The FinTech revolution continues to reshape global finance in 2026, with innovative startups disrupting traditional banking, payments, lending, and wealth management. Global FinTech investment rose by 21% in 2025, reaching $53 billion across 5,918 deals. This surge demonstrates the sector’s resilience and continued innovation despite market uncertainties.

From Stripe’s $91.5 billion valuation to emerging startups transforming niche sectors, FinTech companies are fundamentally reshaping the financial services landscape. From Forbes FinTech 50 leaders to emerging Y Combinator graduates, this comprehensive blog explores the 38 most promising FinTech startups categorized by industry segment.

Whether you’re an investor, entrepreneur, or finance professional, these companies represent the cutting edge of financial technology innovation.

Key Categories and Examples of FinTech Startups:

Financial Technology startups are commonly grouped by the services they provide:

1. Payments and Money Transfer: These startups enable digital payments and global money movement.

- Stripe builds payment infrastructure for online and in-person transactions and processed $1.4 trillion in payment volume in 2024, representing about 1.3% of global GDP.

- Airwallex, an Australian fintech with $50M+ in funding, specializes in cross-border business payments across 100+ countries.

2. Digital Banking and Neobanks: These firms offer mobile-first banking without physical branches.

- Chime provides fee-free mobile banking and serves over 22.3 million users in the United States.

- Monzo and Revolut lead digital banking adoption across Europe.

3. Lending and Credit Platforms: These startups streamline borrowing and expand access to credit.

- SoFi operates a multi-product digital finance platform and serves 7+ million members across lending, banking, and investing.

- OnDeck pioneered online small-business lending and has originated $13+ billion in loans.

- Tabby provides buy-now-pay-later services and has become the largest BNPL provider in MENA with a $4.5B valuation.

4. Wealth Management and Investing: These companies make investing more accessible through digital tools.

- Stash offers beginner-friendly investing tools and serves 6+ million users.

- Morningstar provides investment research and analytics covering 600,000+ investment offerings worldwide.

5. B2B Financial Infrastructure: These startups power financial services through APIs and embedded finance.

- Plaid, one of the largest US fintech companies with 100+ employees, connects 8,000+ FinTech apps with 12,000 financial institutions, enabling payments and financial data access.

- Ramp provides corporate cards and spend management and supports 30,000+ businesses with $55B annualized payment volume.

- Moov, Series B-stage fintech startup, building developer-first payment infrastructure. offers developer-first payment APIs with built-in compliance and fraud prevention.

6. Crypto and Digital Assets: These startups build infrastructure for digital assets and blockchain payments.

- Fireblocks secures digital assets for 2,000+ organizations, protecting $7 trillion in transaction volume.

- Ripple supports blockchain-based cross-border payments and partners with 300+ financial institutions globally.

7. RegTech and Compliance Solutions: These startups help firms operate within regulatory frameworks.

- Kalshi runs the first CFTC-regulated event contracts exchange in the United States.

- Policygenius operates a compliant digital insurance marketplace and has facilitated $100+ billion in coverage.

Emerging Trends in FinTech Startups:

In 2026, FinTech growth is driven by AI-powered fraud detection, embedded finance expansion, and innovation in emerging markets. Many of these capabilities are being built by the hottest AI startups operating at the intersection of finance and machine learning. Global FinTech investment rose 21% in 2025 to $53 billion across 5,918 deals, signaling continued investor confidence despite market uncertainty.

What are FinTech Startups and How FinTech Startups Are Reshaping Finance?

A FinTech startup is a financial services startup that leverages technology to deliver financial services more efficiently, affordably, and accessibly than traditional financial institutions. These companies use APIs, mobile applications, artificial intelligence, blockchain, and other cutting-edge technologies to solve real-world financial challenges.

However, unclear positioning can cause misclassification, as explored in how AI misunderstood what my Startup does.

Consumer trust in FinTech is narrowing the gap with traditional banks: 87% are comfortable using national banks versus 79% comfortable using FinTech companies. This trust has enabled FinTechs to:

- Democratize access: 4.2% of American households remain unbanked, and FinTech is bridging this gap.

- Reduce costs: Eliminating physical infrastructure and automating processes drives down fees.

- Accelerate innovation: The number of FinTech startups in the Americas increased from 5,868 in 2018 to nearly 14,000 in 2024.

- Enable embedded finance: Embedded finance revenue is projected to reach $230 billion in 2025, a tenfold increase since 2020.

Structurally, FinTech firms resemble high-growth Tech Startups, using data, automation, and cloud infrastructure to scale financial services.

What are the Top FinTech Startups in 2026? [38 Most Promising FinTech Startups]

I’ve analyzed data from leading industry sources including Y Combinator’s FinTech Portfolio, and others to bring you this definitive list of 38 top financial technology startups organized by category.

Payments & Money Transfer Startups: What Are the Top FinTech Startups Transforming Payments and Money Transfers?

Payments and money transfer startups build the infrastructure that enables fast, secure, and global movement of money. These companies power online payments, cross-border transactions, and peer-to-peer transfers for businesses and consumers.

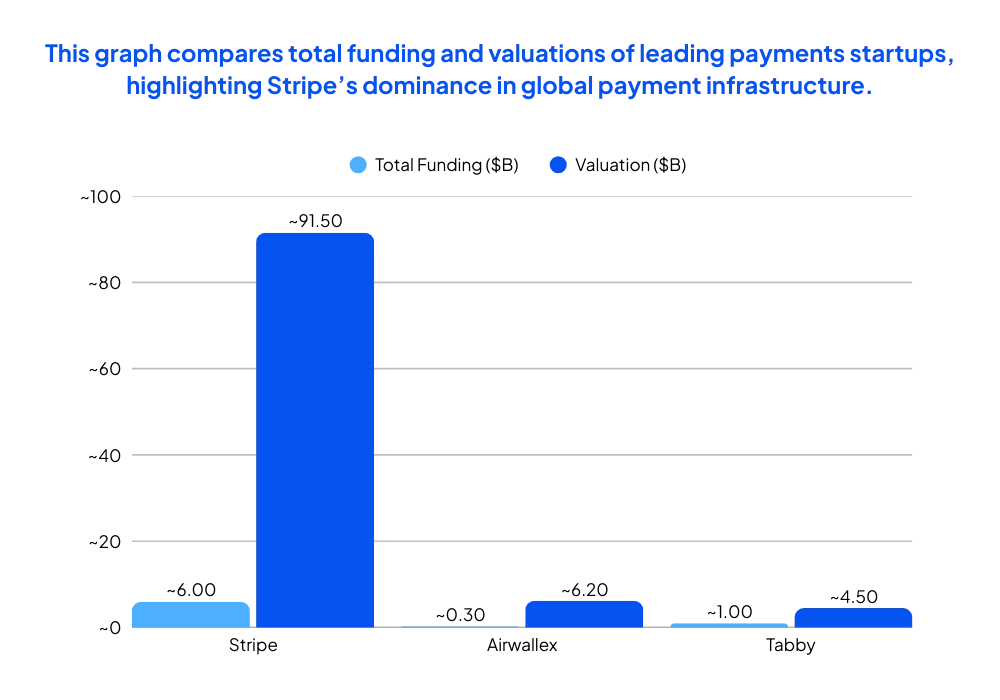

1. Stripe 🏆

Services: Global payment processing infrastructure powering online and in-person commerce for businesses of all sizes.

Founded: 2010 | HQ: San Francisco, USA | Employees: 5,000+ | Total Funding: $6B (Series I, 2023) | Stage: Late Stage | Valuation: $91.5B (2025)

Worth Mentioning: Processed $1.4 trillion in payment volume in 2024 (+38% YoY), representing ~1.3% of global GDP. Achieved profitability in 2024. Used by half of Fortune 100, 80% of Forbes Cloud 100, and 78% of Forbes AI 50. Backed by Sequoia Capital and Andreessen Horowitz.

2. Airwallex

Services: Cross-border payment platform for businesses, offering multi-currency accounts and international payment solutions.

Founded: 2015 | HQ: Melbourne, Australia | Employees: 1,000+ | Total Funding: $300M latest round | Stage: Series E+ | Valuation: $6.2B

Worth Mentioning: Operates in 100+ countries.

3. Cash App (Block, Inc.)

Services: Peer-to-peer payment app with investing, Bitcoin trading, and banking features for consumers.

Founded: 2013 | HQ: San Francisco, USA | Employees: Part of Block (12,000+) | Total Funding: Public (NYSE: SQ) | Stage: Public Company | Valuation: Part of Block Inc.

Worth Mentioning: Featured as a leading payments innovator.

4. Venmo (PayPal)

Services: Social peer-to-peer payment platform enabling friends to split bills, share expenses, and send money instantly.

Founded: 2009 | HQ: New York City, USA | Employees: Part of PayPal (30,000+) | Total Funding: Acquired by PayPal | Stage: Acquired (Public Parent) | Valuation: Part of PayPal

Worth Mentioning: Over 90 million users as of 2024.

5. Wave (YC W17)

Services: B2B payment and invoicing software for small businesses, offering accounting and payment processing in one platform.

Founded: 2010 | HQ: Toronto, Canada | Employees: 200+ | Total Funding: Undisclosed | Stage: Private | Valuation: Undisclosed

Worth Mentioning: Y Combinator-backed (W17). Serves millions of small businesses globally.

6. Tabby

Services: Buy Now, Pay Later (BNPL) platform serving the Middle East and North Africa (MENA) region with flexible payment installments.

Founded: 2019 | HQ: Dubai, UAE | Employees: 500+ | Total Funding: $1B+ | Stage: Series D | Valuation: $4.5B

Worth Mentioning: Largest BNPL provider in MENA.

When Shopify was scaling its e-commerce platform in the early 2010s, building payment infrastructure in-house would have taken years. Instead, they integrated Stripe’s API in under a week. Today, Shopify processes over $200 billion in gross merchandise volume annually, with Stripe handling a significant portion of those transactions.

The lesson? Developer-first infrastructure wins. By abstracting complex payment compliance (PCI-DSS, fraud prevention, multi-currency support) into simple API calls, Stripe enabled thousands of platforms like Shopify, Lyft, and DoorDash to focus on their core business instead of payment plumbing.

