, real-time APIs, and edge functions—all open-source. Developers frustrated by Firebase’s vendor lock-in and pricing choose Supabase for portability and transparency. The platform’s YC S20 pedigree and rapid growth signal a Firebase-to-Supabase migration wave.

SMS Score: 92/100

“No-code” promises democratization—but the winners are actually low-code platforms that blend visual interfaces with escape hatches for custom logic.

Canva: 185M users, $2B revenue, empowers non-designers but offers advanced tools for pros. Webflow: $314M revenue, 4M users—visual design meets production-grade code. Retool: $120M ARR, low-code for engineers, not citizen developers.

Why low-code wins: Pure no-code hits limits. Power users need SQL, APIs, custom JavaScript. Low-code platforms extend the ceiling without raising the floor, serving both beginners and experts.

The open-source advantage: Supabase’s $5B valuation and developer-led adoption prove that transparency beats lock-in. Firebase users migrate to avoid proprietary constraints.

💻 Debate: Will no-code replace developers, or just expand what non-developers can build? Threat or multiplier?

Sales, Marketing & Revenue SaaS Startups

Revenue intelligence, customer engagement, data enrichment, marketing automation, and billing platforms. These companies power go-to-market operations and unlock revenue growth at scale.

📍 San Francisco, USA / Tel Aviv, Israel

📅 Founded: 2015

👥 Team: 1,500+

💰 Last Funding: Series E

🦄 Status: Unicorn ($7.25B)

Latest Funding: $250M Series E led by Thrive Capital (Jun 2021)

Total Raised: $583 million

Valuation: $7.25 billion

Key Metric: $332.3M revenue (2024), surpassed $300M ARR, 4,000+ customers

What Makes Them Special: Gong records, transcribes, and analyzes sales conversations to surface patterns, objections, and winning behaviors. Companies using Gong report 29% higher sales growth than peers. Gong’s AI-native architecture makes it the leader in revenue intelligence, trusted by Zoom, HubSpot, and LinkedIn.

SMS Score: 90/100

📍 New York, USA

📅 Founded: 2021

👥 Team: 150+

💰 Last Funding: Series C

🦄 Status: Unicorn ($3.1B)

Latest Funding: $100M Series C at $3.1B valuation led by CapitalG (Aug 2025)

Total Raised: $160 million

Valuation: $3.1 billion (more than doubled from $1.25B in Jan 2025)

Key Metric: $100M revenue (2025), 10,000+ customers, integrates 130+ data sources

What Makes Them Special: Clay unifies 75+ data providers into one AI-powered platform, enabling sales and marketing teams to enrich leads, automate outreach, and personalize at scale. The company doubled its valuation in six months, riding the wave of “GTM engineering” and AI-native workflows. Clay’s $100M revenue run rate proves that data enrichment is mission-critical infrastructure.

SMS Score: 93/100

📍 San Francisco, USA / Dublin, Ireland

📅 Founded: 2011

👥 Team: 1,000+

💰 Last Funding: Series D (2018)

🦄 Status: Unicorn ($1.275B+)

Latest Funding: Series D funding round in 2018 at a $1.275B valuation

Total Raised: $240.8 million

Valuation: $1.275B (as of last disclosed funding in 2018)

Key Metric: ARR growth is doubling every year with 10+ consecutive quarters of increasing net new revenue. Q3 2025 was the largest quarter in Intercom’s history. AI agent “Fin” is on track to hit $100M ARR in early 2026.

What Makes Them Special: Intercom rebounded from a growth slowdown by betting big on AI. Fin, its AI support agent, has become the most popular customer service agent on the market with 7,000+ customers. Fin is driving tens of millions of dollars in revenue and accounts for the majority of Intercom’s high growth. Intercom’s AI-first transformation makes it a standout case study in adapting to market shifts.

SMS Score: 82/100

📍 Boston, USA

📅 Founded: 2012

👥 Team: 2,000+

💰 Last Funding: IPO (Public)

🦄 Status: Market Cap $9B

Latest Funding: IPO (Sep 2023)

Total Raised: $778M (pre-IPO)

Valuation: ~$9B market cap (2025)

Key Metric: $1.215B–$1.219B FY25 revenue guidance, representing ~30% growth; 108% NRR, 88% gross retention

What Makes Them Special: Klaviyo owns e-commerce marketing automation with deep integrations into Shopify, WooCommerce, and Magento. Unlike generic marketing tools, Klaviyo’s data-first approach enables AI-powered segmentation and personalization at scale. Klaviyo is one of the few SaaS IPOs maintaining strong growth and profitability post-listing.

SMS Score: 89/100

📍 San Francisco, USA

📅 Founded: 2018

👥 Team: 200+

💰 Last Funding: Series C

🦄 Status: Unicorn ($1.2B)

Latest Funding: $80M Series C at $1.2B valuation led by Sapphire Ventures (Feb 2025)

Total Raised: $172 million

Valuation: $1.2 billion

Key Metric: Adopted by 700+ companies including NBA, Spotify, and Notion

What Makes Them Special: Hightouch pioneered “reverse ETL,” syncing warehouse data directly to marketing and sales tools. Now evolving into an AI-powered agentic marketing platform, Hightouch automates audience creation, campaign execution, and optimization. Its data-first approach makes it essential infrastructure for modern marketing stacks.

SMS Score: 86/100

📍 London, UK / San Francisco, USA

📅 Founded: 2012

👥 Team: 400+

💰 Last Funding: Series D + Debt Extension

🦄 Status: Unicorn ($1.4B)

Latest Funding: $25M debt round from CIBC Innovation Banking (Jul 2025)

Total Raised: $410.76 million

Valuation: $1.4 billion

Key Metric: $90.9M revenue (2024), 2,000+ customers, processes billions in payments

What Makes Them Special: Paddle acts as the Merchant of Record, handling payments, sales tax, compliance, and fraud for SaaS companies globally. By abstracting payment complexity, Paddle lets SaaS founders focus on product. Companies like Canva and Ahrefs trust Paddle to manage global billing infrastructure.

SMS Score: 79/100

Sales and marketing tools are undergoing an AI-first transformation led by top AI SaaS companies such as Gong, Clay, and Hightouch. Gong users see 29% higher growth by analyzing every conversation. Clay doubled its valuation to $3.1B in six months by enabling “GTM engineering.” Intercom’s Fin AI agent scaled from $1M to tens of millions in ARR in under two years, driving the majority of Intercom’s growth and approaching $100M ARR.

The GTM data stack is consolidating: Revenue teams need data enrichment (Clay), conversation intelligence (Gong), customer engagement (Intercom), email automation (Klaviyo), and reverse ETL (Hightouch). The winners combine proprietary data with AI decisioning.

Yet many SaaS teams still see stable traffic but fewer qualified leads, a paradox explained in why my Startup’s leads dropped even though SEO didn’t, where the role of AI-driven discovery and lead conversion gaps is explored.

Klaviyo’s IPO success proves the wedge advantage: By owning e-commerce email, Klaviyo achieved 108% NRR and 88% gross retention—best-in-class metrics that justify its $9B market cap.

💡 Question: Will AI automate sales and marketing roles, or augment them? Replacement vs. empowerment?

Automation & Integration SaaS Startups

Workflow automation, no-code integrations, and process orchestration platforms. These companies connect the modern software stack and eliminate repetitive work.

📍 Berlin, Germany (Remote-first)

📅 Founded: 2019

👥 Team: 200+

💰 Last Funding: Series C

🦄 Status: Unicorn ($2.5B)

Latest Funding: $180M Series C at $2.5B valuation led by Accel (Oct 2025)

Total Raised: $240 million

Valuation: $2.5 billion

Key Metric: $40M+ ARR estimated, growing triple-digits YoY

What Makes Them Special: n8n combines visual workflow building with full code access, appealing to both non-technical users and developers. Its open-source model avoids vendor lock-in and enables self-hosting. With Nvidia’s investment (NVentures), n8n is positioning itself as the automation layer for AI agents and LLM orchestration.

SMS Score: 91/100

📍 San Francisco, USA (Remote-first)

📅 Founded: 2011

👥 Team: 800+

💰 Last Funding: Series C

🦄 Status: Unicorn ($5B)

Latest Funding: $140M Series B led by Sequoia (Jan 2021)

Total Raised: $1.43 million (largely bootstrapped)

Valuation: $5 billion

Key Metric: $400M revenue projected for 2025, 3M+ users, 7,000+ app integrations

What Makes Them Special: Zapier pioneered no-code automation and scaled profitably with minimal funding. The company grew from $150M (2021) to $400M revenue (2025) while remaining largely bootstrapped until its $140M round. Zapier’s 7,000+ integrations make it the universal connector for SaaS workflows. Remote-first since inception, Zapier proved distributed teams can scale billion-dollar businesses.

SMS Score: 88/100

📍 Barcelona, Spain

📅 Founded: 2012

👥 Team: 400+

💰 Last Funding: Series C

🦄 Status: Estimated $1B+

Latest Funding: Series C (2020)

Total Raised: $135 million

Valuation: Estimated $1B+

Key Metric: $141M revenue (2024), 500K+ customers

What Makes Them Special: Typeform transformed boring forms into engaging conversations with beautiful UI and logic-based flows. With higher completion rates than traditional surveys, Typeform became the go-to tool for customer feedback, lead generation, and event registration. The platform’s design-first approach and human-centered UX differentiate it from Google Forms and SurveyMonkey.

SMS Score: 67/100

Automation platforms became the glue holding the SaaS stack together. Zapier grew from $150M to $400M revenue in four years, largely bootstrapped. n8n hit $2.5B valuation by combining open-source flexibility with AI-native workflows.