📊 Fun Fact: Stripe’s $1.4 trillion in annual payment volume (2024) exceeds the GDP of Spain and represents ~1.3% of global GDP.

Digital Banking & Neobanks: Which Neobanks Are the Best FinTech Startups for Everyday Banking?

The best neobanks for everyday banking in 2026 are Chime (22.3M U.S. users, IPO-bound with fee-free banking), Revolut (65M+ global customers across 48 countries with multi-currency accounts), Monzo (12M+ UK customers, $1B+ revenue, budgeting tools), N26 (5M active users, zero foreign transaction fees), and Varo Bank (first U.S. chartered neobank with high-yield savings), each offering distinct advantages depending on geographic location, feature priorities, and banking needs.

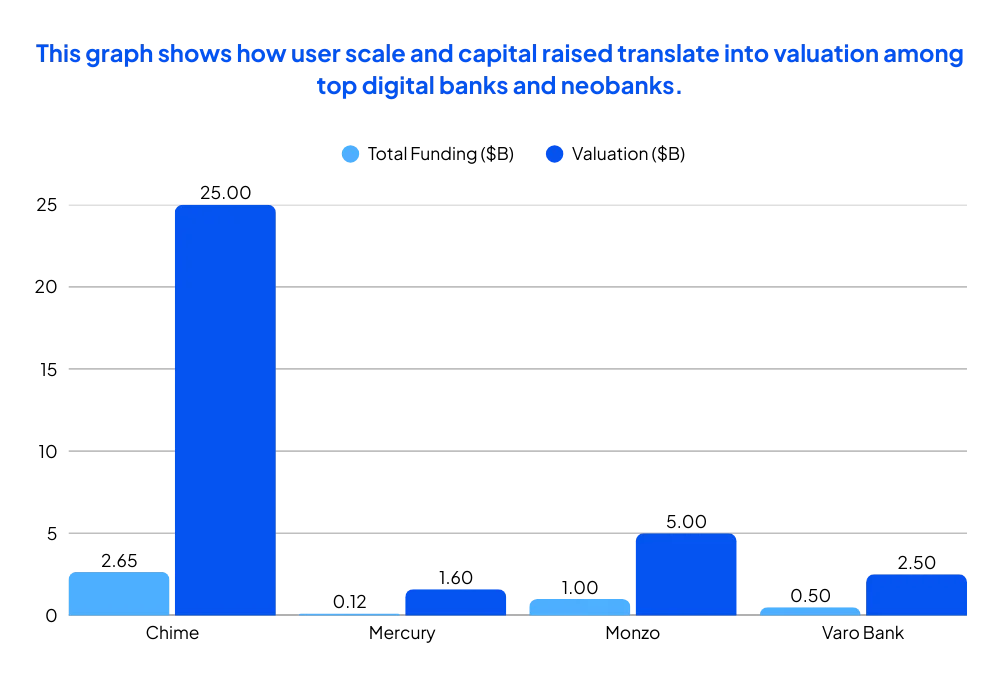

7. Chime 🏆

Services: Leading U.S. neobank offering no-fee mobile banking, early paycheck access, and automated savings features.

Founded: 2013 | HQ: San Francisco, USA | Employees: 1,500+ | Total Funding: $2.65B | Stage: Late Stage | Valuation: $25B (2021)

Worth Mentioning: Over 22.3 million users. Filed confidential IPO in December 2024, planned public listing in 2025.

8. Mercury

Services: Mercury is a standout example of fintech innovation from the 2015–2018 wave. It is considered one of the top neobanks for startups in 2026, offering banking, treasury, and credit tools built for founders.

Founded: 2017 | HQ: San Francisco, USA | Employees: 200+ | Total Funding: $120M+ | Stage: Series B | Valuation: $1.6B+

Worth Mentioning: Serves 100,000+ startups with $500M annualized revenue. In talks with Sequoia for new funding. Expanded to Mercury Personal in 2024.

9. Monzo

Services: UK-based digital bank offering current accounts, savings, lending, and budgeting tools via mobile app.

Founded: 2015 | HQ: London, UK | Employees: 2,000+ | Total Funding: $1B+ | Stage: Series H | Valuation: $5B+

Worth Mentioning: Reported revenue over $1B and pre-tax profit for year ending March 2025 (per Financial Times). Over 9 million customers.

10. Varo Bank

Services: First nationally chartered neobank in the U.S., offering FDIC-insured accounts, high-yield savings, and credit-building products.

Founded: 2015 | HQ: San Francisco, USA | Employees: 500+ | Total Funding: $500M+ | Stage: Series D | Valuation: $2.5B+

Worth Mentioning: First de novo national bank charter granted since 2008.

Notice a trend among successful neobanks? They all follow a similar evolution:

- Phase 1 (Years 1-3): Free checking accounts to acquire users at scale (Chime: 22.3M users)

- Phase 2 (Years 3-5): Cross-sell higher-margin products (credit builder, savings accounts, overdraft protection)

- Phase 3 (Years 5+): Launch lending products (personal loans, credit cards) for profitability

The numbers tell the story: Chime filed confidentially for IPO after reaching profitability. Monzo reported over $1 billion in revenue and pre-tax profit for the year ending March 2025. Mercury hit $500M in annualized revenue serving 100,000+ startups.

🎯 Key Insight: Interchange fees (from debit card swipes) + interest income (from deposits) + subscription revenue (premium features) = sustainable neobank business model.

💡 Tip: Rapid scaling means expanding teams fast, a stage where many startups struggle. An HR checklist for startups helps structure hiring, onboarding, and compliance as headcount grows.

Lending & Credit Platforms: How Are FinTech Lending and Credit Platforms Changing Access to Capital?

Lending and credit startups use technology to simplify borrowing and expand access to capital. These platforms offer faster approvals, alternative credit models, and flexible financing for individuals and businesses by securing strong distribution channels early in the market.

11. SoFi (Social Finance)

Services: Multi-product financial services platform offering student loan refinancing, personal loans, mortgages, investing, and banking.

Founded: 2011 | HQ: San Francisco, USA | Employees: 4,000+ | Total Funding: Public (NASDAQ: SOFI) | Stage: Public Company | Valuation: $8B+ market cap

Worth Mentioning: Over 7 million members.

12. MoneyLion

Services: All-in-one financial platform providing personal loans, credit monitoring, cash advances, and investment accounts for consumers.

Founded: 2013 | HQ: New York City, USA | Employees: 500+ | Total Funding: Public (NYSE: ML) | Stage: Public Company | Valuation: $1B+ market cap

Worth Mentioning: Serves over 14 million customers.

13. OnDeck

Services: Online small business lending platform offering term loans and lines of credit with fast approval processes.

Founded: 2007 | HQ: New York City, USA | Employees: 500+ (part of Enova) | Total Funding: Acquired by Enova | Stage: Acquired | Valuation: $90M acquisition (2020)

Worth Mentioning: Pioneered online small business lending. Has originated over $13 billion in loans.

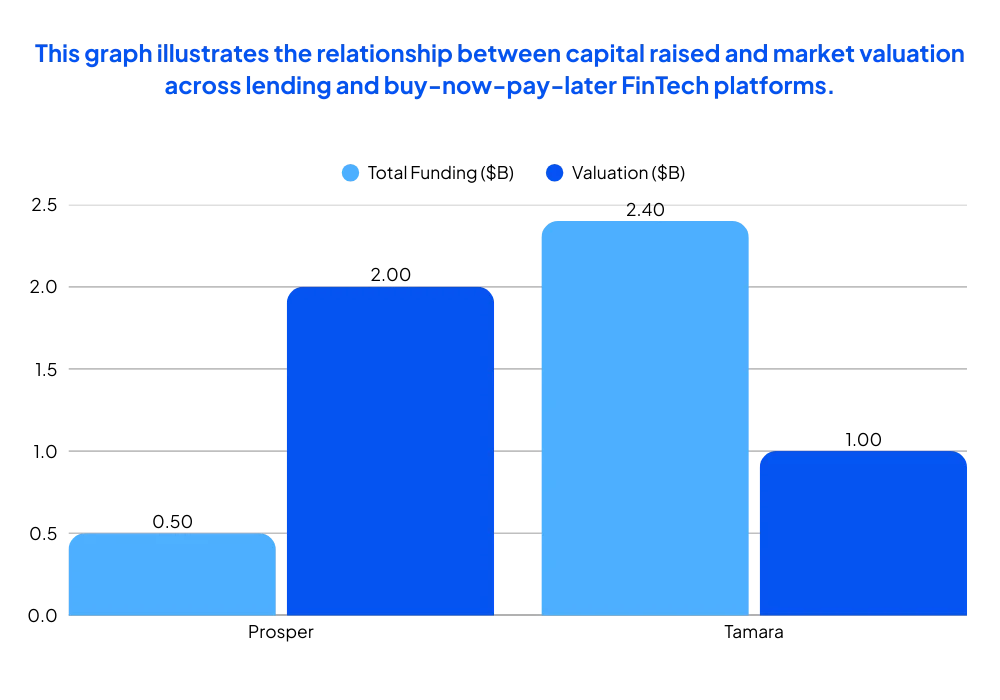

14. Prosper

Services: Peer-to-peer lending marketplace connecting borrowers with investors for personal loans.

Founded: 2005 | HQ: San Francisco, USA | Employees: 300+ | Total Funding: $500M+ | Stage: Late Stage | Valuation: $2B+

Worth Mentioning: First P2P lending marketplace in the U.S., with over $20 billion funded.

15. Tamara

Services: MENA-focused Buy Now, Pay Later platform enabling shoppers to split purchases into interest-free installments.

Founded: 2020 | HQ: Riyadh, Saudi Arabia | Employees: 400+ | Total Funding: Up to $2.4B financing package (2025) | Stage: Series C | Valuation: $1B+

Worth Mentioning: Rapidly growing BNPL leader in Saudi Arabia and UAE.