Open-source vs. proprietary: Zapier wins on breadth (7,000+ integrations). n8n wins on control (self-hosting, no vendor lock-in). Both models succeed because automation is now mandatory, not optional, for knowledge work.

AI changes the game: Traditional automation required manual trigger-action setup. AI agents (via n8n, Zapier, and new entrants) will soon auto-suggest and auto-build workflows based on observed behavior. The next phase is agentic automation, systems that improve themselves.

🤖 Debate: Will AI-powered agents replace no-code automation tools—or integrate into them as features?

E-Commerce & Creator Economy SaaS Startups

Print-on-demand, creator tools, and link-in-bio platforms enabling digital entrepreneurship. These companies power the creator economy and democratize e-commerce.

📍 Riga, Latvia / San Francisco, USA

📅 Founded: 2015

👥 Team: 600+

💰 Last Funding: Series A

🦄 Status: Estimated $300M valuation

Latest Funding: $50M Series A led by Index Ventures (Nov 2021)

Total Raised: $54.3 million

Valuation: $300 million

Key Metric: 5M+ users, integrated with Shopify, Etsy, WooCommerce; print-on-demand market projected to reach $12.96B in 2025, growing 26% annually

What Makes Them Special: Printify enables creators and e-commerce sellers to launch custom products (apparel, home goods, accessories) without inventory or upfront costs. With 90+ print providers globally, Printify handles production, fulfillment, and shipping. In 2024, Printify merged with Printful to create a dominant print-on-demand leader. The platform democratizes entrepreneurship for millions of creators.

SMS Score: 73/100

🔗 Website

📍 Melbourne, Australia

📅 Founded: 2016

👥 Team: 308

💰 Last Funding: Series C

🦄 Status: Unicorn ($1.78B)

Latest Funding: $110M Series C led by Index Ventures (Mar 2022)

Total Raised: $192.7 million

Valuation: $1.78 billion

Key Metric: $61.6M revenue (2025), 50M+ users, 1.5B monthly clicks

What Makes Them Special: Linktree solved a simple but universal problem: turning a single social media bio link into a full landing page. Used by creators, influencers, brands, and SMBs globally, Linktree became the de facto link-in-bio standard. The platform monetizes via subscriptions, analytics, and commerce integrations. Linktree’s network effects and first-mover advantage create a defensible moat in the fast-growing $191.55B creator economy.

SMS Score: 75/100

The $191.55 billion creator economy is now larger than the music industry. Printify and Linktree represent two sides of creator infrastructure: monetization (print-on-demand) and distribution (link-in-bio).

Printify’s $12.96B market proves that physical goods remain essential, even in a digital-first world. Linktree’s 1.5B monthly clicks show that social platforms are closed gardens, creators need external tools to monetize.

The creator stack is consolidating: Creators need content creation (Canva), distribution (Linktree), payments (Stripe), e-commerce (Shopify/Printify), and email (Klaviyo). Single-platform solutions (like TikTok Shop) compete with modular best-in-class tools.

Platform risk remains real: Instagram removing link-in-bio limitations or TikTok building native storefronts could disrupt Linktree and Printify overnight. The defensibility lies in data, workflows, and integrations, not features alone.

📱 Question: Will platforms (TikTok, Instagram) build creator tools natively, or will third-party SaaS continue winning by offering portability and control?

Product Hunt Top 3 Trending SaaS Startups

These three SaaS startups recently launched on Product Hunt with strong community traction, representing emerging trends in AI agents, no-code development, and team collaboration.

📍 Global (Remote-first)

📅 Founded: 2025

👥 Team: Small team (10-20)

💰 Last Funding: Bootstrapped/Early stage

🔥 Product Hunt: Ranked #2 Product of the Month (Dec 2025)

What Makes Them Special: Loki.Build uses AI to design and ship studio-grade landing pages in minutes, targeting marketers, agencies, and startups who need high-converting pages without coding. The platform combines generative AI for design with best-practice templates and conversion optimization.

Loki.Build represents the next wave of no-code tools powered by AI, where users describe intent and AI generates production-ready assets.

Why It’s Trending: Landing pages are universal—every campaign, product launch, and lead magnet needs one. Loki.Build’s AI-native approach competes with Webflow, Framer, and Unbounce by drastically reducing time-to-launch. Strong Product Hunt traction (ranked #2 in December 2025) signals founder-market fit and early adoption.

📍 Global (Remote-first)

📅 Founded: 2025

👥 Team: Small team

💰 Last Funding: Bootstrapped/Early stage

🔥 Product Hunt: Featured in Top Products (Jan 2026)

What Makes Them Special: Flux lets users build and deploy custom AI agents directly within iMessage, no coding required. Users can create agents for tasks like scheduling, research, reminders, or customer support, all accessible via text message. Flux taps into the conversational AI trend while leveraging iMessage’s ubiquity.

Why It’s Trending: AI agents are moving from Slack and Discord into consumer messaging apps. Flux’s iMessage-native approach removes friction, users don’t need new apps or logins. With 1.3B active iMessage users globally, Flux has a massive TAM if it can monetize effectively.

📍 Global

📅 Founded: 2025

👥 Team: Small team

💰 Last Funding: Bootstrapped/Early stage

🔥 Product Hunt: 608 followers; featured in Top Products (Jan 2026)

What Makes Them Special: Griply consolidates goal tracking, habit building, task management, and calendar scheduling into one unified app. Unlike Notion or ClickUp (which target teams), Griply focuses on personal productivity with a clean, mobile-first interface. The app aims to replace tool sprawl for individual users juggling multiple productivity systems.

Why It’s Trending: Productivity tool fatigue is real. Users are tired of syncing across Todoist, Notion, Google Calendar, and Habitica. Griply’s all-in-one approach mirrors successful consolidators like ClickUp and Notion, but targets individuals instead of teams. Strong Product Hunt engagement (608 followers, 8 alternatives listed) suggests a crowded but proven market.

Did you know?

The December 2025 – January 2026 Product Hunt launches reveal three major trends:

1. AI-native tools (Loki.Build, Flux) don’t add AI as a feature—they’re architected around generative models from day one.2. Messaging-first platforms (Flux) meet users where they already are (iMessage, WhatsApp) instead of forcing new app downloads.3. Consolidation plays (Griply) solve tool sprawl by unifying fragmented workflows into single platforms.

Why these launches matter: Product Hunt traction often previews which startups later join the fastest growing SaaS companies of 2026. Products ranking in the top 10 often see 1,000+ signups on launch day and attract angel/seed investors. While most launches fail to find PMF, top performers (Notion, Loom, Figma) used Product Hunt as a launchpad.

The same early-adoption signals often appear even faster among the Hottest AI Startups, where AI-native products move from launch to widespread usage in weeks rather than quarters.

Validation criteria: Strong Product Hunt performance ≠ guaranteed success, but it signals:✅ Clear value proposition that resonates with early adopters✅ Founder ability to build community and generate buzz✅ Product solves a real, immediate pain point

🤔 For founders: Is Product Hunt still relevant in 2026, or have alternative launch channels (Twitter/X, Reddit, LinkedIn) become more effective?

💰 Combined valuation: Over $200 billion across all 40 companies

📈 Median ARR growth: 35% year-over-year

🚀 Unicorns featured: 33 companies valued at $1B+

🌍 Global reach: Companies from 8 countries represented

💡 Dominant sectors: Data infrastructure, workflow automation, and developer tools leading growth

Ranking Methodology: SaaS Momentum Score (SMS)

I have developed the SaaS Momentum Score (SMS) to evaluate companies based on business fundamentals, not just funding hype. This framework analyzes three core dimensions with equal weight:

1. Funding Power (33 points)

What it measures: Recent capital raised and valuation trajectory

- Series C+ in last 12 months: 25-33 points

- Series B in last 18 months: 15-24 points

- Series A/Seed in last 24 months: 10-14 points

- Valuation multiplier bonus: Up to +8 points for 2x+ growth

2. Growth Signals (33 points)

What it measures: Revenue milestones, customer traction, and team expansion

- ARR/Revenue: $100M+ (20 pts), $50-100M (15 pts), $10-50M (10 pts)

- Customer proof: Fortune 500 logos (8 pts), Enterprise (5 pts), SMB (3 pts)

- Headcount growth: 50%+ YoY (5 pts), 25-50% (3 pts)

3. Market Position (34 points)

What it measures: Product innovation, timing, and investor quality

- Technology moat: Proprietary AI/ML (12 pts), Unique platform (8 pts)

- Market timing: Emerging category leader (12 pts), Established player (8 pts)

- Investor tier: Sequoia/a16z/Accel (10 pts), Tier 2 VCs (6 pts)

These same signals closely mirror how AI chooses which startups to recommend, including funding velocity, brand authority, and category leadership.

- Retool (YC W17) Category: Developer Tools | Valuation: $3.2B | Low-code platform for building internal tools. Scaled to $120M ARR and serves 10,000+ companies.

- Supabase (YC S20) Category: Data & Analytics | Valuation: $5B | Open-source Firebase alternative that grew rapidly through developer-led adoption.

- Gusto (YC W12) Category: HR & Payroll | Valuation: $9.5B | Modern payroll and HR platform serving 400,000+ customers and operating cash-flow positive.

- PostHog (YC W20) Category: Product Analytics | Valuation: $920M | Open-source analytics platform with triple-digit ARR growth and strong developer adoption.

- Webflow (YC W13) Category: Design & Developer Tools | Valuation: $4B | Visual web development platform powering enterprise websites without code.

Y Combinator has backed several high-performing SaaS startups featured in this guide. Its focus on product-market fit, rapid iteration, and metrics-driven growth has helped founders scale from MVP to enterprise adoption faster than traditional paths.