- SoFi evaluates education, career trajectory, and cash flow—not just credit scores

- MoneyLion uses bank account data (via Plaid) to assess real-time financial health

- Prosper’s peer-to-peer model allows individual investors to make lending decisions

- AI-powered models reduce default rates by 20-40% compared to traditional underwriting

Traditional banks rely on FICO scores created in 1989—using credit history, payment patterns, and debt ratios. But what about the 45 million Americans with “thin” credit files or immigrants like those served by Pomelo?

Modern fintech lenders are rewriting underwriting:

Real-world impact: Pomelo provides credit cards to Latin American immigrants who’ve been excluded from traditional banking—enabling them to build U.S. credit history while supporting families back home through integrated remittances.

💳 By 2027, analysts predict AI-based underwriting will approve 30% more borrowers than traditional methods while maintaining lower default rates.

Investing & Wealth Tech: Which Investing and WealthTech Startups Are Redefining Personal Finance?

Investing and Wealth Tech startups use digital tools to simplify investing and personal finance. These companies help individuals research investments, manage portfolios, and build long-term wealth more efficiently.

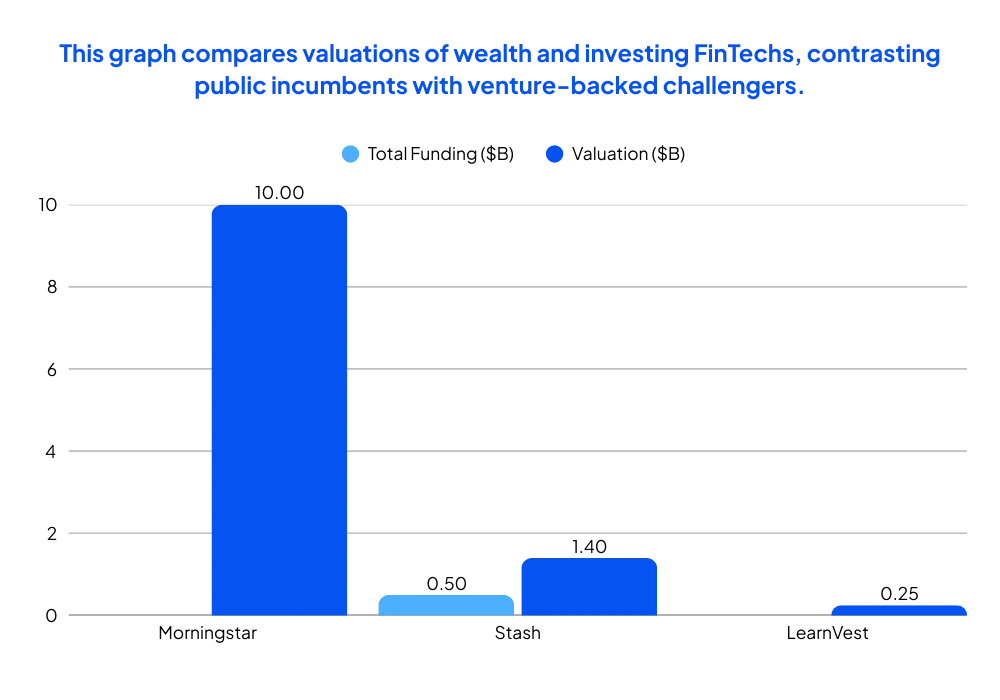

16. Morningstar

Services: Investment research and portfolio management platform providing data, analytics, and tools for investors and financial advisors.

Founded: 1984 | HQ: Chicago, USA (NYC office) | Employees: 10,000+ | Total Funding: Public (NASDAQ: MORN) | Stage: Public Company | Valuation: $10B+ market cap

Worth Mentioning: Covers 600,000+ investment offerings globally.

17. Stash

Services: Beginner-friendly investing and personal finance app offering fractional shares, banking, and personalized guidance.

Founded: 2015 | HQ: New York City, USA | Employees: 300+ | Total Funding: $500M+ | Stage: Series G | Valuation: $1.4B

Worth Mentioning: Over 6 million users.

18. LearnVest (Northwestern Mutual)

Services: Financial planning platform combining technology with certified financial planners to help users budget, save, and invest.

Founded: 2009 | HQ: New York City, USA | Employees: Part of Northwestern Mutual | Total Funding: Acquired by Northwestern Mutual | Stage: Acquired | Valuation: $250M acquisition (2015)

Worth Mentioning: Pioneer in digital financial planning.

19. Copilot (Personal Finance)

Services: Premium personal finance management app for iOS, offering budgeting, spending tracking, and financial insights.

Founded: 2020 | HQ: San Francisco, USA | Employees: 50+ | Total Funding: Bootstrapped/Angel | Stage: Early Stage | Valuation: Undisclosed

Worth Mentioning: Subscription-based model with strong user engagement.

- Morningstar made investment research accessible to financial advisors at a fraction of Bloomberg’s cost

- Stash enabled fractional share investing—buy $5 of Apple stock, not a full $180 share

- Market Terminal (Product Hunt trending, Jan 2026) promises “A Wall Street Terminal For Everyone”

- Copilot and other PFM apps give retail investors institutional-grade portfolio analytics on their phones

For decades, professional financial data was locked behind Bloomberg Terminals costing $24,000/year. Hedge funds and investment banks had information asymmetry over retail investors. Then came the wealth tech revolution:

Case Study: Stash’s 6 million users have invested over $3 billion collectively—many of them first-time investors under age 30 who would never have opened a traditional brokerage account.

📱 The average Stash user invests $50/month. Traditional wealth managers require $100,000+ minimums. That’s democratization.

B2B Financial Infrastructure (APIs, Treasury, Cards): What Are the Leading B2B FinTech Infrastructure Startups Powering Modern Finance?

B2B financial infrastructure startups build the underlying APIs and platforms that power modern financial services, and many of the most promising ventures participate in programs such as the Mastercard fintech startups program, which provides tailored mentorship, co-innovation opportunities, and access to a global payments ecosystem.

These companies enable payments, banking, treasury, and embedded finance for other businesses. Many infrastructure-focused FinTechs function similarly to SaaS Startups, selling subscription-based access to payments, banking, and compliance APIs.

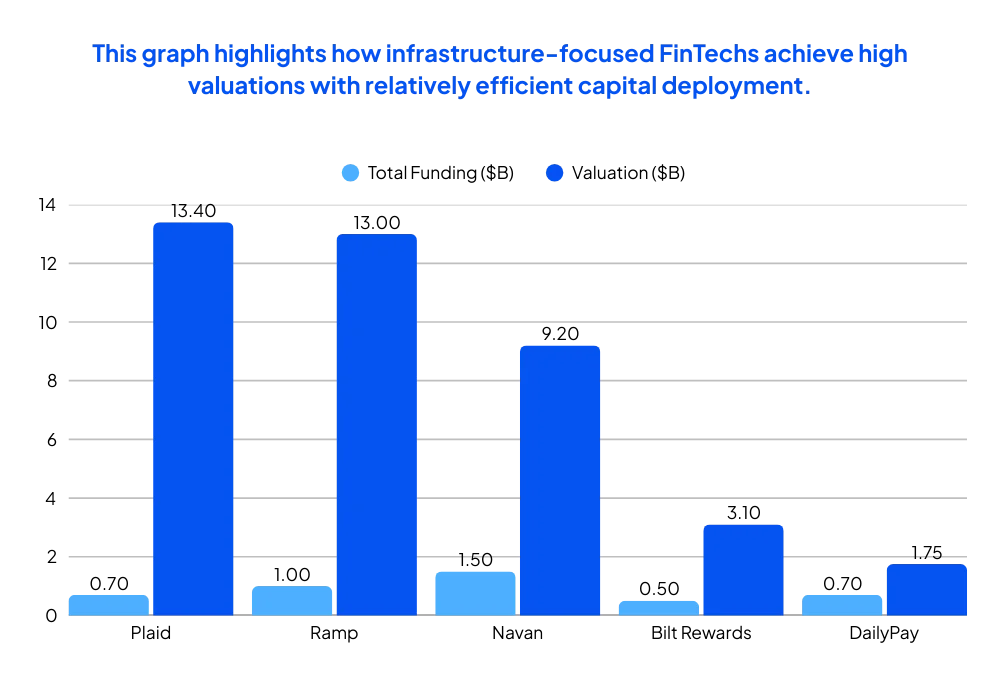

20. Plaid 🏆

Services: Open banking API platform enabling applications to connect with users’ bank accounts for payments, identity verification, and financial data access.

Founded: 2013 | HQ: San Francisco, USA | Employees: 1,000+ | Total Funding: $700M+ | Stage: Series D | Valuation: $13.4B (2021)

Worth Mentioning: Connects 8,000+ digital finance apps with 12,000 financial institutions. 2024 revenue up over 25%. Exploring secondary sale with Goldman Sachs. Backed by Andreessen Horowitz, Kleiner Perkins, and Sequoia (via Index Ventures).

21. Ramp 🏆

Services: Corporate card and spend management platform helping businesses control expenses, automate finance workflows, and save money.

Founded: 2019 | HQ: New York City, USA | Employees: 600+ | Total Funding: $1B+ | Stage: Series D | Valuation: $13B (2025)

Worth Mentioning: Serves 30,000+ businesses with $55B annualized payment volume. Saved customers 20 million hours. Backed by Sequoia Capital, Thrive Capital, and Founders Fund. AI expansion planned for 2025.

22. Navan (formerly TripActions) 🏆

Services: Navan (formerly TripActions) — considered among the leading fintech startups in NYC area — is an all-in-one travel, corporate card, and expense management platform for businesses of all sizes.

Founded: 2015 | HQ: Palo Alto, USA (NYC presence) | Employees: 1,800+ | Total Funding: Over $1.5B | Stage: Series G | Valuation: $9.2B

Worth Mentioning: FinTech revenue growth ~40%, travel bookings up nearly 2x YoY. Backed by Andreessen Horowitz, Coatue, Goldman Sachs, and Lightspeed. On track for 2026 IPO per CNBC.

23. Moov (YC S19)

Services: Payment API infrastructure enabling businesses to accept, store, and send money with built-in compliance and fraud prevention.