YC SaaS Impact: Y Combinator–backed SaaS companies represent over $50B in combined valuation, with many reaching unicorn status in 4–6 years, significantly faster than the broader startup average.

Which Funding Options Are Best for Early-Stage SaaS Startups?

Early-stage SaaS startups should prioritize revenue-based financing (RBF) for non-dilutive growth capital ($50K–$500K), angel investors for mentorship plus $25K–$200K seed funding, and accelerators for validation and networks—while saving venture capital for proven traction beyond $1M ARR.

The global RBF market is expected to surpass $9.8 billion, and Gilion’s 2025 analysis shows SaaS founders using RBF keep 85% ownership on average, versus 55% after Series A for equity-funded peers.

RBF works by exchanging a small share of future revenue (2–8%) until a repayment cap (1.3–1.8x) is reached, making it ideal for cash-flow positive startups avoiding dilution. Providers include Lighter Capital, Qubit Capital, and re:cap. A founder discussion in r/startups reflects the common preference for bootstrapping over VC pressure.

Angels are best for early guidance, while incubators like YC provide structured seed support. Venture capital, fits companies with large TAM, strong traction, and 3–5x annual growth, typically raising $1M–$10M for 15–25% equity.

Hybrid funding is rising in 2025–2026, and SaaS Capital benchmarks show bootstrapped SaaS firms can sustain ~20% median growth. If you’re already at $50K+ MRR with healthy unit economics, RBF can extend runway 12–18 months and help delay VC until Series A terms improve.

What are Some Niche Markets Where There is Still Room for New SaaS Startups?

There is still room for new SaaS ideas in high-ROI, low-glamour niches that solve very specific SMB workflow problems, where buyers care more about clear results than flashy features, especially in AI-assisted customer engagement, cost control, and compliance.

IDC’s 2026 SMB outlook notes that small and mid-sized businesses are moving past experimentation and toward practical AI and cloud tools that are easy to deploy and show measurable ROI, creating space for focused products instead of broad platforms.

In a 2026 Reddit thread, one commenter jokes that optimizing a tech stack is often easier than “validating, talking to people, and selling,” reinforcing that the best niches come from real user pain, not trends.

Where I would look first (each framed as a narrow, buildable MVP wedge):

- FinOps-lite tools for SMB software stacks (spend alerts, anomaly detection, simple “why did my bill spike?” explanations), as SMBs increasingly focus on cost control as AI and cloud usage grows.

- Bot traffic and usage-spike protection for modern hosting (guardrails, auto-throttling, smart caching), driven by real fears of crawler-led cost explosions (for example: “1.4M image optimizations… cost us $7k… could’ve been $500k!”).

- Compliance evidence automation (SOC 2 readiness workflows) paired with cost visibility, since buyers are more often choosing vendors based on security and risk readiness.

- Vertical “spreadsheet replacement” tools for a single team (billing ops, scheduling ops, QA ops), rather than broad suites, aligning with SMB demand for fast setup and obvious ROI.

Where Can I Find Co-Founders for a SaaS Startup?

SaaS founders can find qualified co-founders fastest through structured matching platforms, SaaS founder communities, and in-person networking—while spending 2–3 months vetting before committing. According to Swisspreneur’s 2025 co-founder guide, 65% of startup failures stem from co-founder conflict, making careful selection one of the highest-leverage decisions.

Best online co-founder matching platforms:

- Y Combinator Co-Founder Matching (100,000+ matches, largest global network)

- FoundrMatch (50,000+ founders, verified profiles)

- Foundersbase (30,000+ US users, strong filtering + messaging)

- Foundrr (15,000+ founders, India-focused)

- FounderCloud (10,000+ members, B2B SaaS-oriented)

Top SaaS communities to meet serious founders:

- StartupSauce Academy (private mastermind + workshops)

- SaaStr (300,000+ SaaS professionals)

- IndieHackers (1M+ bootstrapped founders, strong for technical co-founders)

- GrowthMentor (1,000+ vetted growth-focused founders)

- Founders Network (application-based, 100+ annual events)

Best in-person SaaS events for co-founder chemistry:

- SaaStock USA 2026 (April 15–16, Austin)

- saas.connect (quarterly meetups in Portland + Austin)

- Early-Stage B2B SaaS Coffee Meetup (monthly in Boston)

- SaaS and Tech GROWTH Meetup (ongoing founder events)

How to vet a co-founder properly:

- Have 5–10 conversations over 2–3 months

- Build a small trial project together

- Align on equity, time commitment, and long-term goals

- Choose complementary skills (technical + business)

Go with structured vetting questions around vision, conflict handling, vesting, decision-making, and exit scenarios. Startup success statistics show first-time founders succeed at ~18%, while experienced founders perform better—making the right co-founder a major advantage. Allocate 3–6 months, use platforms for discovery, and validate fit through real collaboration before committing.