Founded: 2018 | HQ: Remote (U.S.-based) | Employees: 51-100 | Total Funding: $45M (Series B, 2023)> | Stage: Series B | Valuation: Undisclosed

Worth Mentioning: Y Combinator S19 and Andreessen Horowitz-backed. Developer-first payment infrastructure.

24. Bilt Rewards

Services: Loyalty and payments platform allowing renters to earn points on rent payments without transaction fees, redeemable for travel, fitness, and dining.

Founded: 2019 | HQ: New York City, USA | Employees: 200+ | Total Funding: $500M+ | Stage: Series C | Valuation: $3.1B (2023)

Worth Mentioning: $30B annual platform spending across 4 million rental units. Partners with 21,000 restaurants and 3,500 fitness studios. 70% of top U.S. property owners/managers use Bilt.

25. DailyPay

Services: Earned wage access platform enabling employees to access their earned wages before payday, used by major employers like Target, Kroger, and Hilton.

Founded: 2015 | HQ: New York City, USA | Employees: 500+ | Total Funding: $700M+ | Stage: Series D+ | Valuation: ~$1.75B

Worth Mentioning: Featured on Deloitte Tech Fast 500. 2025 IPO expected. Nelson Chai named executive chair in January 2025.

- Proximity to enterprise buyers: Fortune 500 CFOs, banks, and asset managers are headquartered in NYC/NJ

- Financial services talent: Thousands of ex-Goldman, JPMorgan, and hedge fund professionals transition to fintech

- Regulatory access: CFTC, SEC, FINRA, and NY Department of Financial Services are blocks away

- B2B sales culture: Selling to enterprises requires in-person relationship building—NYC’s density enables it

Notice how Ramp, Plaid, Navan, DailyPay, Trumid, Kalshi, Bilt Rewards, and Venmo — frequently cited among nyc’s most innovative fintech startups — all have headquarters or major offices in New York City? It’s not a coincidence.

NYC’s FinTech Advantage:

The data backs it up: Ramp grew from 0 to $55B in annualized payment volume in 5 years by being steps away from its target customers. Trumid onboarded 920+ institutional bond traders because NYC is the fixed-income capital of the world.

🗽 Fun Fact: According to Built In NYC, the city is home to 6 of the top 10 fastest-growing B2B fintech companies in the U.S.

Crypto & Digital Assets FinTechs: Which Crypto and Digital Asset FinTech Startups Are Gaining Real-World Adoption?

Crypto and digital asset FinTech startups develop platforms for blockchain-based payments, custody, and asset management. These companies support secure digital transactions and real-world adoption of cryptocurrencies.

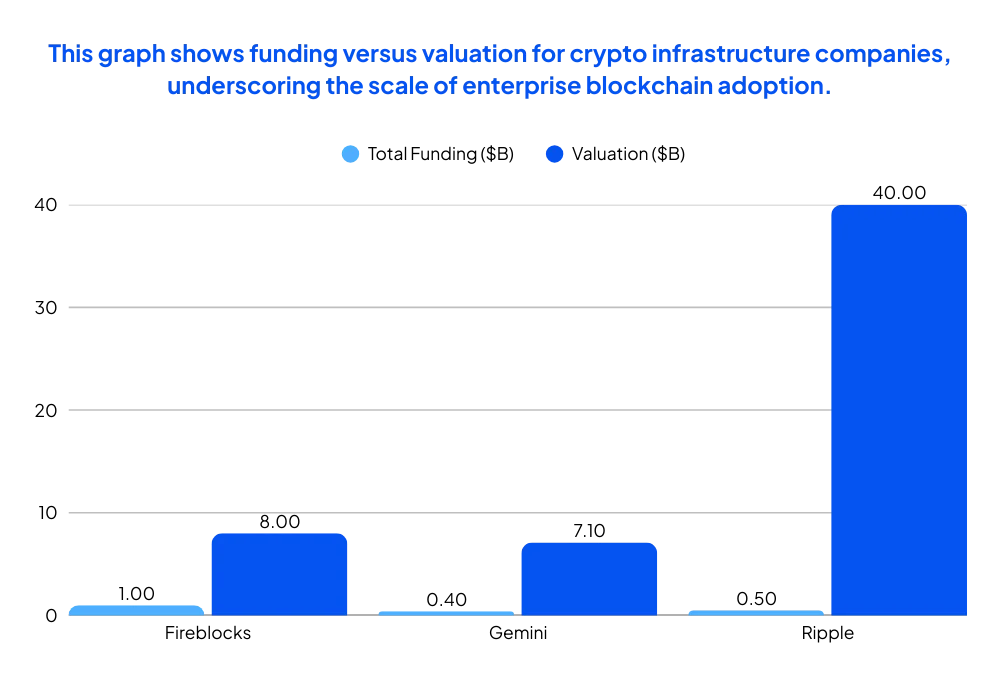

26. Fireblocks 🏆

Services: Enterprise-grade platform for storing, transferring, and issuing digital assets with institutional security and compliance.

Founded: 2018 | HQ: New York City, USA | Employees: 500+ | Total Funding: $1B+ | Stage: Series E | Valuation: $8B

Worth Mentioning: Serves 2,000+ organizations securing $7 trillion in digital asset transactions across 100 blockchains and 250 million wallets. Backed by Sequoia Capital and Spark Capital. Expanded with Japan office.

27. Gemini

Services: Regulated cryptocurrency exchange and custodian offering trading, custody, and crypto credit products for retail and institutional clients.

Founded: 2014 | HQ: New York City, USA | Employees: 1,000+ | Total Funding: $400M+ | Stage: Series D | Valuation: $7.1B (2021)

Worth Mentioning: Founded by Winklevoss twins. Licensed in multiple jurisdictions.

28. Ripple

Services: Blockchain-based payment protocol and cryptocurrency (XRP) enabling fast, low-cost international money transfers for financial institutions.

Founded: 2012 | HQ: San Francisco, USA | Employees: 700+ | Total Funding: $500M latest round | Stage: Late Stage | Valuation: $40B (per Reuters)

Worth Mentioning: Partnerships with over 300 financial institutions globally.

29. Pomelo (YC W20)

Services: Neobank and credit card platform designed for Latin American immigrants in the U.S., enabling remittances and credit building.

Founded: 2020 | HQ: San Francisco Bay Area, USA | Employees: 11-50 | Total Funding: $40M (Series B, 2024) | Stage: Series B | Valuation: Undisclosed

Worth Mentioning: VC-backed fintech startup founded in 2020, supported by Y Combinator and Founders Fund.

- Fireblocks secures $7 trillion in digital asset transactions across 100 blockchains for 2,000+ institutions

- Gemini was founded by the Winklevoss twins specifically to be the “most regulated” crypto exchange—holding licenses in 50+ jurisdictions

- Ripple spent years in legal battles with the SEC, highlighting why a legal checklist is critical for establishing regulatory clarity for assets like XRP early on.

Consumer crypto exchanges like Coinbase focus on ease of use. But institutional platforms—Fireblocks, Gemini, Ripple—live or die by security and compliance. The stakes are astronomical:

Case Study: Fireblocks’ Multi-Party Computation (MPC): Instead of storing private keys in one location (vulnerable to hacks), Fireblocks splits keys into multiple encrypted shares distributed across different secure environments. This technology has secured over $7 trillion in transactions with zero security breaches, a remarkable feat in an industry plagued by hacks totaling billions.

Why it matters: When JP Morgan, BNY Mellon, or Fidelity custody client crypto assets, a single security failure could trigger billions in losses and regulatory shutdown. That’s why institutional crypto infrastructure commands Fireblocks’ $8B valuation despite being younger than most consumer crypto apps.

⚡ In 2024-2025, major banks and asset managers finally entered crypto custody, validating Fireblocks’ and Gemini’s regulatory-first approach.

RegTech and Compliance Solutions: How Are RegTech and Compliance Startups Helping Financial Firms Stay Compliant?

RegTech and compliance startups help financial firms meet regulatory requirements through technology. These companies automate compliance, risk management, and reporting in highly regulated financial markets.

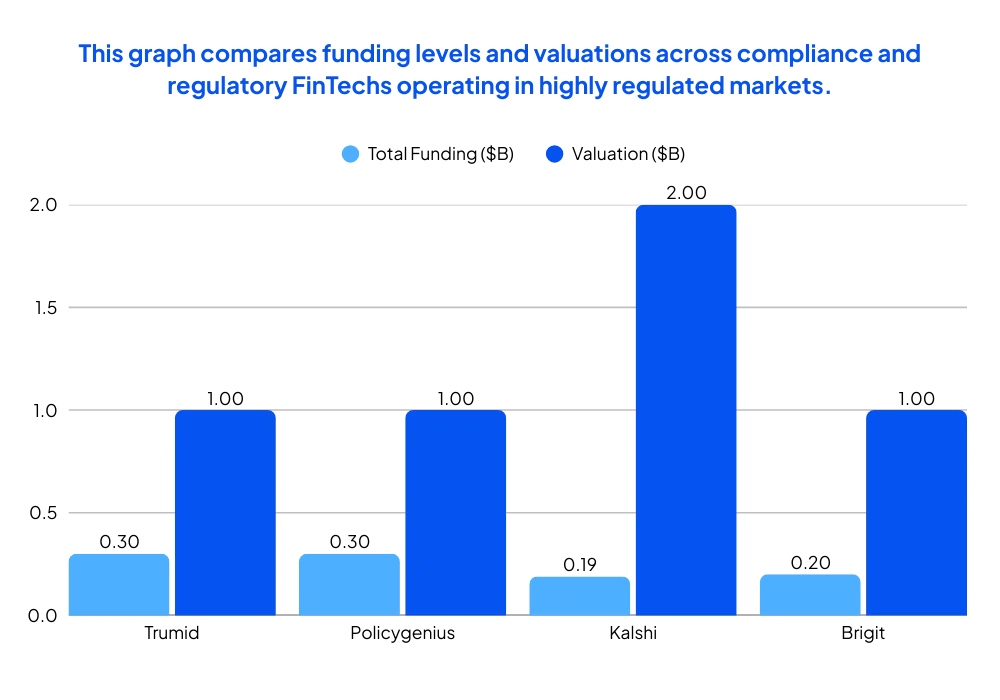

30. Trumid

Services: Electronic trading platform for corporate bonds, offering price discovery, liquidity, and execution for institutional investors.

Founded: 2014 | HQ: New York City, USA | Employees: 200+ | Total Funding: $300M+ | Stage: Series D | Valuation: $1B+

Worth Mentioning: 2024 trading volume +62% YoY to $1.4T. 16,000+ bonds traded, 920+ institutions onboarded.

31. Policygenius

Services: Online insurance marketplace and comparison platform for life, home, auto, disability, and pet insurance.

Founded: 2014 | HQ: New York City, USA | Employees: 400+ | Total Funding: $300M+ | Stage: Series E | Valuation: $1B+ (unicorn)

Worth Mentioning: Over $100 billion in coverage placed.

🔗 Links: Website

32. Kalshi (YC W19)

Services: CFTC-regulated event contracts exchange enabling users to trade on outcomes of real-world events (elections, economic data, weather).

Founded: 2019 | HQ: New York City, USA | Employees: 101-200 | Total Funding: $185M (Series C, 2025) | Stage: Series C | Valuation: $2.0B

Worth Mentioning: Y Combinator W19 and Sequoia Capital-backed. First CFTC-regulated prediction market exchange in the U.S.

33. Camber Health (YC W21)

Services: Healthcare payments infrastructure platform enabling providers to manage eligibility, claims, and payments in emerging markets.

Founded: 2021 | HQ: New York City, USA | Employees: 51-100 | Total Funding: $30M (Series B, 2025) | Stage: Series B | Valuation: Undisclosed

Worth Mentioning: Y Combinator W21 and Andreessen Horowitz-backed.

🔗 Links: Website

34. Bloomberg

Services: Financial data, news, analytics, and trading platform serving institutional investors, traders, and financial professionals worldwide.

Founded: 1981 | HQ: New York City, USA | Employees: 20,000+ | Total Funding: Private (bootstrapped) | Stage: Mature Private | Valuation: $100B+

Worth Mentioning: Industry-standard Bloomberg Terminal. Over 325,000 terminal subscribers.

🔗 Links: Website

35. Dave

Services: Neobank offering cash advances, budgeting tools, and no-fee banking to help users avoid overdrafts and manage money better.

Founded: 2016 | HQ: Los Angeles, USA | Employees: 500+ | Total Funding: Public (NASDAQ: DAVE) | Stage: Public Company | Valuation: $500M+ market cap

Worth Mentioning: Over 10 million users.

36. Brigit

Services: Financial health app providing cash advances, budgeting, credit building, and identity theft protection for consumers.

Founded: 2017 | HQ: New York City, USA | Employees: 200+ | Total Funding: $200M+ | Stage: Series D | Valuation: $1B+

Worth Mentioning: Acquired in 2024 (noted in Plaid article).

37. Shopify Balance (Embedded Finance)

Services: Banking and financial tools embedded within Shopify’s commerce platform, offering business accounts, cards, and capital to merchants.

Founded: 2020 (Balance launch) | HQ: Ottawa, Canada (Shopify HQ) | Employees: Part of Shopify (10,000+) | Total Funding: Part of Shopify (public) | Stage: Public Parent | Valuation: Part of Shopify

Worth Mentioning: Powered by Unit and Checkout.com.

38. SoLo Funds

Services: Community finance platform connecting borrowers with individual lenders for small, short-term loans outside traditional banking.

Founded: 2018 | HQ: Los Angeles, USA | Employees: 100+ | Total Funding: $50M+ | Stage: Series B | Valuation: Undisclosed

Worth Mentioning: Peer-to-peer lending alternative to payday loans.

- Tabby (UAE): $4.5B valuation—larger than many U.S. fintech unicorns

- Tamara (Saudi Arabia): Secured up to $2.4B in financing in 2025

- 400%+ growth: MENA fintech funding has quadrupled since 2019

While Silicon Valley focuses on U.S. markets, the smartest FinTech investors are pouring capital into the Middle East and North Africa (MENA):

Why MENA is exploding: 65% of the population is under 30, smartphone penetration exceeds 80%, governments (Saudi Vision 2030, UAE Digital Economy Strategy) actively support fintech, and 70%+ of adults remain underbanked, creating massive TAM for digital financial services.

The BNPL battle: Tabby and Tamara are fighting for dominance in a region where credit card penetration is low but e-commerce is booming. Winner could become the Middle East’s first $10B+ fintech.

🕌 Cultural insight: Islamic finance principles (no interest-bearing loans) make BNPL’s “split payments” model particularly attractive in MENA markets.

Top FinTech Startups by Funding and Investor Backing

The strongest indicator of a FinTech startup’s potential, and what often separates the top fintech companies from the rest, is the caliber of its investors and the capital it has raised.

Y Combinator-Backed FinTech Startups

- Wave (YC W17) – B2B payments and invoicing for small businesses

- Moov (YC S19) – Payment API infrastructure; raised $45M Series B with Andreessen Horowitz in 2023

- Kalshi (YC W19) – CFTC-regulated event contracts exchange; $2.0B valuation, $185M Series C with Sequoia in 2025

- Camber Health (YC W21) – Healthcare payments infrastructure in emerging markets; $30M Series B with a16z in 2025

- Pomelo (YC W20) – Neobank for Latin American immigrants; $40M Series B with Founders Fund in 2024

Why it matters: YC’s network has helped FinTech founders turn startup ideas into validated businesses with scaled go-to-market strategies, particularly in B2B infrastructure and emerging market segments.

Thinking of joining that network? This startup checklist helps you move from idea to early traction.

VC Leaders in FinTech: Sequoia, Andreessen Horowitz, and More

🏅 Sequoia Capital Portfolio

- Stripe – $91.5B valuation; processed $1.4T in 2024

- Plaid – $13.4B valuation; connects 8,000+ apps with 12,000 financial institutions

- Fireblocks – $8B valuation; $7T in digital asset transactions secured

- Ramp – $13B valuation; $55B annualized payment volume across 30,000+ businesses

- Kalshi – $2.0B valuation; first CFTC-regulated prediction market in the U.S.

- Mercury – In financing talks with Sequoia; serves 100,000+ startups

Sequoia’s FinTech Thesis: According to Sequoia Capital, they invest across the entire FinTech stack—from infrastructure (APIs, data, compliance) to vertical applications (lending, wealth, insurance). The firm has 171 Financial Technology startups in its 2026 portfolio. Sequoia launched $950M in new seed and venture funds in 2025 to continue backing FinTech innovation.

🏅 Andreessen Horowitz (a16z) Portfolio

- Stripe – Co-investor alongside Sequoia

- Plaid – Early investor in open banking infrastructure

- Navan – $9.2B valuation; travel and corporate card platform

- Moov – Payment API infrastructure; $45M Series B

- Camber Health – Healthcare payments in emerging markets; $30M Series B

a16z’s FinTech Strategy: The firm’s FinTech team invests across banking, lending, insurance, and real estate. In 2026, a16z raised over $15 billion in new venture funds to invest across AI, crypto, biotech, health, infrastructure, and growth—with FinTech remaining a core focus area.

🏅 Other Leading VC Firms in FinTech

- Founders Fund: Ramp ($13B valuation), Pomelo ($40M Series B)

- Thrive Capital: Ramp, Plaid

- Kleiner Perkins: Plaid

- Spark Capital: Plaid, Fireblocks

- Lightspeed Venture Partners: Navan

- Goldman Sachs: Navan, Plaid (exploring secondary sale)

Unicorn & High-Valuation FinTech Startups

- Stripe – $91.5B (payments infrastructure)

- Chime – $25B (consumer neobank; IPO expected 2025)

- Plaid – $13.4B (open banking API)

- Ramp – $13B (corporate card & spend management)

- Navan – $9.2B (travel & expense management)

- Fireblocks – $8B (digital asset infrastructure)

- Airwallex – $6.2B (cross-border payments)

- Monzo – $5B+ (UK neobank)

- Tabby – $4.5B (MENA buy-now-pay-later)

- Bilt Rewards – $3.1B (rent rewards & payments)

- Varo Bank – $2.5B+ (U.S. chartered neobank)

- Kalshi – $2.0B (prediction market exchange)

- DailyPay – ~$1.75B (earned wage access; 2025 IPO expected)

3 New FinTech Startups Trending on Product Hunt

Product Hunt is a leading platform for discovering new tech products, and these three Financial Technology startups captured the community’s attention in late 2025 and early 2026:

1. xPayCross-border

Category: Payments & Money Transfer

What it does: Enterprise-focused cross-border payment platform simplifying international transactions with competitive FX rates and transparent fees.

Product Hunt Performance: 332 Followers (Top FinTech product of January 2026)

Why it’s trending: As global commerce continues to grow, businesses need reliable, cost-effective international payment rails. xPayCross-border addresses pain points in B2B cross-border transactions.

2. Market Terminal

Category: Investing & Wealth Tech

What it does: “A Wall Street Terminal For Everyone” – democratizing access to professional-grade financial data, analytics, and trading tools previously available only to institutions.

Product Hunt Performance: 287 Followers (January 2026 top 10)

Why it’s trending: Retail investors increasingly demand institutional-quality tools at affordable prices. Market Terminal capitalizes on the trend of democratizing financial data (similar to Bloomberg Terminal disruption).

3. Optivault

Category: Personal Finance & AI

What it does: AI-powered financial advisor providing personalized investment recommendations, portfolio optimization, and financial planning insights.

Product Hunt Performance: 130 Followers (December 2025 top FinTech)

Why it’s trending: AI-driven financial advice is exploding as consumers seek low-cost alternatives to human advisors. Optivault leverages machine learning to offer personalized guidance at scale.

Honorable Mentions: Other notable Product Hunt FinTech entries include Cumbuca (Brazil payments infrastructure, 403 followers), Autonomous (0% fee financial advisor, 127 followers), and Payroll by Card App (credit card-funded payroll, 183 followers).