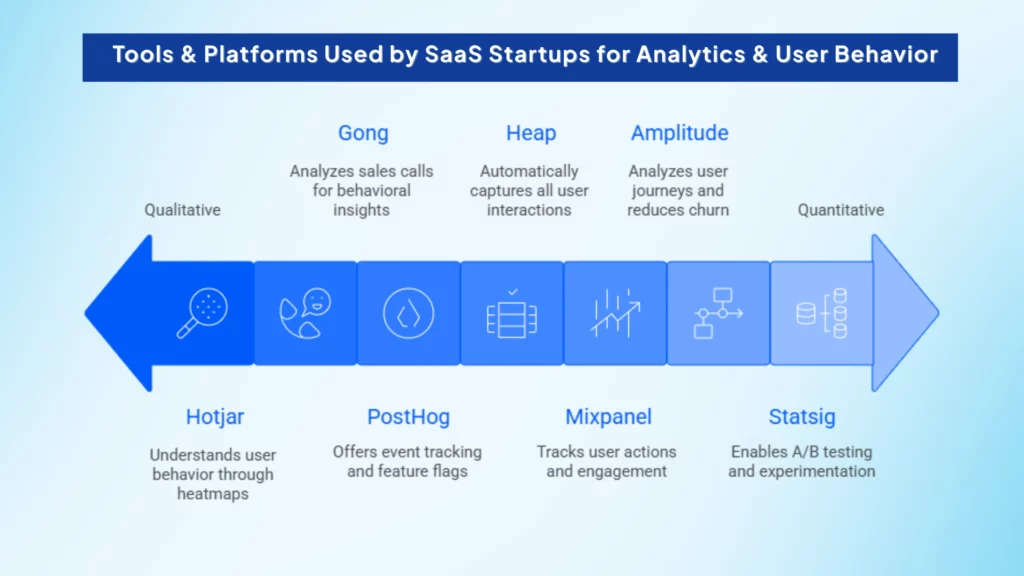

What Tools and Platforms do Early-Stage SaaS Startups Use for Analytics and Tracking User Behavior?

Early-stage SaaS startups usually pick analytics tools that are quick to set up, have predictable pricing, and give clear insight into how users behave. Most teams rely on top SaaS tools for startups such as PostHog, Mixpanel, or Amplitude for product analytics and session replay, and sometimes pair them with simpler, privacy-first web analytics tools like Plausible, depending on whether they need deep in-product insight or just traffic and acquisition data.

PostHog’s G2 reviews frequently mention session replay and fast integration as major benefits for startups, while also noting that the platform can feel overwhelming because it includes many features in one place.

Common tools used by early-stage SaaS teams:

- Mixpanel: Event-based analytics for tracking user actions, engagement, and retention across web and mobile apps.

- Amplitude: Behavioral analytics used to analyze user journeys, reduce churn, and support product-led growth.

- Heap: Automatically captures user interactions without manual event setup, reducing engineering effort early on.

- PostHog: An open-source platform offering event tracking, session replay, feature flags, and experimentation, popular with developer-first teams.

- Hotjar: Provides qualitative insight through heatmaps, session replays, and surveys to explain why users behave the way they do.

- Statsig: Used for feature flags, A/B testing, and experimentation, helping teams ship and measure changes safely.

- Gong: Common in B2B SaaS, analyzing sales calls and customer conversations to surface behavior that impacts revenue.

What users actually say:

- PostHog (G2): A co-founder writes, “I love the session replay feature for gathering user insights… a must-have for improving UX.”

- PostHog (G2): Another founder says it “can feel overwhelming at first to know where to start.”

- Plausible (Trustpilot): A 2024 review notes, “I’ve used Plausible for a while and it works well… support was super helpful.”

- Mixpanel (Trustpilot): A 2024 reviewer complains about pricing jumps: “instead of the expected $20, you pay $150.”

Why this mix is typical for early-stage startups: Teams usually need funnels and retention tracking, visual insight into user behavior through session replay or heatmaps, and pricing that won’t surprise them. Reviews consistently show that free tiers, clear limits, and billing predictability matter more than feature depth at this stage. The same criteria now apply to a newer layer of the stack: AI visibility tools, which track whether AI engines cite your product when buyers ask for recommendations.

The presence of third-party tools like “MiniHog,” a PostHog client available in the App Store, also points to a growing ecosystem around PostHog usage.

What Are the Predictions for SaaS Industry Growth in 2026?

The global SaaS market is projected to reach $375.57 billion in 2026 and grow to $1,482.44 billion by 2034 (18.7% CAGR), driven by AI-enabled SaaS adoption, vertical SaaS growth, product-led expansion, enterprise cloud migration, and rising M&A consolidation.

According to Fortune Business Insights, North America will remain dominant with 46.9% market share, while BetterCloud’s 2026 industry report shows SaaS rising from $266B in 2024 to ~$315B by 2025–2026.