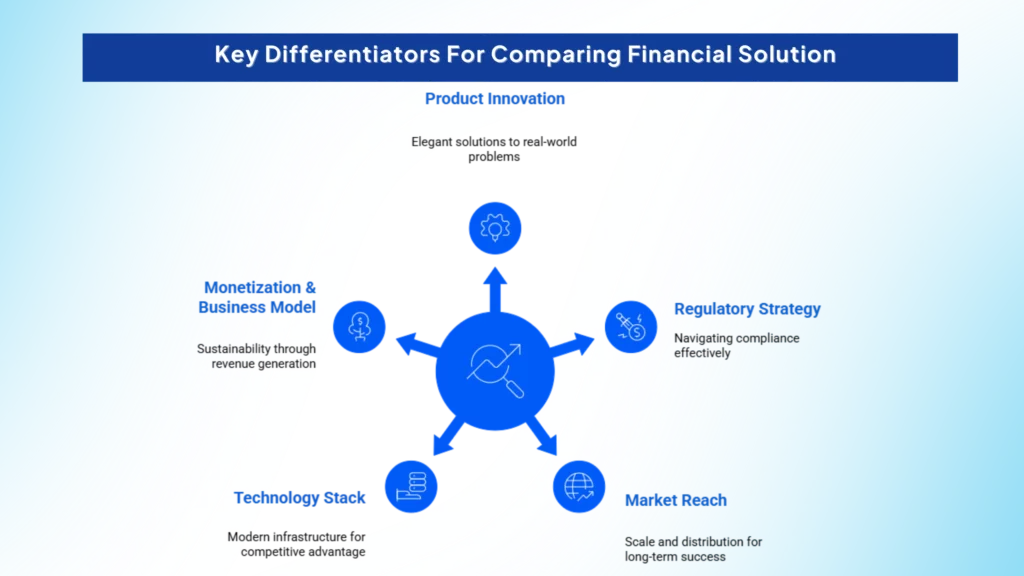

Comparing FinTech Solutions: Key Differentiation Factors

With 38 FinTech startups across multiple categories, how do you evaluate which solutions are truly innovative now also means knowing how AI presents them—making it essential to audit brand visibility on LLMs alongside traditional launch and readiness checks.

Here are the five critical dimensions for comparing the largest FinTech companies:

1. Product Innovation

The best FinTechs solve real problems with elegant technology:

- Stripe pioneered developer-friendly payment APIs, making it trivial to accept payments online

- Plaid unlocked financial data portability with its open banking infrastructure

- Ramp automated expense management with AI-powered workflows, saving customers 20 million hours

- Kalshi created the first regulated prediction market exchange in the U.S., enabling hedging on real-world events

2. Regulatory Strategy

Navigating compliance is a key differentiator:

- Varo Bank became the first neobank to obtain a national bank charter, enabling FDIC insurance without partner banks

- Gemini and Fireblocks prioritize regulatory compliance in crypto, earning trust from institutions

- Kalshi obtained CFTC approval for event contracts, setting a precedent for prediction markets

- Chime operates through partner banks (Bancorp, Stride), balancing innovation with compliance

3. Market Reach

Scale and distribution determine long-term winners:

- Stripe processes $1.4T annually across 120+ countries

- Chime serves 22.3 million U.S. consumers, the largest neobank by users

- Plaid connects 8,000+ apps with 12,000 financial institutions

- Tabby and Tamara dominate MENA’s fast-growing BNPL market

Traffic alone is no longer enough, a reality explored in why my Startup’s leads dropped even though SEO didn’t.

4. Technology Stack

Modern infrastructure separates leaders from laggards:

- API-first: Stripe, Plaid, Moov enable developers to integrate financial services via RESTful APIs

- AI/ML: Ramp uses machine learning for expense categorization; Optivault and Autonomous offer AI financial advisors

- Blockchain: Fireblocks, Ripple, and Gemini leverage distributed ledger technology for security and speed

- Cloud-native: Most modern FinTechs run on AWS, Google Cloud, or Azure for scalability

5. Monetization & Business Model

How FinTechs make money reveals sustainability:

- Transaction fees: Stripe, Airwallex charge percentage of payment volume

- Subscription/SaaS: Ramp, Navan, Mercury offer platform subscriptions

- Interchange revenue: Chime, Varo earn from debit card usage

- Interest income: SoFi, MoneyLion profit from lending

- Data licensing: Plaid monetizes aggregated financial data insights

- Float/treasury services: Mercury offers yield on business deposits

Which FinTech Startups Should I Watch for Tokenized Assets?

The leading FinTech startups in asset tokenization are Ondo Finance (largest provider with ~$2B in tokenized Treasuries), Securitize (841% revenue surge in 2025), tZERO (tokenization-as-a-service infrastructure), Figure Technology Solutions (Provenance Blockchain for home equity), and Centrifuge (real-world asset DeFi protocol), with the tokenized securities market projected to reach $400 billion in 2026 according to Forbes analysis.

Top 6 Tokenized Asset FinTech Startups:

- Ondo Finance – Tokenized Treasuries & Equities Leader

Ondo Finance became the largest provider of both tokenized Treasuries and tokenized stocks in January 2026, with approximately $2 billion in total value locked (TVL). The company announced plans to launch tokenized U.S. stocks and ETFs on the Solana blockchain in early 2026.

Notably, the SEC formally closed its multi-year investigation into Ondo in 2026 without filing charges, signaling regulatory acceptance. Ark Invest projects the tokenized assets market could surpass $11 trillion by 2030, positioning Ondo as a category leader. - Securitize – Institutional Tokenization Platform

Securitize reported an 841% revenue surge in 2025 as institutional demand for tokenized securities accelerated. The platform holds licenses required for compliant tokenized securities issuance and serves asset managers tokenizing private equity, real estate, and fixed-income products. According to industry analysis, Securitize ranks as the #2 asset tokenization platform globally. - tZERO – Tokenization-in-a-Box Infrastructure

tZERO operates as a blockchain-powered multi-asset infrastructure provider offering “tokenization-as-a-service.” In January 2026, tZERO announced it would leverage its SPBD (special purpose broker-dealer) license to expand into crypto assets, creating unified tokenized markets.

The company’s regulatory-first approach makes it attractive for traditional financial institutions entering digital assets. - Figure Technology Solutions – Blockchain Lending & Provenance Network

Figure operates the Provenance Blockchain, supporting tokenization of home equity lines of credit (HELOCs), cash-out refinance loans, and other financial products.

By 2025, Figure had developed comprehensive systems for trading and managing blockchain-based assets. The company represents the intersection of traditional lending and tokenized asset infrastructure. - Centrifuge – Real-World Asset DeFi Protocol

Centrifuge connects real-world assets to decentralized finance, enabling businesses to tokenize invoices, real estate, and other cash-flow-generating assets. The protocol ranked #6 in Medium’s Top Asset Tokenization Platforms analysis for 2025-2026. - Polymath & Tokeny – Security Token Standards

Polymath (security token issuance platform) and Tokeny (compliance-focused tokenization) provide infrastructure for regulated security tokens. Both platforms emphasize built-in compliance automation, making them attractive to asset managers navigating SEC and MiCA regulations.

Market Context: The BDO 2026 FinTech Industry Predictions report notes that traditional banks introduced tokenization in 2025, and FinTechs will increasingly prioritize institutional endorsements in 2026. With speculation that tokenized securities could achieve $400 billion market cap in 2026 (Forbes), early-stage investors should focus on platforms with regulatory clarity (SEC closed investigations, banking licenses) and institutional partnerships.

Which FinTech Startups are Focused on Helping People with Bad Credit Rebuild Their Credit Scores?

Fintech startups focused on helping people with bad credit rebuild their credit scores include StellarFi, Self (formerly Self Lender), and Kikoff—companies targeting the 32 million Americans estimated to be “unscoreable” due to being credit invisible or having thin credit files, according to Federal Reserve data from October 2025.

- StellarFi takes the unique approach of reporting existing bill payments (utilities, rent, subscriptions) to Experian and Equifax as credit tradelines, with WalletHub reviewers reporting 60-point credit score increases after consistent use, though the company faced technical issues with platform upgrades between July 2024 and January 2025 that temporarily limited functionality.

- Self offers credit builder loans where borrowers make monthly payments into a locked savings account that reports to all three credit bureaus, then receive the saved funds (minus interest) after the 12-24 month term ends, essentially forcing disciplined savings while building payment history.

- Kikoff provides a $750 credit line with automatic payments from a linked bank account, ensuring on-time payment history without requiring traditional creditworthiness for approval.

While these tools demonstrate measurable credit score improvements for users who make consistent on-time payments, financial experts note they work best as supplements to addressing underlying spending habits rather than standalone solutions, since payment history alone cannot overcome high credit utilization or excessive debt loads that often accompany bad credit situations.

Credit challenges remain widespread, in the U.S., an estimated ~25 million adults had insufficient or unscored credit records as recently reported by the Consumer Financial Protection Bureau (CFPB), indicating many consumers need alternative tools to improve credit access and scoring.

Should I Choose Stripe or Another FinTech Startup for My Business Payments?

Choose Stripe if you need developer-friendly APIs, global payment methods (100+), and advanced fraud prevention for online/SaaS businesses; choose Square for in-person + online integration with free hardware; choose PayPal for maximum customer trust and existing user base; choose Adyen for enterprise-scale international operations; or choose Braintree for mobile app and marketplace payment flows.

The optimal choice depends on transaction volume, in-person vs. online mix, geographic reach requirements, and technical resources available.