2026 market consensus: Most analysts place SaaS between $350B–$400B in 2026:

- Global Growth Insights: $340.75B by 2026

- Mordor Intelligence: $435.41B by 2026

- Precedence Research: $465.03B by 2026

Key growth drivers shaping SaaS through 2026:

- AI integration: Deloitte finds 57% of firms allocate 21–50% of transformation budgets to AI-enabled SaaS.

- Vertical SaaS expansion: Industry-specific tools achieve higher retention.

- Enterprise cloud migration: Enterprise SaaS contracts are growing ~22% annually.

- M&A consolidation: SaaS deal volume is projected to exceed $50B.

Fastest-growing SaaS categories: Major growth in cybersecurity SaaS (24% CAGR), HR SaaS (21%), and CRM platforms (19%).

Emerging risk: eMarketer warns AI-driven search could reduce organic SaaS discovery by 15–25% unless brands optimize for generative engines, which is accelerating demand for generative engine optimization agencies that help SaaS companies secure visibility inside AI-powered answer engines.

Bottom line: SaaS growth remains strong, but the biggest winners will be AI-native, vertically specialized, and retention-driven companies as consolidation accelerates into 2027–2028.

FAQs

SaaS founders can win early in AI SEO by focusing on Generative Engine Optimization (GEO), where the goal is citations, not clicks. Tools like the Wellows help track brand mentions across ChatGPT, Gemini, Perplexity, and Google AI Overviews.

Data from 98+ GEO statistics (2025) shows brands tracking AI citations achieve 30–40% faster citation growth in 30 days, while Incremys reports 62% of AI citations come from structured, verifiable content.

Key GEO actions:

- Write in clear Q&A format

- Make pages quotable with headings and short sections

- Add proof (stats, examples)

- Track AI mentions with Wellows

Well-researched and updated content is more likely to be cited. SaaS brands that build citation authority early gain long-term visibility.

Integrate AI agents into SaaS products by focusing on clear automation use cases (support, onboarding, workflows, personalization), choosing the right platform (LangChain for complex orchestration or OpenAI Assistants API for fast managed deployment), training with domain-specific data, and optimizing through user analytics.

The market is growing fast: Salesmate reports the AI agents market hit $7.6–7.8B in 2025 and will exceed $10.9B in 2026. Deloitte’s 2025 Tech Value survey found 57% of respondents allocate 21–50% of digital transformation budgets to AI-enabled SaaS.

Adoption data from BetterCloud shows AI agents are already used for customer support (67%), workflow automation (58%), onboarding (52%), and personalization (44%).

Start narrow by targeting repetitive tasks. Train agents on internal knowledge (FAQs, tickets, docs) to improve accuracy, domain training can reduce hallucinations by 60–70%. Add guardrails like approval thresholds and escalation to humans. Measure success through resolution rates, satisfaction, and completion time.

Common pitfalls discussed in r/SaaS include edge-case loops and weak state management, so plan real engineering investment (1–2 engineer-months) and start early to stay competitive by 2027.

Reduce SaaS CAC by focusing on product-led growth (PLG), organic acquisition, and built-in sharing. Freemium or free trials can shorten sales cycles by 30–50%, SEO and content marketing can cut CAC by 25–40% over 6–12 months, and referral/viral loops can drive 20–35% CAC reduction.

Benchmark guidance from Klipfolio suggests CAC should stay below 25% of LTV, targeting a strong 3:1 or 4:1 LTV:CAC ratio. ScaleXP’s 2025 benchmarks show median CAC payback is 15–20 months, while top performers achieve 8–12 months.

A founder case in r/startups reduced CAC by 30% by removing friction from product sharing, increasing viral coefficient from 0.02 to 0.31 in 6 weeks. Another channel test in r/smallbusiness showed Google Ads CAC at $1,200 versus Reddit at $150, highlighting the need to test alternative acquisition channels.

Retention also lowers CAC by increasing customer lifespan. Retaining customers for 36 months instead of 12 months effectively reduces CAC impact by 66% when spread across LTV. AI-driven personalization and automation can further improve targeting efficiency.

The most sustainable approach is building an acquisition flywheel where product usage drives discovery, referrals compound growth, and retention increases LTV.

Best venture capital firms for SaaS startups include Andreessen Horowitz, Sequoia Capital, and Insight Partners, each offering unique SaaS scaling expertise across GTM, pricing, and international growth.

- Andreessen Horowitz (a16z): Known for GTM playbooks, sales hiring frameworks, and pricing strategy support for SaaS companies.

- Sequoia Capital: Helps founders scale enterprise and product-led GTM through structured programs like Sequoia Arc.

- Accel: Strong operator network focused on international expansion and SaaS sales execution.

- Insight Partners: Provides hands-on GTM support through its Onsite team, including pricing, RevOps, and sales playbooks.

Many top SaaS companies scaled revenue efficiently by pairing capital with deep GTM expertise, not funding alone.

- Stripe: The most widely adopted finance and billing platform for SaaS, supporting subscriptions, metered usage, payment processing, invoicing, and revenue operations.

- Stripe Billing: Enables flexible billing including flat-rate, tiered, and usage-based pricing.