Detailed Payment Processor Comparison:

| Processor | Pricing | Best For | Key Differentiator | Annual Volume Processed |

|---|---|---|---|---|

| Stripe | 2.9% + $0.30 (online) 2.7% + $0.05 (in-person) |

SaaS, e-commerce, developers, global businesses | Developer-first APIs, 100+ payment methods, subscription billing, fraud prevention (Stripe Radar) | $1.4T (2024) — ~1.3% of global GDP |

| Square | 2.6% + $0.15 (in-person) 3.3% + $0.30 (online) |

Retail, restaurants, small businesses with in-person sales | Free card reader, integrated POS system, inventory management | $200B+ (2024 estimate) |

| PayPal | 2.29% + $0.09 (in-person) 3.49% + $0.09 (manual entry) |

E-commerce with existing PayPal user base, invoicing | Customer trust (active in 200+ markets), Venmo integration, buyer protection | $1.5T+ (2024 estimate) |

| Adyen | Custom pricing (volume-based) | Enterprise, high-volume businesses, international operations | 250+ payment methods, 150+ currencies, unified commerce platform, real-time fraud detection | $900B+ (2024 estimate) |

| Braintree | Similar to PayPal standard rates | Mobile apps, marketplaces, startups needing flexibility | Full-stack APIs, PayPal/Venmo/Apple Pay/Google Pay support, owned by PayPal | $200B+ (2024 estimate) |

When to Choose Stripe:

Stripe dominates the developer-first payment infrastructure market, processing $1.4 trillion in 2024 (+38% YoY), equivalent to approximately 1.3% of global GDP. According to the 2025 Fintech Payments AI Visibility Index, Stripe leads with a 77% AI Visibility Score, meaning it appears in 3 out of 4 AI-generated answers about payment processing.

Choose Stripe if you:

- Need rich developer APIs and extensive documentation (used by 80% of Forbes Cloud 100)

- Require subscription billing, usage-based pricing, or complex payment workflows

- Want built-in fraud prevention (Stripe Radar uses machine learning to block fraud)

- Need global reach—Stripe supports 100+ payment methods including Apple Pay, Google Pay, Alipay

- Value financial infrastructure beyond payments (Stripe Capital, Stripe Treasury, Stripe Issuing)

Stripe’s 2024 Performance: Achieved profitability in 2024, used by half of Fortune 100 companies, 78% of Forbes AI 50. Valuation reached $91.5 billion in February 2025 (per CNBC).

When to Choose Alternatives:

- Square — Best for brick-and-mortar + online hybrid businesses. Offers free card reader hardware and integrated point-of-sale systems. According to NerdWallet’s comparison, Square’s 2.6% + $0.15 in-person rate beats Stripe’s 2.7% + $0.05 for transaction volumes under $10,000/month. Ideal for coffee shops, boutiques, farmers markets.

- PayPal — Best for businesses targeting consumers with existing PayPal accounts (active in 200+ markets). The 2025 AI Visibility Index shows PayPal with 64% visibility score, second only to Stripe. Lower in-person rates (2.29% + $0.09) make it competitive for physical retail. Integration with Venmo expands reach to younger demographics.

- Adyen — Best for enterprise businesses processing $50M+ annually. Custom pricing becomes favorable at high volumes. Supports 250+ payment methods and 150+ currencies. Memberful analysis notes Adyen’s unified commerce platform handles online, mobile, and in-person payments through single integration, reducing technical complexity for omnichannel retailers.

- Braintree — Best for mobile apps and marketplaces (Uber, Airbnb use Braintree infrastructure). Full-stack solution supports PayPal, Venmo, Apple Pay, Google Pay, and all major cards through single SDK. Owned by PayPal but operates independently with developer-first approach similar to Stripe.

Expert Recommendation: For SaaS and online businesses with technical teams, Stripe remains the default choice due to API quality, ecosystem integrations (connects to 8,000+ apps via Plaid), and proven scalability ($1.4T processed). For retail/in-person priority, Square’s free hardware and 2.6% in-person rate provide better economics. For marketplaces requiring complex split payments, Braintree’s full-stack APIs excel.

Evaluate based on transaction volume projections, in-person vs. online mix, and available technical resources.

What Are the Biggest Challenges for New FinTech Startups Today?

The seven biggest challenges for new FinTech startups in 2026 are regulatory compliance, securing funding, cybersecurity threats, talent acquisition, building customer trust, scalability infrastructure, and differentiation in crowded markets.

- Regulatory Compliance — The Primary Failure Driver

According to a 2025 industry study, 73% of financial technology startups fail within their first three years due to preventable regulatory compliance issues. This includes navigating KYC (Know Your Customer), AML (Anti-Money Laundering), data privacy laws (GDPR, CCPA), and licensing requirements that vary across jurisdictions.

Real-world example: Chime faced regulatory scrutiny before its IPO filing, requiring extensive compliance infrastructure buildout. Ripple spent years in legal battles with the SEC over XRP’s classification, only achieving clarity in 2023. Qubit Capital research emphasizes that compliance cannot be treated as an afterthought—it must be embedded from MVP stage.

Cost impact: Compliance infrastructure typically consumes 10-15% of early-stage FinTech budgets. Startups must allocate resources for legal counsel, compliance officers, audit systems, and regulatory reporting tools. The 2026 FinTech Regulation Guide notes that regulatory obligations are increasing, particularly around AI governance (EU AI Act) and crypto asset regulations (MiCA in Europe). - Funding Challenges — 67% Decline from 2021 Peaks

FinTech VC funding dropped to $30 billion in 2023, down 67% from 2021 highs, per Qubit Capital’s funding analysis. However, 2025 showed recovery with global FinTech investment rising 21% to $53 billion across 5,918 deals (Innovate Finance report).

Investor scrutiny has intensified: According to QED Investors’ 2026 predictions, VCs now focus on profitability metrics, clear unit economics, regulatory compliance track records, and realistic path to exit (IPO or acquisition). The “growth at all costs” mentality of 2020-2021 has been replaced by “efficient growth” requirements.

Capital concentration trend: The Q4 2025 PitchBook-NVCA Venture Monitor shows remaining value in VC funds hit $1.02 trillion, surpassing 2021 levels due to markups. However, this capital is concentrating in proven sectors—AI accounted for 77% ($19.5B) of Q4 2025 funding, FinTech only 13% ($3.4B). - Cybersecurity Threats — Prime Target Status

FinTech startups handle sensitive financial data, making them prime targets for cyberattacks. According to FintechZoom’s security analysis, implementing robust security measures—encryption, multi-factor authentication (MFA), continuous monitoring, penetration testing—is essential but expensive.

Regulatory pressure increasing: The EU’s DORA (Digital Operational Resilience Act) took effect in 2025, requiring FinTechs to demonstrate cybersecurity resilience through stress testing and incident response plans. Failure to comply results in fines up to 2% of annual revenue. - Talent Acquisition & Retention — Competition with Big Tech

The 2026 Financial Technology USA Hiring Outlook shows fierce competition for AI engineers, data scientists, cybersecurity experts, and compliance professionals. Big Tech firms (Google, Meta, Microsoft) and established financial institutions offer higher salaries and stock options, making talent retention challenging for bootstrapped startups. - Customer Trust & Adoption — Overcoming Traditional Bank Bias

Building customer trust remains difficult. According to Visa’s FinTech challenges analysis, consumers remain skeptical about FinTech safety versus traditional banks, particularly regarding deposit insurance, fraud protection, and account recovery processes.

Trust gap data: Plaid’s consumer research shows 87% of Americans are comfortable with national banks versus 79% with FinTech companies—an 8-point trust gap that startups must overcome through transparency, regulatory compliance messaging, and clear FDIC insurance partnerships. - Scalability & Infrastructure — Technical Debt Accumulation

Insart’s tech stack analysis warns that rapid growth leads to technical debt where “quick fixes and patchwork solutions hinder long-term scalability.” Startups must invest in cloud-native architectures, API-first designs, and modernized systems to support growth without performance degradation.

Cost of delays: Replatforming after reaching scale costs 10x more than building correctly from the start. Companies like Mercury and Ramp invested heavily in infrastructure before scaling, enabling them to handle 100,000+ business customers and $55B annual payment volume respectively. - Market Differentiation — Standing Out Among 14,000 Competitors

The number of FinTech startups in the Americas grew from 5,868 in 2018 to nearly 14,000 in 2024 (Statista). In this crowded landscape, establishing clear differentiation is critical.

AI visibility as competitive advantage: The 2025 AI Visibility Index shows only 10 companies exceed 10% AI visibility, with the median at 1-2%. Startups investing in generative engine optimization (GEO) and AI citation strategies gain disproportionate visibility as 34% of U.S. adults now use ChatGPT for financial research (per UpGrowth).

Expert Insight:

The most successful FinTech startups in 2026 treat compliance as competitive advantage (not cost center), maintain 18-24 month cash runways to survive funding gaps, invest in cybersecurity infrastructure before incidents occur, build distributed remote teams to access global talent at competitive rates, focus on retention metrics (not just acquisition), and optimize for AI visibility to capture the growing segment discovering financial services through ChatGPT and Perplexity.

2026 will be “the year of enforcement”—startups must view regulatory compliance as foundational, not optional.

What is the Future of Financial Technology Startups?

Predictions for 2027 and Beyond

The FinTech landscape is evolving rapidly, here are our predictions:

2027-2030 FinTech Predictions

- AI-native financial advisors will surpass human advisors in AUM for retail investors (following Autonomous, Optivault trajectory)

- Embedded finance will become ubiquitous—every software platform will offer payments, lending, or banking (Shopify Balance model)

- Stablecoins will see mainstream adoption for cross-border payments, with Stripe and Ripple leading enterprise adoption

- Real-time payments will become the global standard, replacing ACH and wire transfers

- Open banking mandates will expand globally, creating new opportunities for Plaid-like infrastructure

- Vertical FinTech will dominate, industry-specific solutions (healthcare via Camber Health, construction, logistics) will outperform horizontal players

- IPO resurgence: Chime, DailyPay, and Navan will go public in 2025-2026, opening the floodgates for FinTech public offerings

Emerging Sub-Sectors: AI in Finance, InsurTech, Embedded Finance

AI in Finance: Artificial intelligence is revolutionizing every FinTech category.

- Underwriting: AI models assess creditworthiness faster and more accurately than FICO scores

- Fraud prevention: Real-time anomaly detection reduces chargebacks

- Personalization: Robo-advisors (Stash, Autonomous) tailor portfolios to individual goals

- Customer service: Chatbots and voice assistants handle 80%+ of support inquiries

InsurTech: Insurance technology is finally catching up to banking and payments innovation.