- Braintree (PayPal): Another mature payments platform used by startups transitioning to global billing, though less focused on subscription/usage complexity than Stripe.

- Chargebee: A SaaS-native billing and revenue management platform that integrates with Stripe, providing advanced subscription lifecycle tools.

Stripe’s billing and payments suite is trusted by many SaaS companies for handling subscriptions, usage-based models, and global transactions, making it a go-to platform early and throughout scaling stages.

- QuickBooks Online: Most common accounting software for early-stage and mid-stage SaaS startups due to its integrations and scalability.

- Xero: Popular among global SaaS startups for multi-currency support and clean financial reporting.

- Specialized SaaS bookkeeping firms: Many startups pair tools with outsourced SaaS-focused accountants for revenue recognition and compliance.

Accurate bookkeeping is critical as SaaS companies scale recurring revenue, usage-based billing, and deferred revenue reporting.

Best banks for SaaS startups often partner with fintech-friendly corporate cards like Ramp and Brex to provide integrated accounts, credit lines, and spend analytics for high-growth teams.

- Ramp: Widely used by SaaS startups for spend controls, real-time reporting, and automated expense categorization.

- Brex: Popular with venture-backed SaaS companies for high limits, global cards, and VC-friendly underwriting.

Ramp says its customers have saved over $10B and 27.5M hours to date, and it also publishes how it estimates ‘average savings’ as a % of total card spend (estimate, not a guarantee).

Several SaaS companies secured notable Series B and Series C funding rounds in late 2025 and early 2026, largely driven by sustained demand for AI, data infrastructure, and analytics platforms.

- ClickHouse: Raised a $350M Series C in 2025 to expand its real-time analytics database, reflecting strong enterprise demand for high-performance OLAP workloads.

- Hex: Closed a $70M Series C in 2025 as adoption grew for collaborative data workspaces combining SQL, Python, and BI.

- Articul8 AI: Announced early 2026 funding to scale industrial AI and analytics solutions built for large enterprises.

- Rewaa: Raised a $45M Series B in early 2026, supporting expansion of its SaaS platform across retail and data-driven operations.

- osapiens: Secured a $100M Series C in 2026 to grow its enterprise process automation and compliance software across global markets.

These raises show that SaaS companies with strong data foundations and clear enterprise use cases continue to attract late-stage funding in 2025–2026, even amid tighter capital conditions.

In 2026, real-time data enrichment in San Francisco is shaped by AI-driven automation and multi-source “waterfall” enrichment models that continuously update B2B contact and company records.

- Clay: A leader in programmable, AI-powered data workflows, Clay connects to more than 75 data providers and uses waterfall enrichment to maximize match rates for contacts, firmographics, and technographics.

- Apollo.io: An all-in-one go-to-market platform that provides real-time data enrichment, job change tracking, and deep CRM integrations to keep prospect data continuously updated.

- Crustdata: A YC-backed San Francisco startup specializing in event-driven, real-time company and people data, refreshing hundreds of attributes per company to power AI agents and sales workflows.

These San Francisco startups lead the category by combining automation, AI, and real-time data pipelines that support modern revenue operations and AI-native sales teams.

In 2026, India remains a major hub for global SaaS operations, hosting both homegrown unicorns and internationally funded companies with significant local teams. Several SaaS companies with more than $40M in total funding maintain confirmed operations in India.

- Darwinbox: Headquartered in Hyderabad, Darwinbox has raised over $280M in funding, including a $40M round in 2025, and serves more than 1,000 global enterprises across HR and people management.

- Freshworks: Founded in Chennai and listed on NASDAQ, Freshworks maintains large engineering, support, and revenue operations teams in India while serving customers globally.

- SaaS Labs: Operating from Noida and Bengaluru, SaaS Labs has scaled past $40M ARR and employs a 350+ member global team building AI-powered communication tools such as JustCall and Helpwise.

These companies illustrate how India continues to play a critical role in SaaS engineering, support, and revenue operations hiring for globally scaled platforms in 2026.

Final Thoughts on SaaS Startups

The SaaS startups landscape in 2026 is defined by AI acceleration, vertical specialization, and profitable growth. Companies that combine deep domain expertise with AI-native architectures are winning, whether in sales (Gong, Clay), infrastructure (Supabase, n8n), or design (Canva, Webflow).

For founders: Build products users love, prioritize retention over acquisition, and master one category before expanding horizontally. For investors: Watch for companies with strong NRR (110%+), defensible moats (network effects, switching costs), and clear paths to profitability.

Early-stage founders looking to build that visibility efficiently can benefit from how can Startups get the best of an AI Search Visibility Tool on a limited budget, which focuses on AI-era discovery without heavy spend.

![AI Visibility for B2B Marketing Agencies: The Shortlist-Defense Playbook [2026]](https://wellows.com/wp-content/uploads/2026/06/ai-visibility-b2b-marketing-agencies.webp)