- Policygenius leads online insurance comparison with $100B+ in coverage placed

- Embedded insurance: Buy insurance at point of purchase (travel, e-commerce, auto)

- On-demand coverage: Pay-per-use insurance for gig workers and shared mobility

Embedded Finance: Non-financial companies are becoming FinTech providers.

- Shopify Balance offers banking to millions of merchants

- Uber Money provides drivers with instant payouts and debit cards

- Tesla Insurance underwrites policies based on vehicle telematics

- Platforms like Unit, Stripe Treasury, and Synapse (infrastructure) enable any company to embed financial services

Impact of Regulation and Global Economics

Regulation remains the double-edged sword of FinTech innovation:

Regulatory Headwinds & Tailwinds

Headwinds:

- Increased scrutiny on crypto (despite Ripple’s recent legal wins)

- Anti-money laundering (AML) compliance costs rising for neobanks

- Consumer Financial Protection Bureau (CFPB) crackdown on overdraft fees and earned wage access

Tailwinds:

- Open banking mandates (EU PSD2, UK Open Banking) expanding to U.S. and Asia

- FedNow instant payments system enabling real-time settlement

- Clearer crypto regulations post-2024 election cycle

- Bank charter pathways for FinTechs (Varo precedent)

Global Economic Factors:

- Interest rates: Higher rates benefit neobanks (interest income) but hurt lending FinTechs

- Recession risk: Economic downturns increase demand for financial management tools (Dave, Brigit) and alternative credit (SoLo Funds)

- Emerging markets: Fastest FinTech growth in MENA (Tabby, Tamara), Latin America (Pomelo), and Africa

FAQs

The most recognizable consumer FinTech brands include:

- Payments: Venmo, Cash App, PayPal

- Neobanks: Chime (22.3M users), Varo, Dave

- Investing: Robinhood (well-known), Stash

- Personal finance: Dave, Brigit, Copilot, MoneyLion

- Crypto: Gemini, Coinbase

Why they’re popular: These apps focus on financial inclusion, low or no fees, and intuitive mobile experiences that traditional banks struggle to match.

Based on employee satisfaction, growth trajectory, and company culture, top FinTech employers include:

- Stripe: Industry-leading compensation, remote-first culture, massive global scale

- Plaid: Mission-driven team with a strong engineering culture

- Ramp: Fast growth, AI-forward product, strong presence in NYC

- Navan: Near-IPO stage with global expansion opportunities

- Mercury: Startup-friendly culture and highly loved product

- Chime: Pre-IPO equity upside with strong consumer impact

Pro tip: All startups listed have active hiring pages. YC- and a16z-backed companies often offer strong equity packages and steep learning curves.

The MENA region is experiencing rapid FinTech growth, driven by young populations, high smartphone adoption, and government-led digital transformation:

- Tabby (UAE): $4.5B valuation and the region’s leading buy-now-pay-later provider

- Tamara (Saudi Arabia): Up to $2.4B financing package and a major BNPL competitor

- Emerging players: BOSS Money, focused on remittances from the U.S. to LATAM

Why MENA matters: FinTech funding in the region has grown over 400% since 2019, with Saudi Arabia, the UAE, and Egypt emerging as key hubs for payments, Islamic finance, and remittance solutions.

FinTech startups gain competitive advantage by tracking AI Visibility Score, citation frequency in LLM responses, and E-E-A-T signal strength—metrics that determine how often brands appear in AI-generated answers from ChatGPT, Perplexity, and Google AI Overviews.

According to the 2025 Fintech Payments AI Visibility Index, Stripe leads with a 77% AI Visibility Score, followed by PayPal (64%) and Square (50%), meaning these brands appear in over half of relevant AI-generated financial answers.

The four critical AI visibility metrics for FinTech startups are:

- AI Visibility Score (Citation Frequency): This measures how often a brand is mentioned in AI-generated responses across platforms like ChatGPT, Gemini, and Perplexity. Research shows ChatGPT’s citations for financial queries surged 556% throughout 2025, from 0.9% in spring to 5.9% by year-end. Only 10 companies in the payments sector exceed 10% AI visibility, while the median sits at 1-2%.

Tools like Wellows help startups track their citation rate across industry queries and compare performance against competitors in real-time. - Citation Quality & E-E-A-T Signals: AI models prioritize content demonstrating Experience, Expertise, Authoritativeness, and Trustworthiness (E-E-A-T). According to UpGrowth research, 88% of financial citations come from brand-managed sources, meaning FinTech companies control the primary levers of visibility through authoritative content, expert quotes, and specific data points.

The 2025 AI Visibility Index found that product pages on brand websites accounted for 25% of all branded citations. - Structured Data Implementation: Schema markup enables AI systems to parse financial product information reliably. FinTech startups implementing structured data for services, pricing, locations, and FAQs see measurably higher citation rates.

Princeton University research cited in the UpGrowth study demonstrates that adding authoritative citations, expert quotations, and specific statistics can boost AI visibility by up to 40%. - Sentiment Distribution in AI Mentions: The Avenue Z Index reveals sentiment patterns by company stage: growth-stage brands achieve 75% positive sentiment when mentioned (driven by specialized innovations and pricing transparency), mid-market niche players earn 65% positive sentiment through easy-to-integrate solutions, while enterprise brands control 87% of total AI share of voice despite mixed sentiment.

Wellows provides bootstrapped FinTech founders with multi-platform monitoring across ChatGPT, Perplexity, Gemini, and Google AI Overviews. The platform tracks citation frequency for target queries, analyzes competitor positioning, identifies content gaps affecting visibility, and provides actionable recommendations.

Unlike enterprise tools requiring $10K+ monthly commitments, Wellows offers startup-friendly pricing with automated reporting that non-technical founders can execute on immediately.

Fintech startups leading in real-time payments and instant transfers between bank accounts operate across rapidly expanding domestic and international payment networks, reflecting a major shift in how money moves.

- In the United States, real-time payments primarily run through two networks: the FedNow Service, which processed 8.4 million transactions in 2025 representing 458.9% year-over-year growth and $853 billion in total value according to Federal Reserve data, and the RTP (Real-Time Payments) network operated by The Clearing House, which processed $481 billion in Q2 2025 alone, a 195% leap from the previous quarter.

- Plaid plays a critical infrastructure role by connecting over 8,000 fintech apps to 12,000 financial institutions and added FedNow-based instant payout capabilities to its Transfer product in 2023, enabling companies to disburse funds instantly rather than waiting 1–3 business days for ACH settlement.

- International leaders include Flutterwave, which provides real-time payment infrastructure across Africa and processes payments in 150+ currencies, and Yape in Peru, which grew to over 20 million users by 2025 by offering instant, commission-free peer-to-peer transfers without requiring traditional bank accounts.

The rapid adoption reflects a fundamental shift in consumer and business expectations, as 58% of US financial institutions enabling instant payments now support both RTP and FedNow, ensuring redundancy and maximizing reach.

FinTech startups typically work with neobanks and sponsor banks that specialize in startup-friendly compliance, APIs, and scalability.

- Mercury: Popular with early-stage FinTech and SaaS startups for fast onboarding and treasury tools.

- SVB (Silicon Valley Bank): Historically dominant in FinTech banking, now operating under new ownership with continued startup focus.

- Evolve Bank & Trust and Cross River Bank: Leading sponsor banks powering FinTech products like cards, payments, and lending.

Why it matters: Choosing the right banking partner is critical for regulatory compliance, payment processing, and scaling FinTech products.

Several top-tier venture capital firms consistently invest in FinTech across payments, banking, lending, and infrastructure.

- Sequoia Capital: Backer of Stripe, Plaid, Ramp, and Fireblocks.

- Andreessen Horowitz (a16z): Invests across FinTech, crypto, and infrastructure, including Stripe and Navan.

- Accel: Early investor in FinTech leaders like Nubank and Brex.

- Index Ventures: Known for backing Plaid, Wise, and Revolut.

Insight: These firms invest across multiple FinTech layers, from consumer apps to deep financial infrastructure.

Infrastructure-heavy FinTech startups are typically funded by VCs with long investment horizons and technical expertise.

- Andreessen Horowitz: Focuses on APIs, payments infrastructure, and embedded finance platforms.

- Sequoia Capital: Backs large-scale infrastructure players like Stripe and Plaid.

- Index Ventures: Invests in foundational FinTech layers, including payments and open banking.

- Ribbit Capital: Specializes exclusively in financial services and FinTech infrastructure.

Why these investors matter: Infrastructure FinTechs require patient capital due to long sales cycles, regulatory complexity, and high upfront costs.

Blockchain and crypto-focused FinTech startups are supported by a mix of traditional VCs and crypto-native investment firms.

- a16z Crypto: One of the most active investors in blockchain infrastructure and crypto FinTech.

- Paradigm: Focuses on crypto protocols, exchanges, and financial infrastructure.

- Pantera Capital: Early investor in blockchain-based FinTech and digital asset platforms.

- Sequoia Capital: Invests selectively in crypto and blockchain FinTech infrastructure.

Trend: These investors prioritize security, scalability, and real-world financial use cases over speculative tokens.

Final Thoughts on FinTech Startups

The 38 FinTech startups featured here represent the forefront of financial innovation in 2026. From Stripe’s $1.4T payment volume and Chime’s 22.3M users to Plaid’s open-banking infrastructure and Kalshi’s regulated prediction markets, these companies are reshaping how money moves, scales, and complies.

- Investors: Focus on B2B infrastructure, emerging markets, and AI-native FinTechs, with IPOs expected from

Chime, DailyPay, and Navan. - Founders: The biggest whitespace lies in vertical FinTech and embedded finance,

powered by platforms like Stripe and Plaid. - Talent & institutions: Pre-IPO startups offer strong upside, while banks must partner or build to stay relevant

as open banking adoption accelerates.

As AI, blockchain, and regulation converge, FinTech’s next decade will be led by startups backed by Sequoia, a16z, and Y Combinator, setting the foundation for global financial systems ahead.

![AI Visibility for B2B Marketing Agencies: The Shortlist-Defense Playbook [2026]](https://wellows.com/wp-content/uploads/2026/06/ai-visibility-b2b-marketing-agencies.webp)